Europe holds a 2.5% share of a market it helped build July 08, 2026 New data from in4ma and EMSNOW puts the global EMS and ODM industry at USD 820 billion for 2025 – and Europe's share of that figure is shrinking in relative terms even as the continent's largest players post revenue growth.

The next two years won't offer shortcuts – A memory market reality check May 25, 2026 Following his presentation at Evertiq Expo Zürich, Memphis Electronics' Nikolaos Florous had a conversation with Evertiq to go deeper on the market outlook. The short version: conditions will stay difficult, and procurement teams that haven't adapted yet are running out of time.

Kioxia, Solidigm and SanDisk invests in Nanya Technology April 14, 2026 Nanya Technology Corporation has received strategic participation in its private placement from Kioxia, SK hynix subsidiary Solidigm and SanDisk, as the company accelerates investment in advanced DRAM capacity for AI-driven demand.

Samsung partners with AMD on next-gen AI memory solutions March 30, 2026 The companies will collaborate on HBM4 supply for AMD Instinct MI455X GPUs and next-generation DDR5 solutions for AMD EPYC processors and the AMD Helios platform.

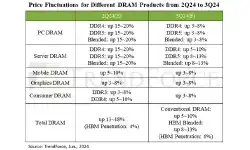

DRAMpocalypse: Memory price projections skyrocket for 1Q26 February 02, 2026 The global memory market is heading toward historically sharp price increases in the first quarter of 2026, according to a new forecast from market research firm TrendForce.

Micron’s PSMC acquisition could support DRAM supply from 2027 January 20, 2026 Micron Technology’s planned acquisition of Powerchip Semiconductor Manufacturing Corp.’s (PSMC) Tongluo fab in Taiwan could help strengthen global DRAM supply from 2027, according to market analyst TrendForce.

SK hynix completes Intel certification for 256GB DDR5 RDIMM January 09, 2026 As an Intel Data Center Certified system/platform, 256GB DDR5 RDIMM has completed extensive testing and rigorous validation by Intel’s Advanced Data Center Development Laboratory.

DRAM and NAND Flash prices to surge in Q1 2026 January 05, 2026 Global memory prices are set to rise sharply in the first quarter of 2026 as suppliers continue to prioritise server and AI-related applications, according to TrendForce.

The memory market isn't correcting - It's reorganising December 03, 2025 Industry analyst Claus Aasholm on why the supply-demand forces that once stabilised DRAM pricing have permanently shifted.

Rising memory prices force console makers to rethink pricing December 02, 2025 Rising memory prices are squeezing profit margins for game console makers, prompting TrendForce to revise downward its 2026 global shipment forecasts for the sector.

Why memory may drive tomorrow’s processor choices November 17, 2025 Device manufacturers were able to enjoy two years of low memory prices. However, this year, the tide has completely turned. Memory manufacturers have pulled the ripcord on both NAND flash memory and DRAM, announcing that they will focus on new memory generations in the future.

Tight DRAM supply to boost DDR5 Contract prices October 30, 2025 TrendForce’s latest investigations show that server DRAM contract prices are strengthening in 4Q25, driven by ongoing data centre expansion among global CSPs.

DRAM module revenue up 7% in 2024, driven by tight supply and restocking October 01, 2025 TrendForce reports that following the completion of inventory digestion in the downstream consumer market concluded at the end of Q4 2023, DRAM suppliers shifted focus towards HBM and server DDR5 products, leading to tighter supply for other DRAM types.

Cadence advances Cloud AI with DDR5 12.8Gbps MRDIMM Gen2 IP April 22, 2025 The Cadence DDR5 MRDIMM IP boasts a new high-performance, scalable and adaptable architecture based on Cadence’s proven and highly successful DDR5 and GDDR6 product lines.

Server DRAM and HBM continue to drive growth February 27, 2025 TrendForce’s latest research reveals that global DRAM industry revenue surpassed USD 28 billion in 4Q24, marking a 9.9% QoQ increase. This growth was primarily driven by rising contract prices for server DDR5 and concentrated shipments of HBM, leading to continued revenue expansion for the top three DRAM suppliers.

Samsung reports sharp drop in profit amid chip slowdown February 03, 2025 The South Korean company’s chip business showed a 2.9 trillion won operating profit due to the tech giant’s slow transition to HBM chips specialized for AI processors.

The memory market: supply, demand, and geopolitical influences in 2025 December 30, 2024 As we head into 2025, the DRAM memory market is bracing for significant turbulence. With price erosion projected across multiple sectors and a shift in production dynamics, it’s clear that the landscape will look vastly different by the second half of 2025.

Server DRAM and HBM boost 3Q24 DRAM Industry revenue November 27, 2024 TrendForce’s latest investigations reveal that the global DRAM industry revenue reached US$26.02 billion in 3Q24, marking a 13.6% QoQ increase.

DRAM prices fall in 2025 amid weak demand and rising inventory November 19, 2024 The fourth quarter is a critical period for setting DRAM contract prices. According to TrendForce's latest research, prices for mature DRAM processes such as DDR4 and LPDDR4X are already falling due to excess supply and dwindling demand.

Global semiconductor revenue to grow 14% in 2025 October 31, 2024 Global semiconductor revenue is projected to grow 14% in 2025 to total USD 717 billion, according to the latest forecast from Gartner. In 2024, the market is forecast to grow 19% and reach USD 630 billion.

Intelligent Memory takes over Memphis' DRAM module product line October 31, 2024 From January 2025, Memphis Electronic will hand over its private-label DRAM modules to Intelligent Memory.

Slowing demand growth constraints Q4 memory price increases October 09, 2024 TrendForce’s latest findings reveal that weaker consumer demand has persisted through 3Q24, leaving AI servers as the primary driver of memory demand. This dynamic, combined with HBM production displacing conventional DRAM capacity, has led suppliers to maintain a firm stance on contract price hikes.

SK hynix develops world's first 6th-gen DRAM chip August 30, 2024 The new DRAM may help data centers reduce electricity costs by 30% thanks to technological innovation in design at a time when the AI boom is hiking power consumption.

DRAM industry surges 24.8% in 2Q24 August 15, 2024 According to TrendForce's most recent data, the DRAM industry had a significant revenue increase in the second quarter of 2024, reaching USD 22.9 billion – a quarter-over-quarter surge of 24.8%.

DRAM prices expected to increase by 8–13% in Q3 July 05, 2024 TrendForce reports that a recovery in demand for general servers — coupled with an increased production share of HBM by DRAM suppliers — has led suppliers to maintain their stance on hiking prices.

HBM3e to reach 35% of advanced wafer input by 2024 May 27, 2024 TrendForce reports that the three largest DRAM suppliers are increasing wafer input for advanced processes. Following a rise in memory contract prices, companies have boosted their capital investments, with capacity expansion focusing on the second half of this year.

Did we finally learn the lesson, or is this just the calm before the storm? May 21, 2024 Following the earthquake in Taiwan in April, the industry expected an impact on chip and especially memory prices. After all, 65% of the world’s advanced nodes are being produced there, and when it comes to AI servers the figure is even higher.

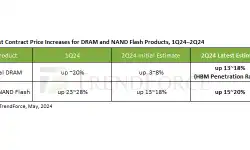

NAND and DRAM contract prices set to increase even more May 08, 2024 TrendForce’s latest forecasts reveal contract prices for DRAM in the second quarter are expected to increase by 13–18%, while NAND Flash contract prices have been adjusted to a 15–20%. Only eMMC/UFS will be seeing a smaller price increase of about 10%.

Powertech to boost CAPEX by 50% to meet demand for memory May 06, 2024 Chip testing and packaging provider Powertech Technology Inc has revealed it will spend USD 460 million on advanced capacity and equipment.

SK Hynix to invest $3.86B in DRAM production in South Korea April 24, 2024 SK hynix says that it plans to expand production capacity of the next-generation DRAM, including HBM, in response to the rapidly increasing demand for AI semiconductors.

2Q24 DRAM price increases expected to narrow March 26, 2024 TrendForce says that despite DRAM suppliers’ efforts to trim inventories, they have yet to reach healthy ranges. As they continue to improve their loss situations by boosting capacity utilisation rates, the overall demand outlook for this year remains tepid.

Rochester and IM ensure availability of legacy storage solutions March 26, 2024 Rochester Electronics and Intelligent Memory (IM) have joined forces to ensure the continued availability of mature and legacy DRAM and NAND storage solutions tailored for industrial and embedded applications.