© TrendForce

Analysis |

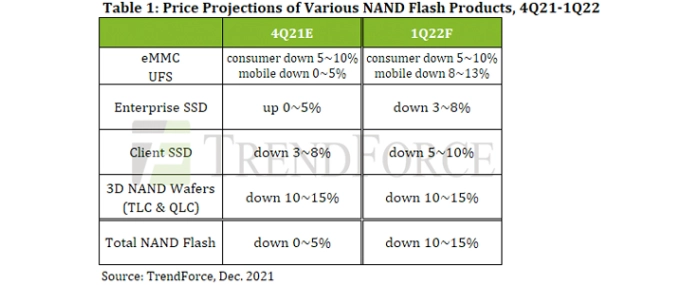

NAND Flash ASP to undergo 10-15% QoQ decline in 1Q22

Demand for NAND Flash products will undergo a noticeable and cyclical downward correction in 1Q22 as major smartphone brands wind down their procurement activities for the peak season and ODMs prepare for the New Year holidays, according to TrendForce’s latest investigations.

As such, the NAND Flash market will remain in an oversupply situation, with prices continuing to undergo downward corrections accordingly. However, PC OEMs have been reinstating certain orders for client SSDs since early November in response to improvements in the supply of upstream semiconductor materials. By fulfilling these orders, suppliers are able to keep their inventory level relatively low, meaning they are not under as much pressure as previously expected to reduce inventory by lowering prices. Taking these factors into account, TrendForce expects NAND Flash ASP to undergo a 10-15% QoQ decline in 1Q22, during which NAND Flash prices will experience the most noticeable declines compared to the other quarters in 2022.

Regarding the price trend of NAND Flash products across the whole 2021, TrendForce further indicates that suppliers have actively transitioned their output to higher-layer technologies, resulting in a bit supply growth that noticeably outpaces demand, though the tight supply of components such as controller ICs and PMICs has constrained the production of NAND Flash end-products. Hence, the decline in contract prices of NAND Flash products has not been as severe as previously expected. Moving ahead to 2022, however, the supply of relevant components is expected to gradually improve, so the market for various NAND Flash products will also likely shift towards a noticeable oversupply. As a result, prices of NAND Flash products will steadily decline before the arrival of the peak season in 3Q22.

Client SSD prices will maintain a downward trajectory in 1Q22, by about 5-10% QoQ

While PC OEMs aggressively push out shipments in 4Q21, demand also remains strong for commercial notebooks, in turn propelling the overall volume of notebook production for 4Q21 to 3Q21 levels, surpassing prior expectations. Moving into 1Q22, however, notebook demand from the consumer segment and education segment is expected to moderate, and client SSD buyers’ procurement activities for the quarter will therefore become more conservative. Suppliers, on the other hand, continue to shift the bulk of their client SSD output to 128L and higher layer products as they release the next generation of client SSDs to both capture market share and increase the consumption of these higher-layer products. The average storage capacity of client SSDs will expand to 567GB next year, with WD releasing QLC products alongside existing QLC manufacturers Intel and Micron, in turn intensifying suppliers’ pricing competition. TrendForce therefore expects contract prices of client SSDs to maintain their existing downward trajectory and undergo a 5-10% QoQ decline in 1Q22.

Prices will decrease by about 3-8% QoQ for PCIe enterprise SSDs but hold flat for SATA enterprise SSDs

North American hyperscalers saw their inventory levels rising throughout the fourth quarter as their production capacities for servers were negatively affected by component gaps. In addition, some of these issues are expected to persist in 1Q22, so server shipment for the 4Q21-1Q22 period will experience continued declines, thus putting downward pressure on the growth of enterprise SSD bit demand. As for the supply side, not only has the issue of insufficient PMIC production capacity become gradually alleviated, but hyperscalers have also cut down on their enterprise SSD orders somewhat due to their focus on inventory reduction. Hence, the production capacities for enterprise SSDs with PCIe interface have slowly returned to normal, and room for price negotiations with suppliers is also beginning to surface. Regarding enterprise SSDs with SATA interface, their supply has become relatively tight because manufacturers prioritize the production of high-density PCIe SSDs over SATA SSDs, which feature an older interface and lower density. As such, contract prices of SATA SSDs are unlikely to drop. For 1Q22, TrendForce forecasts an overall 3-8% QoQ decline in enterprise SSD prices, with contract prices of SATA enterprise SSDs mostly holding flat and prices of PCIe products declining by 3-8% QoQ.

eMMC prices will decrease by 5-10% QoQ

TVs, Chromebooks, and other categories of consumer products that carry eMMC solutions have been experiencing sluggish demand in the second half of this year as related subsidies and tenders in the US wind down. The seasonal fluctuations of the demand for consumer products will return to the pre-pandemic pattern next year. Chromebook production is forecasted to show a small rebound in 1Q22 and climb to the year’s peak in 2Q22 in accordance with the traditional seasonal pattern. Even so, the annual total Chromebook production for 2022 will still register a significant decline from the previous year. Turning to TV production, a QoQ decline is projected for 1Q22. Taking account of these demand-related projections, TrendForce expects the demand for eMMC solutions to be fairly weak in 1Q22. The overall production capacity for low-density 2D NAND Flash products has remained relatively constant. Some suppliers continue to scale back 2D NAND Flash production capacity, but they have slowed down the pace of reduction. Regarding the price trend of eMMC solutions, it is now adjusting downward to a stable level after the surge in 2Q21. TrendForce forecasts that contract prices of eMMC solutions will drop again by 5-10% QoQ for 1Q22.

UFS prices will decrease by 8-13% QoQ due to rising supply and falling demand

Component gaps in the upstream sections of the supply chain are still a serious issue affecting smartphone brands’ device production. Despite the contribution from the traditional peak shipment season in the second half of the year, the YoY growth rate of the total smartphone production in 2021 is expected to once again fall short of earlier projections. Looking ahead to 1Q22, Apple is expected to scale back its smartphone-related demand due to seasonality. This, in turn, will negatively affect NAND Flash suppliers’ bit shipments and further weaken mobile storage demand as a whole. The latest examination of product shipments from NAND Flash suppliers indicates that 1XX-L technologies are now mainstream, and 1YY-L technologies will gradually be adopted during 1H22. Micron has skipped 128L in its stacking technology migration and thereby advanced from 96L directly to 176L. To lower production cost and raise bit output, suppliers continue to increase the layer number of their 3D NAND technologies. This means that supply growth will further outstrip demand growth in 1Q22 as the off-season sets in. Hence, TrendForce forecasts that prices of UFS solutions will also register steeper QoQ declines of 8-13% for 1Q22.

NAND Flash wafer prices will decrease by 10-15% QoQ as oversupply becomes more severe

Sales of retail storage products such as UFDs and memory cards have been weak through this entire year. The promotional activities initiated by e-commerce companies for the special events and festivals near the end of the year have generated only a marginal amount of demand. Looking ahead to the early part of 2022, the demand for retail storage products is not expected to gain noticeable momentum before the arrival of Lunar New Year holiday. Additionally, the cryptocurrency market has been energetic, so the demand for graphics cards from cryptocurrency miners has been outpacing supply for the most part. This development has been impacting shipments of DIY PCs and thereby suppressing the demand for retail client SSDs during 2021. In sum, the aforementioned factors have significantly impeded the consumption of NAND Flash wafers. In view of the demand situation in the different application segments, NAND Flash suppliers will likely ramp up wafer shipments to prevent excess inventory. Moving into 1Q22, even if there is sustained demand for storage components in the PC and server segments, smartphone-related demand will shrink further and exacerbate the oversupply situation of the NAND Flash wafer market. TrendForce forecasts that contract prices of 3D NAND Flash wafers will fall by 10-15% QoQ. Among the various NAND Flash products, 3D NAND Flash wafers will suffer the sharpest price drop. It is worth noting that the growing gap between supply and demand is already exerting considerable pressure on some suppliers, so there is a possibility that suppliers could begin dumping products earlier than expected at the end of this year. Such development could help moderate the magnitude of the price downtrend in 1Q22.

[:]

For more information visit TrendForce