Localisation of chip manufacturing rising

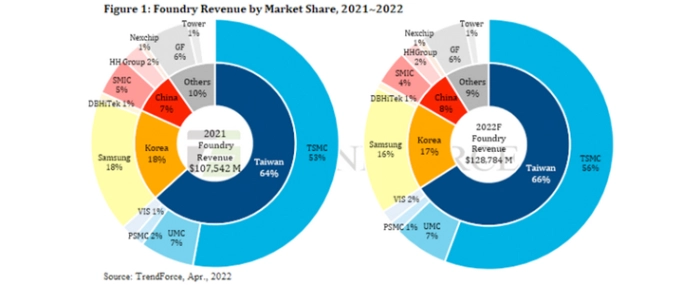

According to TrendForce, Taiwan is crucial to the global semiconductor supply chain, accounting for a 26% market share of semiconductor revenue in 2021, ranking second in the world. Its IC design and packaging & testing industries also account for a 27% and 20% global market share, ranking second and first in the world, respectively. Firmly in the pole position, Taiwan accounts for 64% of the foundry market.

In addition to TSMC possessing the most advanced process technology at this stage, foundries including UMC, Vanguard, and PSMC also have their own process advantages. Under the looming shadow of chip shortages caused by the pandemic and geopolitical turmoil in the past two years, various governments have quickly awakened to the fact that localisation of chip manufacturing is necessary to avoid being cut off from chip acquisition due to logistics difficulties or cross-border shipment bans. Taiwanese companies have ridden this wave to become partners that governments around the world are eager to invite to set up factories in various locales.

Currently, 8-inch and 12-inch foundries are dominated by 24 fabs in Taiwan, followed by China, South Korea, and the United States. Looking at new factories plans post 2021, Taiwan still accounts for the largest number of new fabs, including six new plants in progress, followed in activity by China and the United States, with plans for four and three new fabs, respectively. Due to the advantages and uniqueness of Taiwanese fabs in terms of advanced processes and certain special processes, they accepted invitations to set up plants in various countries, unlike non-Taiwanese foundries who largely still build fabs locally. Therefore, Taiwanese manufacturers have successively announced factory expansions at locations including the United States, China, Japan, and Singapore in addition to Taiwan in consideration of local client needs and technical cooperation.

The focus of Taiwan's key technologies and production expansion remains in Taiwan, accounting for 44% of global wafer production capacity by 2025

In 2022, Taiwan will account for approximately 48% of global 12-inch equivalent wafer foundry production capacity. Only looking at 12-inch wafer production capacity with more than 50% market share, the market share of advanced processes below 16nm (inclusive) will be as high as 61%. However, as Taiwanese manufacturers expand their production globally, TrendForce estimates that the market share held by Taiwan's local foundry capacity will drop slightly to 44% in 2025, of which the market share of 12-inch wafer capacity will fall to 47% and advanced manufacturing processes to approximately 58%. However, Taiwanese foundries’ recent production expansion plans remain focused on Taiwan including TSMC's most advanced N3 and N2 nodes, while companies such as UMC, Vanguard, and PSMC retain several new factory projects in Hsinchu, Miaoli, and Tainan.

TrendForce believes, since Taiwanese foundries have announced plans to build fabs in China, the United States, Japan, and Singapore, and foundries in numerous countries are also actively expanding production, Taiwan's market share of foundry capacity will drop slightly in 2025. However, semiconductor enclaves do not come together quickly. The integrity of a supply chain relies on the synergy among upstream (raw materials, equipment, and wafers), midstream (IP design services, IC design, manufacturing, and packaging and testing), and downstream (brands and distributors) sectors. Taiwan has advantages in talent, geographical convenience and industrial enclaves. Therefore, Taiwanese foundries still tend to focus on Taiwan for R&D and production expansion. Looking at the existing blueprint for production expansion, Taiwan will still control 44% of the world's foundry capacity by 2025 and as much as 58% of the world's capacity for advanced processes, continuing its dominance of the global semiconductor industry.

| Foundries | New fab location | |

| Taiwan | TSMC | Taiwan, US, Japan, China* |

| UMC | Taiwan*, Singapore* | |

| PSMC | Taiwan | |

| Vanguard | Taiwan | |

| China | SMIC | China |

| HuaHong | China | |

| Nexchip | China | |

| South Korea | Samsung | South Korea, US |

| Others | Globalfoundries | US, Singapore |

| Tower | Europe | |

*TSMC China, UMC Taiwan and UMC Singapore are expanding existing factory campuses not building new campuses