PMIC demand stable in 2H22 considering automotive demand

According to TrendForce, market conditions in 1H22 were chaotic and there was disparate demand for chips of varying functionality. Given the global development of electronic devices and power systems, the overall demand for power management ICs (PMIC) is still relatively good.

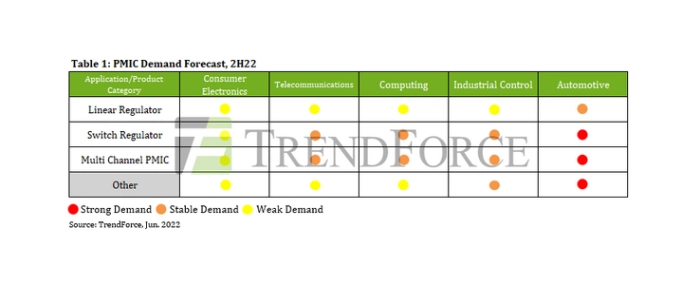

PMICs are used in consumer electronics, communications, computing, industrial control, automotive and other fields. In 2H22, supply and demand gradually diverged and demand for automotive Switching Regulators, Multi-Channel PMICs was strongest.

According to TrendForce, there are various specifications and types of PMICs, including Linear Regulators, etc. Even usage scenario dependent products such as Battery Charging & Management, Voltage References, and USB Power Delivery ICs all fall into this category.

In the field of consumer electronics, it was true that demand for linear regulators and switch regulators with relatively simple functions and structures in the panel, home appliance, and consumer notebook markets fell in 1H22 and orders are even forecast to be revised down by 15-30%. However, multi-channel PMICs with slightly longer lead times will experience price competition pressure in 2H22 as OEMs and ODMs control inventory to a level of less than 2 months. As for the industrial control and automotive markets, these fields have always been vital battlegrounds ripe for conquest and demand higher requirements for PMIC voltage accuracy, temperature control, and reliability. With the trend toward Industry 5.0 and automotive electrification, product pricing will maintain strength into 2H22 but this field is mostly dominated by IDM players that have been in the market for decades such as Texas Instruments (TI), Infineon, Analog Devices (ADI), STMicroelectronics (ST), ON Semiconductor (onsemi), etc., while the proportion of small and medium-sized Fabless operators is relatively low.

Looking at the current delivery status, from the perspective of IDMs with a PMIC market share of more than 61%, due to comprehensive product portfolios, stable quality, and irreplaceability coupled with strong demand for production capacity, the current lead time for new orders is still long, with average lead time for switch regulators at 36 to 46 weeks and 40 to 50 weeks for multi-channel PMICs. However, some existing orders with an original lead time of more than 52 weeks can be shipped 4 to 16 weeks earlier. In addition, from the perspective of small and medium-sized Fabless operators, since they are not on the level of IDM manufacturers in terms of product specifications and application areas, lead time is generally shorter than that of large IDM manufacturers, usually no more than 28 weeks.

TrendForce indicates, that during the major shortages of the past year, Fabless and IDM players shared in the dividends provided by shortage-induced price hikes. However, as wafer production capacity expands moderately and lead times are gradually normalized, dealers, agents, and small and medium-sized Fabless operators that originally increased their prices by 20-40% due to tight supply have naturally been under pressure to moderate pricing due to rapid accumulation of inventory. Therefore, in various application fields in 2H22, Approved Vendor List (AVL) Preferred vendors will continue to maintain a balanced supply and demand status while Non-Preferred vendors with a single product type and limited application fields may need to reduce prices to ensure volume and sell inventory. However, in general, demand for PMICs as a subset of all IC products is still relatively stable in 2H22.

For more information visit TrendForce