Global 300mm fab capacity to reach new high in 2025

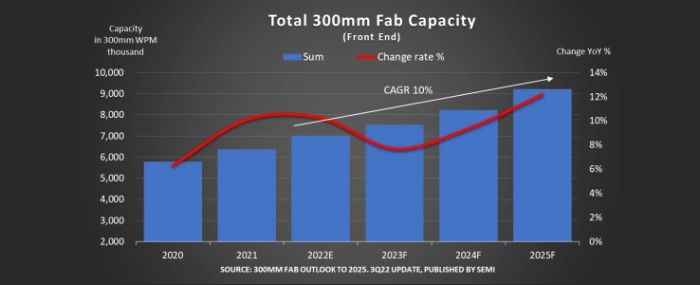

Semiconductor manufacturers worldwide are forecast to expand 300mm fab capacity at a nearly 10% compound average growth rate (CAGR) from 2022 to 2025, reaching an all-time high of 9.2 million wafers per month (wpm), SEMI reports.

SEMI points to strong demand for automotive semiconductors and new government funding and incentive programs in multiple regions as drivers of much of the growth.

The organisation says that it is currently tracking 67 new 300mm fabs or major additions of new lines to start construction from 2022 to 2025.

New fabs announced by companies including GlobalFoundries, Intel, Micron, Samsung, SkyWater Technology, TSMC and Texas Instruments are ramping in 2024 or 2025 to help meet the growth in demand.

"While shortages of some chips have eased and supply of others has remained tight, the semiconductor industry is laying the groundwork to meet longer-term demand for a broad range of emerging applications as it expands 300mm fab capacity," says Ajit Manocha, SEMI President and CEO.

Regional outlooks

China is projected to increase its global share of 300mm front-end fab capacity from 19% in 2021 to 23% in 2025, reaching 2.3 million wpm, a rise driven by factors including growing government investments in the domestic chip industry. With the growth, China is nearing global leader Korea in 300mm fab capacity and is expected to overtake Taiwan, now in second place, next year.

Taiwan's worldwide capacity share is expected to slip 1% to 21% from 2021 to 2025, while Korea's share is also projected to edge 1% lower to 24% during the same period. Japan's share of worldwide 300mm fab capacity is on a path to fall from 15% in 2021 to 12% in 2025 as competition with other regions increases.

The Americas' global share of 300mm fab capacity is forecast to rise from 8% in 2021 to 9% in 2025, driven partly by U.S. CHIPS Act funding and incentives. Europe/Mideast is projected to increase its capacity share from 6% to 7% during the same period on the strength of European CHIPS Act investments and incentives. Southeast Asia is expected to maintain its 5% share of 300mm front-end fab capacity during the forecast period.

From 2021 to 2025, the 300mm Fab Outlook to 2025 shows Power-related capacity with the strongest growth at a 39% CAGR, followed by Analog at 37%, Foundry at 14%, Opto at 7% and Memory at 5%.

SEMI's latest update of the 300mm Fab Outlook to 2025 report tracks 356 current and future fabs.