The consolidation war chest: Who has the firepower to buy the growth?

The companies announced as many as 13 acquisitions last year, of which 12 have been realised. Many companies are still indicating to have further acquisitions on the agenda. It will be interesting to look at the remaining M&A firepower in their balance sheets to estimate what to expect.

Author: Riku Hynninen - CEO & Founder - Agame Oy

This is part 2 of the article series "EMS under the hood" – part 1, Dissecting the financial engines of Europe’s manufacturing leaders, can be found here.

In part 2, following the acquisition spree of 2025, which companies still have the most firepower in their balance sheet to continue with the industry consolidation, and which companies would have to consider raising new capital?

| Acquiring company | Target company | Est revenue of acquired | Valuation EV/EBITDA | Status |

| Cicor | TT electronics | €625M | 6,5x | Offer rejected |

| Cicor | Eolane | €134M | N/A (distressed) | Closed Apr 2025 |

| Cicor | Valtronic (2 sites) | €21,5M | N/A | Closed Nov 2025 |

| Cicor | Mades | €29M | N/A | Closed Aug 2025 |

| Hanza | Leden Group | €100M | 7x (EBITA) | Closed Mar 2025 |

| Hanza | Milectria | €30M | 4,9x | Closed Oct 2025 |

| Hanza | BMK Group | €300M | 8x (10x-12x EV/EBIT) | Closed Jan 2026 |

| Scanfil | ADCO | €32M | 5.4x | Closed Dec 2025 |

| Scanfil | MB Elettronica | €100M | 10.2x (midpoint) | Closed Jan 2026 |

| Kitron | Delta Nordic | €74M | 9,65x | Closed Jan 2026 |

| NOTE EMS | Kasdon Group | €14M | 6x | Closed Oct 2025 |

| Inission | UAB Selteka | €16M | 5.5x-8x | Closed July 2025 |

| Incap | Lacon Group | €68M | 7x-8x | Closed 1Q2026 |

| Table 1: Announced acquisitions in 2025 | ||||

Covenants, cash, and execution capability

It is worth noting that the firepower is not only about financial tools, including the equity component, but also about an organisation's capability to execute the M&A process and integration successfully. Both usually stretch the company management, and if there’s too much on the plate at the same time, it may take the focus away from other key priorities and customers.

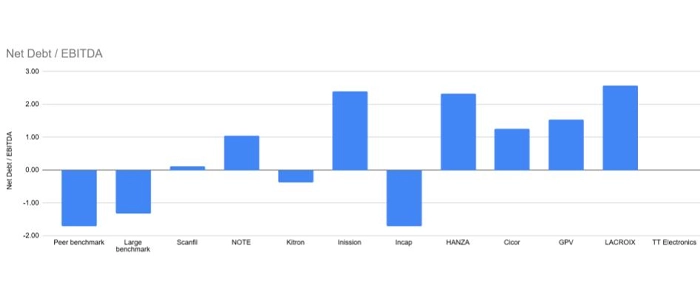

A common method to assess the firepower is to compare the Net Debt / EBITDA to creditor covenants. Among this group, the covenants vary between 2.5 and 3.5. For simplicity and comparability, the net debt includes IFRS 16 lease liabilities. I am aware that some companies net them out in their reporting, while some don’t. Companies are also actively issuing new shares to finance the deals - this is further increasing the firepower, but does have a cost for shareholders through share dilution.

Figure 1. Net Debt / EBITDA at 2025 closing, with benchmarks from peers (left) and giants (second from left). TT Electronics N/A due to negative reported EBITDA. © Agame

The early 2026 deal completions

At the 2025 closing, Kitron and Scanfil had the highest firepower estimated at 200 M€ - 300 M€. Both companies had upcoming acquisitions to be financed in the range of 70-90 M€. Those were closed in early 2026. They were mainly funded by cash/credit facility, in addition to Kitron using their recently issued shares to a minor extent.

As a result, Scanfil’s Net Debt / EBITDA rose to 1.57, the closing of the acquisition eating roughly half of the firepower. Kitron virtually remained debt-free, however as mentioned, they issued new shares worth 80 M€ in November 2025, which can be seen as a smart move given their high market valuation.

Incap’s firepower with their net cash position could be assessed at 100 M€ - 150 M€, which is a considerable amount given their size (215 M€ revenue). After the closing of the Lacon acquisition worth about 50 M€, their Net Debt / EBITDA increased to ~0.4x, still plenty of firepower for additional acquisitions (50 M€ - 100 M€).

With their 1.25 x Net Debt / EBITDA, Cicor does have about 100 M€ further firepower before hitting their covenants. Actually, their ~300 M€ failed buyout bid for TT Electronics would have been a stretch, involving also new shares issued. It would have increased Cicor leverage very close to covenant levels and diluted their shares. Knowing Cicor’s bold and active moves in the M&A space, it will be interesting to watch their next move. Actually, in June 2026, Cicor announced a divestiture of a Tunisian factory, and a >10 MCHF profitability improvement program to realize integration synergies from their numerous earlier acquisitions.

With Inission’s Net Debt / EBITDA at 2.4x, their firepower is estimated at 20 M€ - 30 M€. They are signalling a continued strategy of growing both organically and inorganically. One could expect Inission to continue with smaller acquisitions that have been typical for them in the past, unless they make a share issue for a bigger move.

Taking a Breather

GPV is more likely to stay away from major acquisitions until the operational performance in its current setup improves, even if it has about 100 M€ firepower remaining to the assumed 3x Net Debt / EBITDA threshold.

GPV seems to still be digesting the Enics merger in 2022, and has recently been suffering from revenue and EBIT decline. Perhaps reflecting this, rather than acquisitions, GPV announced a partnership with a US-based company, EastWest late 2025 to widen their footprint in the region. Finally, it is worth mentioning that GPV is a part of the parent company Schouw & Co., which provides them with additional liquidity opportunities.

Hanza’s Net Debt / EBITDA at the end of 2025 was 2.3x. In January 2026, they closed the acquisition of BMK, valued at a bit above 200 M€. They financed the deal by issuing ~17 million new Hanza shares with historically strong EV/EBITDA hovering around 20x. With a streak of recent acquisitions (OrbitOne, Leden Group, Milectria and BMK), Hanza Group is signalling towards taking a breather with acquisitions. They are moving from an aggressive growth phase to a technology and efficiency development phase called “Hanza 2028”.

NOTEs firepower at the end of 2025 was about 100 M€. In early 2026, they acquired STI in the UK for about 80 M€ which took their Net Debt / EBITDA from ~1.1x to above 2x. This acquisition was in addition to the Kasdon acquisition a few months earlier. It is likely that also NOTE will focus more on successful execution and integration than further acquisitive growth.

Lacroix and TT Electronics, both recovering from heavy restructuring, are most likely to focus on further stabilising and improving their continuing business before considering acquisitions.

| Company | Net Debt / EBITDA (2025 Close) | Estimated M&A Firepower at the end of 2025 based on Net Debt IFRS16 / EBITDA | Current M&A Focus |

| Kitron | Net cash | 200 M€ - 300 M€ | Closed major acquisition in early 2026, virtually remained debt free. Signalling importance of proper integration - low likelihood for major acquisitions despite the remaining firepower |

| Scanfil | 0.1x (Rose to 1.57 after MB acquisition) | 200 M€ - 300 M€ | Roughly half of initial firepower used in 2026 MB acquisition. Smaller size acquisitions may follow |

| Incap | Net cash (~0.4x after Lacon acquisition) | 100 M€ - 150 M€ | Plenty of firepower for additional acquisitions, however expected to focus on integration |

| Cicor | 1.25x | ~100 M€ | Based on acquisition history, expected to continue to pursue new deals. Profitability improvement program 6/26 could be a sign of slowing down and focusing on integration? |

| NOTE | ~1.1x (Rose to >2x after STI acquisition) | ~100 M€ (Before STI acquisition of 72 M£, or 84 M€) | Likely to focus more on successful execution and integration than further acquisitive growth. |

| Hanza | 2.3x | ~10 - 20 M€ | Signalling toward taking a breather with acquisitions after the recent deal streak |

| GPV | 1.5x | ~100 M€ | Likely to stay away from major acquisitions, continued focus on current setup and its performance |

| Inission | 1.3x | ~20 M€ - 30 M€ | Likely to continue with smaller acquisitions. |

| Lacroix | 2.6x | - | Most likely to focus on stabilising and improving business after restructuring. |

| TT Electronics | *EBITDA negative | - | Most likely to focus on stabilising and improving business after restructuring. |

Need for Net Working Capital May Change Quickly

There is a special characteristic in the EMS business model that is crucial to understand when assessing debt ratios and firepower. Net working capital that consists of inventory, trade payables and receivables, is very sensitive to business environment changes. For example, between 2020 and 2023 when supply chains got inflated, the EMS companies’ net working capital generally increased by 50% to 100% within 1-2 years. Imagine suddenly having to tie up 100 M€ capital for ongoing business, only to sustain sufficient liquidity.

What about giant EMS companies, how do their balance sheets look like? A quick look shows that their net debt / EBITDA varied between -1.3x to 0.8x, telling a story how important it is to keep the balance sheet in good shape in the working capital-heavy business model of EMS companies.

Based on the balance sheet and communicated intentions, I consider Cicor and Inission as the most likely candidates to announce new deals in the coming months, while Lacroix and TT Electronics will continue on their recovery paths. The rest of the pack is likely going to focus on integrating the recent acquisitions. However, I still see some possibilities for opportunistic moves if something really interesting becomes available, as there is still firepower left. And let’s not forget that there’s always a possibility to issue shares when really good opportunities arise!

Having a massive war chest is a strategic advantage, but spending it unwisely on inefficient operations is a fast track to shareholder disappointment. In our final part to be released later, we go 'into the weeds' of Capital Efficiency to see who is running the leanest supply chain in the business.

During Evertiq Expo Warsaw on October 22, 2026, Riku Hynninen will take the stage to present a financial benchmarking analysis of 10 leading European EMS companies. His presentation will explore how profitability is shaped by factors such as depreciation, interest and taxation, while also identifying which companies are best positioned for future M&A activity following recent industry consolidation.