© TrendForce

Analysis |

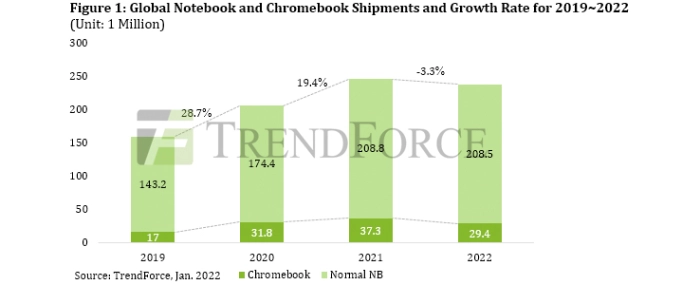

2022 notebooks shipments expected to reach 238M units

Due to the pandemic, laptops shipments reached a record high of 240 million units in 2021, according to TrendForce's investigations.

However, the market has been abuzz recently and, as the global population of the fully vaccinated has exceeded 50%, relevant demand driven by the pandemic is expected to gradually weaken. Shipment volume will decrease by 3.3% year-on-year, revised down slightly to 238 million units. Chromebooks will account for approximately 12.3% of shipment volume, though it accounted for approximately 15.2% in 2021. The momentum of shipments has slowed down significantly which indicates that demand derived from the economic effect of remote working and teaching has subsided.

TrendForce further states that Chromebook shipments declined sharply by nearly 50% in 2H21 due to the end of the Japanese government’s education tender and an increase in U.S. market share. However, thanks to the sequential return to the office of European and American companies driving a wave of commercial equipment replacement, shipments of commercial laptops have grown rapidly to make up for the shortfall. In turn, the shipment of laptops in 4Q21 hit the highest levels of the year, reaching 64.6 million units. In addition, due to the severe shortage of IC materials in mature processes, the backlog of orders extends to 1Q22 and the off-season is expected to be short. Compared with the average quarterly reduction of 15% in previous years, this year’s pullback is expected to be less than 10%.

It is worth noting that due to the shortage of container ships and issues with port congestion, shipping time has been prolonged, increasing by two to three times from manufacturers in mainland China to the United States compared to before the epidemic. Notebook brands have all been shipping in advance and the proportion of air freight shipments has increased. However, shipping time still exceeds expectations, which may flood the supply chain with duplicate orders from downstream customers, resulting in overstocked inventories and the risk of subsequent orders being canceled. In addition, the wave of commercial equipment replacement driven by a return to the office will be a major variable that will affect the demand for notebooks in 2022, resulting in near-term buzz in the market.

TrendForce indicated that in the past, due to factors such as fewer working days during the Lunar New Year Holiday and labor shortages in mainland China, brands would often require large OEMs to produce and ship before the Lunar New Year. This first quarter end-of-season surge will start from this month. Even though changes in end-user demand is unclear, March will see the beginning of a production surge to end the first quarter. If there is a major change in demand at that time, it may lead to an accumulation of distribution channel inventory, leading to a downward revision in demand, and a return to the normal equipment replacement cycle.