© Jakub Jirsak Dreamstime.com

Analysis |

Semiconductor acquisitions regain momentum in 2019

This year’s merger and acquisition announcements are driven by deals in networking and wireless connectivity ICs and by suppliers adding products for automotive systems and other strong-growth markets into the next decade, says IC Insights.

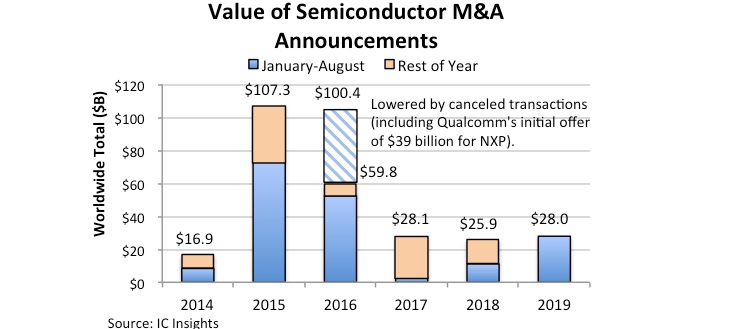

After slowing in the past couple years, semiconductor merger and acquisition activity strengthened in the first eight months of 2019 with the combined value of about 20 M&A agreement announcements reaching USD 28.0 billion for the purchase of chip companies, business units, product lines, intellectual property (IP), and wafer fabs between January and the end of August. IC Insights’ latest update to the 2019 McClean Report shows the dollar value of semiconductor acquisition agreement announcements in the first eight months of 2019 surpassed the USD 25.9 billion total for all of 2018 and was close to topping the value in 2017.

The jump in acquisition agreements in 2019 is being driven by M&A deals for networking and wireless connectivity ICs and by semiconductor suppliers looking to add products for automotive applications and higher-growth markets as they head into the next decade. M&A announcements this year are also resulting from companies refocusing themselves and shedding businesses, such as Intel’s deal in July 2019 to sell its cellphone modem business to Apple for about USD 1 billion after the IC giant struggled for eight years to unseat Qualcomm as the market leader. In May 2019, Marvell announced the sale of its Wi-Fi Connectivity business to NXP for USD 1.7 billion. That month, Marvell also said it would acquire GlobalFoundries’ ASIC business for USD 650 million and buy Multi-Gig Ethernet and networking controller supplier Aquantia for USD 452 million as the company shifts emphasis to data centers and related networks. There have been a half-dozen semiconductor acquisition announcements in 2019 valued at USD 1 billion or more, together representing 89% of the M&A total so far this year.

While it is impossible to predict how many acquisition announcements will be made in the next several months, 2019 is virtually certain to surpass 2017 as the third largest year for semiconductor M&A agreements. Semiconductor M&A peaked in 2015 with more than 30 deals valued at USD 107.3 billion, followed by USD 100.4 billion for about 30 M&A announcements in 2016. The final value for 2016 M&A announcements was lowered to USD 59.8 billion because several large acquisitions were eventually canceled after failing to win government regulatory approvals in the U.S. and China. The U.S.-China trade war and government agencies protecting domestic semiconductor industries have discouraged some companies from attempting to strike large acquisition agreements in the past couple years.

It is important to note that IC Insights’ M&A list covers purchase agreements for semiconductor companies and business units, product lines, chip IP, and wafer fabs, but it excludes acquisitions of software and system-level businesses by IC companies. IC Insights’ list of acquisitions also excludes transactions between semiconductor capital equipment suppliers, material producers, chip packaging and testing companies, and design-automation software firms.

The jump in acquisition agreements in 2019 is being driven by M&A deals for networking and wireless connectivity ICs and by semiconductor suppliers looking to add products for automotive applications and higher-growth markets as they head into the next decade. M&A announcements this year are also resulting from companies refocusing themselves and shedding businesses, such as Intel’s deal in July 2019 to sell its cellphone modem business to Apple for about USD 1 billion after the IC giant struggled for eight years to unseat Qualcomm as the market leader. In May 2019, Marvell announced the sale of its Wi-Fi Connectivity business to NXP for USD 1.7 billion. That month, Marvell also said it would acquire GlobalFoundries’ ASIC business for USD 650 million and buy Multi-Gig Ethernet and networking controller supplier Aquantia for USD 452 million as the company shifts emphasis to data centers and related networks. There have been a half-dozen semiconductor acquisition announcements in 2019 valued at USD 1 billion or more, together representing 89% of the M&A total so far this year.

While it is impossible to predict how many acquisition announcements will be made in the next several months, 2019 is virtually certain to surpass 2017 as the third largest year for semiconductor M&A agreements. Semiconductor M&A peaked in 2015 with more than 30 deals valued at USD 107.3 billion, followed by USD 100.4 billion for about 30 M&A announcements in 2016. The final value for 2016 M&A announcements was lowered to USD 59.8 billion because several large acquisitions were eventually canceled after failing to win government regulatory approvals in the U.S. and China. The U.S.-China trade war and government agencies protecting domestic semiconductor industries have discouraged some companies from attempting to strike large acquisition agreements in the past couple years.

It is important to note that IC Insights’ M&A list covers purchase agreements for semiconductor companies and business units, product lines, chip IP, and wafer fabs, but it excludes acquisitions of software and system-level businesses by IC companies. IC Insights’ list of acquisitions also excludes transactions between semiconductor capital equipment suppliers, material producers, chip packaging and testing companies, and design-automation software firms.

For more information visit © IC Insights

The jump in acquisition agreements in 2019 is being driven by M&A deals for networking and wireless connectivity ICs and by semiconductor suppliers looking to add products for automotive applications and higher-growth markets as they head into the next decade. M&A announcements this year are also resulting from companies refocusing themselves and shedding businesses, such as Intel’s deal in July 2019 to sell its cellphone modem business to Apple for about USD 1 billion after the IC giant struggled for eight years to unseat Qualcomm as the market leader. In May 2019, Marvell announced the sale of its Wi-Fi Connectivity business to NXP for USD 1.7 billion. That month, Marvell also said it would acquire GlobalFoundries’ ASIC business for USD 650 million and buy Multi-Gig Ethernet and networking controller supplier Aquantia for USD 452 million as the company shifts emphasis to data centers and related networks. There have been a half-dozen semiconductor acquisition announcements in 2019 valued at USD 1 billion or more, together representing 89% of the M&A total so far this year.

While it is impossible to predict how many acquisition announcements will be made in the next several months, 2019 is virtually certain to surpass 2017 as the third largest year for semiconductor M&A agreements. Semiconductor M&A peaked in 2015 with more than 30 deals valued at USD 107.3 billion, followed by USD 100.4 billion for about 30 M&A announcements in 2016. The final value for 2016 M&A announcements was lowered to USD 59.8 billion because several large acquisitions were eventually canceled after failing to win government regulatory approvals in the U.S. and China. The U.S.-China trade war and government agencies protecting domestic semiconductor industries have discouraged some companies from attempting to strike large acquisition agreements in the past couple years.

It is important to note that IC Insights’ M&A list covers purchase agreements for semiconductor companies and business units, product lines, chip IP, and wafer fabs, but it excludes acquisitions of software and system-level businesses by IC companies. IC Insights’ list of acquisitions also excludes transactions between semiconductor capital equipment suppliers, material producers, chip packaging and testing companies, and design-automation software firms.

For more information visit © IC Insights