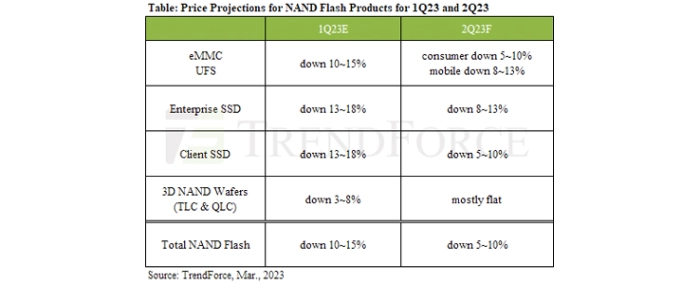

ASP of NAND flash products will continue to fall 5~10% in 2Q23

Although NAND suppliers have continued to roll back production, there is still an oversupply of NAND Flash as demand for products such as servers, smartphones, and notebooks is still too weak.

Therefore, TrendForce predicts that the ASP of NAND Flash will continue to fall in 2Q23, though that decline may shrink to 5~10%. The key to supply and demand returning to a market equilibrium lies in whether NAND suppliers can cut back on production even more. TrendForce believes if demand remains stable, then the ASP of NAND Flash will have an opportunity to rebound in 4Q23; if demand is weaker than expected, then ASP will take longer to recover.

Client SSD: Currently, PC OEMs have managed to liquidate most of their component inventory, and are now gearing up in preparation for mid-year sales events. Suppliers are cutting prices to clear out their inventories of PCIe Gen 3 SSDs, which are gradually being phased out. Meanwhile, prices of PCIe Gen 4 SSDs continue to face downward pressure due to a slow intake of new customer orders. The continuous decline of QLC products in 1Q23 has also dragged down the prices of TLC products, and there is relatively little room for prices to keep falling in 2Q23. While it still remains unclear whether or not demand will recover, TrendForce projects that the prices of PC client SSDs will drop 5~10% in 2Q23.

Enterprise SSD: TrendForce predicts that demand from Chinese CSPs will steadily increase as a result of China’s annual Two Sessions gathering. In addition, the launch of AMD Genoa will continue to drive shipments of enterprise SSDs. It is expected that prices will continue to fall in 2Q23 as supply exceeds demand; suppliers have sustained significant losses from sales, which has weakened their ability to negotiate. TrendForce estimates that the price decline of enterprise SSDs will narrow to 8~13% in 2Q23.

eMMC: Demand for small-capacity eMMCs has remained stable while demand for large-capacity products has been impacted by weak NB and smartphone markets. Aggressive price undercutting between module houses has significantly driven down prices of small-capacity eMMCs in 1Q23, leaving not much room for further downward movement next quarter. Large-capacity eMMCs will experience a greater decrease in prices due to being linked to smartphone UFSs of the same capacity, even as suppliers actively push for sales. TrendForce predicts that eMMC prices will decline by 5~10% in 2Q23.

UFS: NAND suppliers will continue to push for sales of large-capacity UFSs to encourage customers to upgrade the storage capacity of their smartphone products. The introduction of UFS 4.0 means that many flagship smartphone models will be seeing an upgrade in storage capacity. Meanwhile, inventory levels of smartphone components have mostly returned to normal levels, and suppliers are debating whether to stock up for mid-year sales events and peak season demand in 2H23. TrendForce believes that suppliers may accelerate the bottoming of UFS prices as buyers decide how much they wish to purchase in the next quarter. It is estimated that UFS prices in 2Q23 will fall between 8~13%.

NAND Flash wafer: Inventory levels in module houses have returned to normal. Module houses are gradually purchasing more components and creating low-price inventory—operating under the belief that demand for SSDs, memory cards, disks, and other products will recover in 2H23—in order to avoid absorbing inflated costs when prices rebound in the future. NAND suppliers have managed to limit overstock by controlling bit output through delaying their transition to new processes and reducing wafer starts. As a result, NAND Flash wafer contract prices are seeing shrinking declines. TrendForce reports that NAND suppliers that have already implemented production cuts have had their contract prices fall to cash costs, and have avoided further losses from price cutting. TrendForce estimates that contract prices of NAND Flash wafers in 2Q23 will largely level out.

For more information visit Trendforce.

.png)