© Trendforce

Analysis |

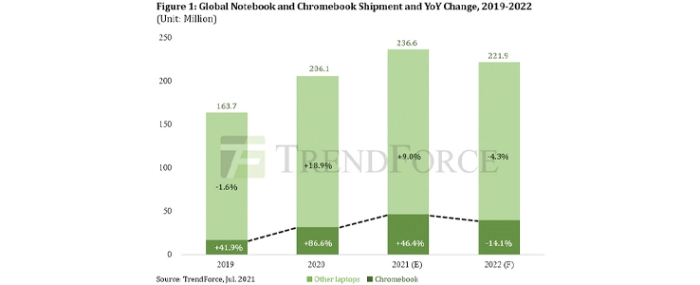

Annual notebook shipment likely to break records in 2021

While the stay-at-home economy generated high demand for notebook computers from distance learning and WFH applications last year, global notebook shipment for 2020 underwent a nearly 26% YoY increase, which represented a significant departure from the cyclical 3% YoY increase/decrease that had historically taken place each year, reports TrendForce.

The uptrend in notebook demand is expected to persist in 2021, during which notebook shipment will likely reach 236 million units, a 15% YoY increase. In particular, thanks to the surging demand for education notebooks, Chromebooks will become the primary growth driver in the notebook market. Regarding the shipment performance of various brands, Samsung and Apple will register the highest growths, with the former having Chromebooks account for nearly 50% of its total notebook shipment this year and the latter continuing to release MacBooks equipped with the M1 chip.

Chromebooks have been accounting for an increasingly high share in the notebook market in recent years, and Chromebook shipment is expected to reach a historical peak this year at 47 million units, a staggering 50% YoY growth. The vast majority (70%) of global Chromebook demand comes from the US, while Japan takes second place with 10%. However, the US education notebook market is gradually saturated with Chromebooks, and the general public has also been returning to physical workplaces and classrooms following the lifting of domestic restrictions. In addition, the Japanese GIGA School program, which equips student with computers and internet access, has notably slowed down its notebook procurement. The global demand for education notebooks will therefore slightly lose momentum in 2H21.

Regarding notebook brands, as Chromebooks occupy a relatively large allocation of notebook shipment by Acer and Samsung, the two companies are likely to bear the brunt of the education market’s downturn. TrendForce therefore believes that the Chromebook market’s growth going forward will mainly depend on regions outside the US as well as non-education applications.

Global demand for notebooks will decelerate in 2H21, with the bulk of the slowdown taking place in 4Q21

It should be pointed out that certain recent rumors claim that the demand for notebooks will decline in 2H21. This decline can be primarily attributed to the fact that notebook brands are increasingly finding Chromebooks’ low margins to be unprofitable, while 11.6-inch panels, which are used in 70% of all Chromebooks, have also skyrocketed in price, and certain semiconductor components are in shortage. In light of these factors, brands are starting to lower the share of Chromebooks in their overall notebook production for 2H21. TrendForce expects consumer demand in Europe and the US to gradually weaken in 3Q21. However, low inventory levels in the channel markets will still generate some upward momentum propelling the notebook market. Hence, quarterly notebook shipment in 3Q21 is expected to remain unchanged compared to 2Q21.

Furthermore, the pandemic has gradually been brought under control in Europe and the US due to increased vaccinations. Therefore, the slowdown of demand in the overall notebook market and in education sector bids will not come into force until 4Q21, during which notebook shipment is expected to reach 58 million units, a 3% QoQ decrease. At the same time, the fact that notebook manufacturers overbooked certain components, which subsequently resulted in additional inventory, will likely have implications in 4Q21 as well. Going forward, although notebook demand will likely slow in 2022, the normalization of the hybrid-work model as well as the recovering demand for business notebooks will provide some upward momentum for annual notebook shipment next year, which will reach 220 million units, a minor downward correction of 6% YoY.