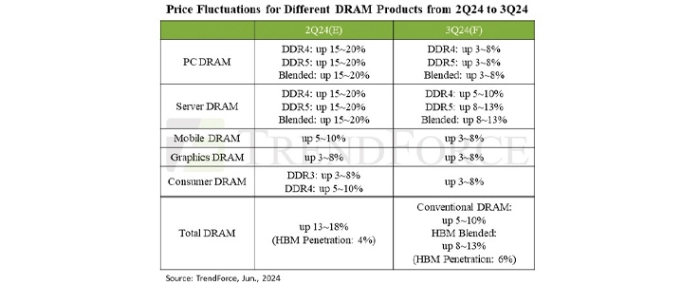

DRAM prices expected to increase by 8–13% in Q3

TrendForce reports that a recovery in demand for general servers — coupled with an increased production share of HBM by DRAM suppliers — has led suppliers to maintain their stance on hiking prices.

As a result, the ASP of DRAM in the third quarter is expected to continue rising, with an anticipated increase of 8–13%. The price of conventional DRAM is expected to rise by 5–10%, showing a slight contraction compared to the increase in the second quarter.

TrendForce notes that buyers were more conservative about restocking in the second, and inventory levels on both the supplier and buyer sides did not show significant changes. Looking ahead to the third quarter, there is still room for inventory replenishment for smartphones and CSPs, and the peak season for production is soon to commence. Consequently, it is expected that smartphones and servers will drive an increase in memory shipments in the third quarter.

PC DRAM prices expected to increase by 3–8% in Q3

PC DRAM prices are expected to continue their upward trend in the third quarter considering the recovery in demand for general servers and the increased production share of HBM by suppliers. The average price is projected to rise by 3–8% QoQ. This increase is lower than that of server DRAM and shows a contraction compared to the second quarter. The main reasons are the high inventory levels of PC DRAM and the lack of significant improvement in consumer demand.

Server DRAM prices are expected to increase by 8–13% in Q3

Benefiting from seasonal stocking demand for general servers in the third quarter, TrendForce estimates that the contract price of DDR5 server DRAM will increase by 8–13%. Due to high average inventory levels of DDR4 among buyers, purchasing momentum will be focused on DDR5, leading to a higher price increase for DDR5 compared to DDR4. As a result, the average contract price for server DRAM—considering both DDR4 and DDR5—is expected to rise by 8–13% QoQ.

Mobile DRAM prices expected to increase by 3–8% in Q3

Continuous price increases for mobile DRAM in 4Q23 have posed significant challenges to the profitability of brands. Additionally, with current inventories being quite sufficient, brands are not in a hurry to enter price negotiations for the third quarter and have adopted a passive stance in negotiations. However, manufacturers are aiming to fill the profit gaps from previous quarters and anticipate a tightening supply-demand balance next year, thereby maintaining their intention to raise contract prices. Nonetheless, due to the passive negotiation stance of buyers and high inventory levels, the price increase in the third quarter may be limited. TrendForce estimates that the quarterly price increase will be between 3–8%, with LPDDR4(X) experiencing the smallest increase and possibly even further contraction.

Graphics DRAM prices expected to increase by 3–8% in Q3

In the third quarter, overall demand for graphics DRAM remains relatively flat, with price trends mainly influenced by the interconnected effects of other DRAM products. With manufacturers firmly entering an upward pricing cycle and the price increase momentum not yet abating, buyers are adopting a continuous stocking strategy, making them more amenable to price hikes proposed by sellers. On the supply side, as new GPUs enter the verification stage, manufacturers are gradually increasing the production of GDDR7, which currently carries a 20–30% premium over GDDR6. The shipment of GDDR7 samples in 3Q24 is expected to slightly push up the average selling price. As such, graphics DRAM prices are anticipated to increase by 3–8% QoQ.

DDR3 & DDR4 prices expected to increase by 3–8% in Q3

The overall consumer DRAM market continues to exhibit oversupply, but the three major suppliers are clearly intent on raising prices due to the capacity squeeze from HBM production. Additionally, Taiwanese manufacturers have yet to return to profitability, creating further upward pressure on prices. As a result, prices are expected to maintain a slight upward trend.

Looking further ahead to the fourth quarter, the need for inventory replenishment by smartphone manufacturers and CSPs—along with an increased production share of HBM by suppliers—will support the continuation of rising prices. As the end of the year approaches, both buyers and sellers will formulate procurement strategies based on the current supply and demand outlook for 2025. Therefore, TrendForce does not rule out the possibility that buyers will continue to raise inventory levels in anticipation of potential shortages caused by the increased share of HBM production in 2025.

For more information visit TrendForce.