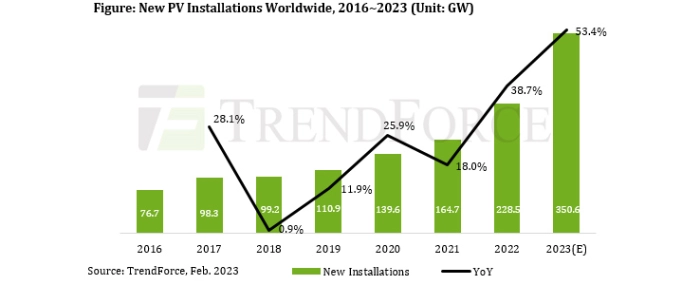

Global PV installations will grow by more than 50% YoY

TrendForce’s latest research on the global market for solar PV reveals that some of the unmet demand that emerged during the 2021~2022 period has been carried over to 2023.

In the past two years, the supply chain for PV products experienced pandemic-related disruptions, and prices of PV modules (solar panels) were high due to a supply crunch for polysilicon. These factors led to delays in installations of PV systems. Moving into this year, prices have fallen back to their usual ranges across the supply chain due to a significant growth in the overall production capacity for polysilicon. Therefore, the global PV demand is expected to expand significantly. TrendForce currently projects that new PV installations worldwide will total 351 GW and show a YoY growth rate of 53.4% for 2023. However, there are potential factors that could negatively affect the market. For instance, there are still concerns about the global economy exhibiting a serious slowdown. Additionally, high inflation remains a challenge for many countries. Hence, the release of installation demand may not proceed as smoothly as anticipated if governments are unable to provide the necessary financial resources to support their policies for promoting renewable energy.

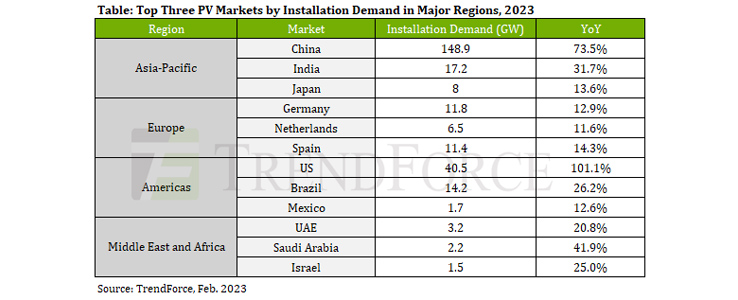

According to TrendForce’s analysis, the Asia-Pacific region has the largest amount of installation demand in 2023. It is followed by Europe, the Americas, and the combined regions of the Middle East and Africa. New PV installations in the Asia-Pacific region are currently projected to reach 202.5 GW by 2023, reflecting a YoY growth rate of 55.4%. Countries in the Asia-Pacific region that are projected to post a high growth rate of more than 40% include China, Malaysia, and the Philippines. In these markets, government policies are the primary accelerant for installation growth. Turning to the more mature markets such as Japan, Australia, and South Korea, they will be seeing a more stable level of installation demand during 2023.

With regard to Europe, new PV installations in the region are projected to increase by 39.7% YoY to around 68.6 GW for 2023. Germany, Spain, and the Netherlands are the main demand contributors. To address the problem of persistently high electricity prices, governments of many European countries have provided subsidies and tax credits to promote the deployment of PV systems. These incentives, together with falling prices for PV modules, will be driving installation growth across the region this year, especially in relation to residential PV projects. Furthermore, the EU has loosened the regulations concerning permits and applications for setting up PV projects. The lowering of the regulatory barriers will also synergize with the decline in module prices, thereby encouraging the development of large-scale projects. TrendForce believes the installation demand related to the construction of ground-mounted PV power stations in Europe will return to positive growth during the 2023~2024 period.

Looking at the Americas as a whole, new PV installations are projected to total around 64.6 GW for 2023. This figure translates to a YoY growth rate of 65.2%. In the Americas, PV demand has been highly concentrated in a few countries such as the US, Brazil, and Chile. However, Colombia and Canada will witness a surge in grid connections of new PV projects this year. Regarding the US market, it was previously affected by the Uyghur Forced Labor Prevention Act and the anti-circumvention investigation on several Southeast Asian countries. And there was a slowdown in new installations related to ground-mounted PV power stations since this kind of project is highly sensitive to cost fluctuations. However, the US market will again exhibit strong growth in 2023 because the Inflation Reduction Act has helped increase the number of projects in the pipeline. There is a possibility of a doubling of the installation demand from the US in 2023. Turning to Brazil, the government there continues to promote distributed PV projects. These include rooftop PV projects for residential, commercial, and industrial settings. As for centralized PV projects such as ground-mounted PV power stations, the related installation demand could grow at a much faster pace if the country’s regulatory regime undergoes further liberalization.

Lastly, with regard to the Middle East and Africa, these regions are showing steady growth. The two regions together will add 14.9 GW of new PV installations in 2023, thereby posting a YoY growth rate of around 49.5%. TrendForce points out that the installation growth of Mideast and African countries is highly dependent on renewable energy tenders, and projects involving large ground-mounted PV power stations account for much of the demand from these markets. The major growth contributors in the two regions are the UAE, Saudi Arabia, South Africa, and Israel. Presently, tendered projects that are either to be built or being built in the two regions come to a total of more than 9GW. TrendForce also notes that Mideast and African countries have an abundance of solar resources and offer strong policy incentives for the development of renewable energy. Thus, the potential for growth is huge. TrendForce expects the two regions to provide more and more solar tenders in the future.

For more information visit TrendForce.

.png)