BYD closes in on Tesla in Q2 BEV sales

The global automotive landscape is undergoing a decisive shift toward new energy vehicles (NEVs). TrendForce reports that in 1H23, NEV sales – which encompass battery electricity vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and fuel cell electric vehicles (FCEVs) – soared to an impressive 5.462 million units, reflecting a growth of 33.6% YoY.

Specifically, Q2 sales reached 3.03 million units, a 42.8% YoY surge, constituting 14.4% of total car sales for the period, and playing a pivotal role in 1H23 growth.

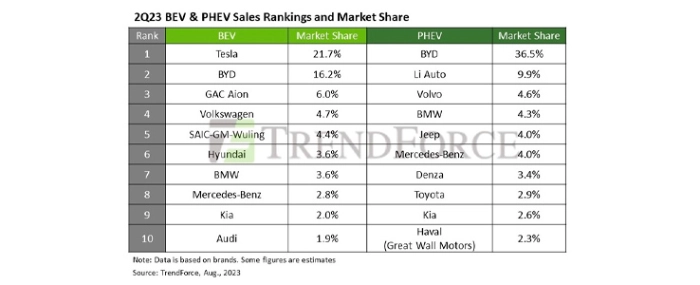

In Q2, BEVs alone posted sales of 2.151 million units, marking 39.3% growth YoY. While Tesla maintains the lead with a market share of 21.7%, BYD trails closely behind with a boosted share of 16.2%. Moreover, GAC Aion, a brand that has been making waves primarily in the Chinese market with its high value-for-money proposition, clinched the third spot with a 6% market share. Recently, the company has launched high-end models priced above CNY 220,000, aiming to diversify its product range. The top 10 BEV brands in Q2 remained fairly consistent with Q1, with only a minor shuffling in ranks. However, compared to the same period in 2022, fewer Chinese brands made the list, likely due to the growing number of EV models from traditional automakers and fierce competition among Chinese brands.

PHEVs weren’t left behind, registering sales of 876,000 units in Q2—a striking 52.9% YoY increase. Astonishingly, about 66% of these sales hailed from the Chinese market. In this segment, BYD continued its lead with a whopping 36.5% market share. Its high-end subsidiary Denza, recorded increasing sales, escalating its market share to 3.4% and climbing to seventh place. Another brand to watch, Li Auto, set a new Q2 record with 87,000 units sold, keeping its second-place position firm with 10% market share. Among international competitors, both Volvo and Jeep noted growth over the previous year, with Jeep crossing 30,000 units, an achievement that’s brought them into the top five for the first time.

While major markets including China, Western Europe, and the US continue to dominate NEV sales, emerging players like Thailand and Australia have made significant strides in 2023. Both nations exceeded 35,000 units in sales in 1H23, with Thailand quadrupling its 2022 figures and Australia experiencing a fivefold increase.

Although these figures are modest in comparison to global sales, they highlight the vast potential of these markets. Recognising this growth trajectory, many major automobile brands are strategically planning their expansions into these burgeoning regions.

For more information visit TrendForce.