© TrendForce

Analysis |

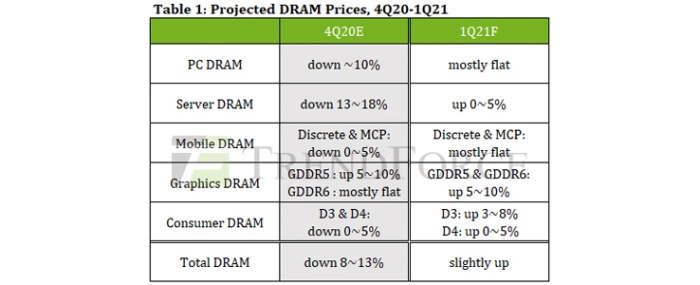

DRAM ASP to recover from decline in 1Q21

The DRAM market exhibits a healthier and more balanced supply/demand relationship compared with the NAND Flash market because of its oligopolistic structure, says to TrendForce.

The percentage distribution of DRAM supply bits by application currently shows that PC DRAM accounts for 13%, server DRAM 34%, mobile DRAM 40%, graphics DRAM 5%, and consumer DRAM (or specialty DRAM) 8%. Looking ahead to 1Q21, the DRAM market by then will have gone through an inventory adjustment period of slightly more than two quarters. Memory buyers will also be more willing to stock up because they want to reduce the risk of future price hikes. Therefore, DRAM prices on the whole will be constrained from falling further. The overall ASP of DRAM products is now forecasted to stay generally flat or slightly up for 1Q21.

PC DRAM prices will be mostly constant as notebook (NB) manufacturers increase procurement activities in response to soaring NB shipment

Regarding the NB market and its influence on PC DRAM demand, total NB production is expected to decline by 9% QoQ to reach 52.7 million units in 1Q20 due to the traditional off-season and the reduction of work days caused by the celebration of the Lunar New year, as well as the fact that 4Q20 was a relatively high base period for comparison. On the other hand, 2020 has been a decent year for PC OEMs with the annual total NB shipments projected to grow by 20%. This means that PC OEMs will be holding a relatively low level of DRAM inventory in 1Q21 (i.e., four to five weeks). To meet and sustain the demand for NBs, PC OEMs will probably continue with their inventory building in the short term. Regarding the supply of PC DRAM, the three dominant DRAM suppliers (Samsung, SK Hynix, and Micron) have not significantly raised bit output for nearly two quarters. Furthermore, they have been allocating more production capacity to mobile DRAM since the end of 3Q20 due to the recent demand upswing in that application segment. Hence, production capacity has tightened for both PC DRAM and server DRAM. Moving to 1Q21, PC DRAM supply is not expected to grow noticeably, while DRAM demand from PC OEMs will remain healthy. TrendForce therefore believes that the downward trajectory of the ASP of PC DRAM products will be increasingly difficult to maintain.

Owing to the power outage at Micron's Taiwan-based fab and the overall constrained production capacity, server DRAM price forecast for 1Q21 has been revised from relatively flat to slightly increasing

Demand-wise, the first quarter is the traditional off-season for OEMs of electronic products. As such, server procurement tends to be at its lowest level in the first quarter as well when compared with the following three quarters of the year. However, there is the distinct possibility that customers in the data center segment will build up their inventories ahead of time during 1Q21 because they anticipate a general price rally later on. Supply-wise, the three dominant suppliers have been assigning more production capacity to mobile DRAM since this September as this application segment has recently experienced a demand recovery. The shift in their product mixes is having the same effect on the supply of both server DRAM and PC DRAM, so the supply bit growth of server DRAM will be very limited in 1Q21.

There is a growing consensus among memory buyers that stocking up early is the best strategy as prices are close to bottoming out and the DRAM industry’s production capacity has become more limited. In 1Q21, seasonal headwinds will affect shipments for OEMs of electronic products. However, the demand side of the DRAM market is expected to be very active. Memory buyers will likely stock up ahead of time because the price rebound could happen at any moment, especially after the power outage of MTTW (Micron’s Taiwan-based DRAM fab). The downtrend in DRAM prices are now led by a few product lines. With the recent demand recovery for mobile DRAM and the continuation of strong demand for PC DRAM, the decline in prices of server DRAM products will probably taper off sooner than previously anticipated. Hence, DRAM prices are now projected to formally begin their next cyclical upturn in 1Q21.

Mobile DRAM prices will for the most part trend flat, but smaller smartphone brands may see a slight increase in contract prices

On the matter of demand, smartphone brands that are competing with Huawei in Greater China will continue to aggressively extend their component inventories and ramp up device production in 1Q21 as they intend to capitalize on the latest round of US sanctions against Huawei. Therefore, the quarterly total smartphone production for 1Q21 will not register a QoQ drop that exceeds 10% as typically happened for the first quarters of the past years due to the effect of the traditional off-season. Instead, the QoQ decline is now forecasted to come to just around 6% with the total volume coming to nearly 330 million units. On the matter of supply, as mentioned above, the three dominant suppliers have not noticeably increased bit output and will remain passive in this respect during 1Q21. Furthermore, some mobile DRAM orders intended for 4Q20 will not be fulfilled until 1Q21. Consequently, supply is going to be rather tight for mobile DRAM products.

On the whole, TrendForce forecasts that contract prices of mobile DRAM products in 1Q21 will stay around the same level as in 4Q20. The major smartphone brands that can secure special deals and procure in large quantities should be able to keep prices relatively stable when negotiating contracts for 1Q21. For the smaller smartphone brands, they could experience slight QoQ hikes in prices (i.e., within 3%) since they are competing with the major brands for the tightening supply. Also, DRAM suppliers tend to give a lower priority to the smaller brands. This is because they do not provide the same kind of demand as the major brands in terms of quantity, and the memory solutions that they need are relatively low in density.

Graphics DRAM prices are expected to exhibit a minor uptrend, with GDDR6 prices up by about 5-10%

The releases of new graphics cards, game consoles, and ASIC miners remain the three major drivers of graphics DRAM demand, leading to an uptrend in graphics DRAM ASP ahead of other DRAM products. TrendForce therefore expects that prices of mainstream GDDR6 memory will increase by about 5-10% QoQ in 1Q21 on account of high demand. On the other hand, most suppliers currently manufacture graphics DRAM with the 20nm or 1Xnm processes, which are relatively mature processes. However, rising demand for mobile DRAM, which is also mass-produced with the 1Xnm process, has resulted in constricted production capacities for graphics DRAM. As a result, suppliers’ fulfillment rate for graphics DRAM will remain subpar even in 1Q21, and the price hike of graphics DRAM will be the most prominent out of all DRAM product categories.

Consumer DRAM prices are expected to remain mostly still while DDR3 prices lead the uptick due to reduced supply

The gradual recovery of demand for TVs, STBs, and networking products has galvanized a corresponding increase in the demand for low-density DDR3 products (DDR3 1/2/4Gb and below). Although consumer (or specialty) DRAM quotes for many small and medium clients with short-term procurement contracts have already risen ahead of time, quotes for tier-one clients are still mostly trending flat. In terms of supply, SK Hynix has officially ceased DDR3 2Gb production, while Samsung is gradually shifting the old DRAM manufacturing processes at its Line 13 fab to CIS manufacturing instead. As Korean suppliers continue to lower their DDR3 output, DDR3 prices are likely to show an early uptick compared to other consumer DRAM products. Likewise, DDR4 consumer DRAMs are somewhat resilient to price drops since they are closely linked with mainstream DDR4 PC and server DRAMs and thereby share the same pricing trend.