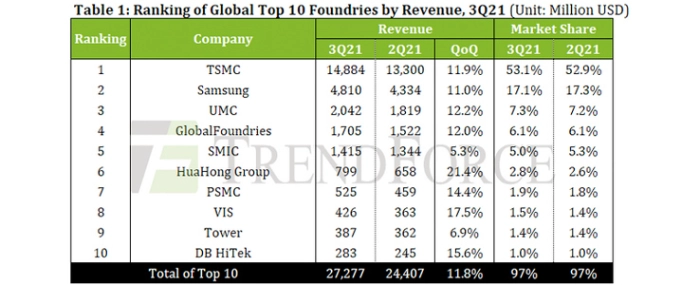

Foundry revenue rises by 12% QoQ for 3Q21, says TrendForce

Although the demand for end products related to the stay-at-home economy slowed down as many countries saw rising vaccination rates and were partially lifting social distancing restrictions, the decline in foundry orders from this source was more than offset by the traditional peak season for smartphones, according to TrendForce’s latest investigations.

At the same time, OEMs for notebook (laptop) computers, networking devices, automotive electronics, and IoT devices kept vigorously building up their inventories because the earlier capacity crunch in the foundry market was constraining them from reaching their shipment targets. Because of these developments, demand continued to outstrip supply in the foundry market during 3Q21. As for foundries, they have been gradually taking on new production capacity in the recent period and gaining from the ongoing rise in the ASP. Thanks to robust demand, new production capacity, and rising wafer prices, the quarterly total foundry revenue rose by 11.8% QoQ to reach a new record high of USD 27.28 billion for 3Q21. This result indicated nine consecutive quarters of revenue growth.

Top four foundries posted double-digit revenue growth for 3Q21 due to peak season for smartphones; SMIC’s revenue growth was slightly limited by restrictions imposed on its capacity expansions

TSMC raised its quarterly revenue by 11.9% QoQ to USD 14.88 billion as it benefited from the release of new iPhone models. The foundry remained firmly at the top of the ranking in 3Q21. Regarding TSMC’s revenue generation by node, the combined revenue share of the 7nm and 5nm nodes has already surpassed 50% and is still expanding thanks to continued demand for smartphone chips and HPC chips. Samsung raised its revenue by 11% QoQ to USD 4.81 billion for 3Q21 and sat firmly in second place. The revenue growth was attributed to several factors. First, the releases of new smartphone models during the second half of the year has spurred the demand for SoCs and DDIs. Second, fab Line S2 in Austin has returned to its normal level of revenue contribution following the recovery from the winter storm that struck Texas in the earlier part of this year. Third, fab Line S5 in Pyeongtaek has activated its newly added production capacity. And finally, the revenue result for 2Q21 was a low base for comparison and thus led to a rather impressive performance for 3Q21.

UMC made significant gains in 3Q21 because the activation of new production capacity for its 28/22nm nodes led to an increase in wafer input for OLED driver ICs and other components. This also caused a rise in its blended ASP. UMC’s revenue went up by 12.2% QoQ to USD 2.04 billion for 3Q21. With a growth rate that surpassed the top two ranking leaders, UMC retained third place by overtaking GlobalFoundries in the ranking for the first time in 1Q20, and its lead has been gradually widening since then. GlobalFoundries posted a QoQ increase of 12% in revenue to USD 1.71 billion for 3Q21 and kept fourth place in the ranking. To address the worldwide chip shortage, GlobalFoundries has announced a series of capacity expansions and greenfield projects this year. Existing plants including Fab1 in Dresden and Fab8 in Malta (which is a town in the state of New York) will take on new production capacity. New plants will also be built in Singapore and Malta. It is worth noting that the capacity expansions and greenfield projects that GlobalFoundries has revealed so far for this year will be financed via a public-private partnership model. GlobalFoundries will be leveraging funding from governments and advance payments from its clients to reduce the pressure of rising capital expenditure and ensure that the new production capacity will operate at a high utilization rate in the future.

SMIC increased its revenue by 5.3% QoQ to USD 1.42 billion for 3Q21 and was ranked fifth. Two reasons were behind the revenue growth. First, there is a stable level of demand for its PMICs, Wi-Fi chips, MCUs, and RFICs. Second, SMIC has been steadily raising wafer prices. It is also worth pointing out that SMIC has been adjusting its product mix and client base due to geopolitical factors. Growing consistently over the quarters, the share of Chinese clients in SMIC’s client base came to almost 70% in 3Q21. Under the impetus of the semiconductor policies of the Chinese government, SMIC will continue to give priority to the demand from domestic clients. Hence, the portion of foreign clients in its incoming orders will gradually shrink relative to that of domestic clients.

Second- and third-tier foundries posted higher revenue growth rates compared with first-tier counterparts because of strong demand for mature nodes

HuaHong Group posted a QoQ increase of 21.4% in revenue to USD 799 million for 3Q21, thereby taking sixth place in the ranking. HuaHong continues to raise its ASP as it production capacity is expected to be fully loaded through the whole 2021. This development, together with the successful capacity expansion undertaken at its Fab7 in Wuxi, contributed to the above-expected revenue result for the foundry. PSMC’s revenue growth continued to pick up pace in 3Q21 thanks to the general rise in wafer prices and the robust demand for the main categories of chip products (e.g., DDIs, PMICs, CIS, and power discretes such as MOSFETs and IGBTs). PSMC raised its quarterly revenue by 14.4% QoQ to USD 525 million and was ranked seventh.

After surpassing Tower Semiconductor in the ranking for the first time in 2Q21, VIS maintained its strong growth momentum by posting a QoQ increase of 17.5% in revenue to USD 426 million in 3Q21 on account of several factors. First, VIS increased its products shipments through capacity expansion. Furthermore, VIS was able to optimize its product mix and raise its ASP. It secured eighth place in the ranking. Occupying ninth place in the ranking, Tower Semiconductor’s performance exceeded expectations for 3Q21 with its revenue climbing 6.9% QoQ to USD 387 million. Tower’s revenue generation mainly benefited from the stable demand related to RF-SOI chips, industrial sensor chips, and PMICs.

Taking the tenth place in the ranking, DB HiTek registered a 15.6% QoQ increase in revenue to a record high of USD 283 million for 3Q21 because of the rising ASP. In the past year, DB HiTek kept its capacity utilization rate at almost 100%. To raise its overall output, the foundry has decided to focus its expansion efforts on its existing wafer production lines. As a result, its production capacity has been increasing slightly since 2Q21. The additional production capacity will effectively contribute to its revenue generation in 4Q21.

Moving into 4Q21, although foundries have undertaken various capacity expansions and greenfield projects, their new production capacity that has been activated this year is already completely booked. The new fabs that foundries have announced will need some time to get built and fully set up, so the chip shortage on the whole will unlikely ease off anytime soon. On the demand side, sales have weakened a bit for TVs and other end products associated with the stay-at-home economy. However, the hardware and infrastructure demand related to 5G, Wi-Fi 6, and IoT continues to gain momentum. Moreover, OEMs for consumer electronics are still stocking up on components in preparation for the year-end holiday sales. Based on the latest examination of incoming foundry orders, TrendForce finds that foundries will continue to operate at fully-loaded capacity. Due to the undersupply situation, the overall ASP of the foundry market has also been climbing. Meanwhile, foundries have been optimizing their product mixes to boost their financial performances. Taking account of this and other aforementioned developments, TrendForce believes that revenue growth will continue for the top 10 foundries in 4Q21. However, 4Q21 will also see more moderate growth compared with the previous quarter because there is a shortage of peripheral ICs made using mature process nodes. Additionally, demand has slacked a bit for some SoC products.