© TrendForce

Analysis |

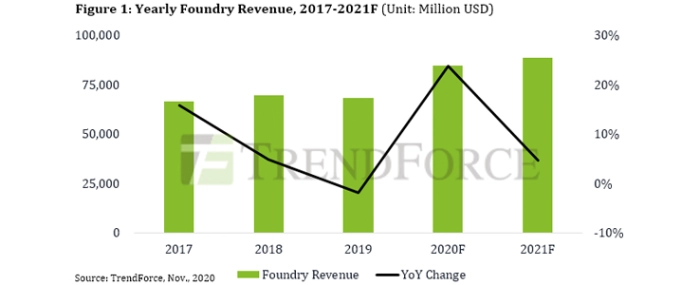

Foundry revenue expected to increase by 23.8% YoY in 2020

Despite the COVID-19 pandemic’s negative impact on the global economy, several emergent trends, such as WFH, distance education, rising 5G smartphone penetration, and strong component demand from telecom infrastructure build-out, have resulted in a bullish semiconductor market against economic headwinds, according to TrendForce.

Global foundry revenue is projected to undergo a 23.8% increase YoY in 2020, the highest percentage in 10 years.

Based on the status of various foundries’ client orders, TrendForce expects the current tight supply of wafer capacity to persist at least until 1H21. With regards to advanced processes below and including the 10nm node, both TSMC’s and Samsung’s wafer capacities are currently close to fully loaded. As well, since 4/3nm processes are expected to arrive on the market in 2021 and 2022, respectively, ASML’s EUV machines have now become a scarce commodity highly sought after by various foundries, as these machines are a mission-critical component in foundries’ capacity expansion for advanced processes. On the other hand, wafer capacities for mature processes above and including the 28nm node are gradually exhibiting a tight supply, given the growing demand for current applications (CIS, SDDI, RF front-end, TV, WiFi, Bluetooth, and TWS chips) and emerging applications (WiFi 6 chips and AI memory heterogeneous integration).

Notably, 8-inch wafer capacity has been in severe shortage since 2H19, as almost no suppliers still currently produce 8-inch semiconductor equipment, meaning the price for such equipment has now skyrocketed. Moreover, since 8-inch wafer prices are relatively low in comparison to 12-inch wafer prices, foundries generally find it cost-ineffective to expand their 8-inch capacities. However, as it is significantly more cost-effective to manufacture products such as PMIC and LDDI in 8-inch fabs, foundries may deem it unnecessary to transition to 12-inch fabs or even advanced nodes for these products. Demand for PMICs, used in smartphones and base stations, has undergone an exponential growth with the arrival of the 5G era, further exacerbating the existing tight supply of 8-inch wafer capacity. Therefore, although manufacturing operations for some products may gradually transition from 8-inch fabs to 12-inch fabs, the shortage of 8-inch wafer capacities is unlikely to be alleviated in the short run.

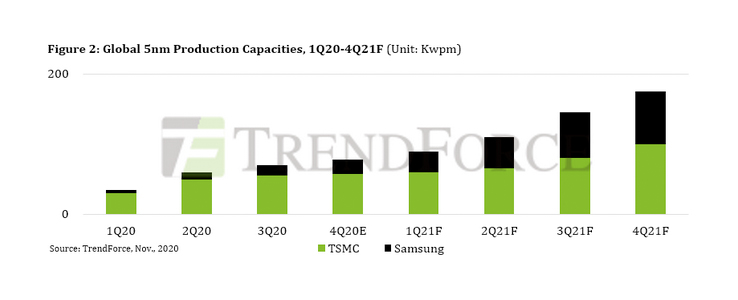

TSMC’s aggressive 5nm capacity expansion will allow the company to capture nearly 60% of advanced process market by the end of 2021

With regards to the 5nm process technology, which is the most advanced node at the moment and which entered mass production in early 2020, Apple remains the sole client utilizing TSMC’s 5nm process after U.S. sanctions prohibited chip shipment to Huawei subsidiary HiSilicon. As such, despite Apple’s wafer input orders for its in-house-developed Mac CPU and FPGA accelerators used in servers, these wafer inputs are unable to completely make up for the leftover excess wafer capacities following HiSilicon’s departure. TSMC’s 5nm capacity utilization rate for 2H20 is therefore estimated to fall within the 85-90% range. Looking ahead to 2021, in addition to Apple’s 5nm+ wafer input for the A15 Bionic SoC, trial production will also kick off for a small batch of AMD 5nm Zen 4 CPUs. These products will help maintain TSMC’s 5nm capacity utilization rate at an 85-90% range next year.

It should be pointed out that, from late-2021 to 2022, MediaTek, Nvidia, and Qualcomm will kick-start their 5/4nm mass production, while AMD will ramp up its Zen 4 CPU manufacturing. Moreover, the first batch of outsourced 5nm Intel CPUs is also expected to enter production in 2022. The enormous wafer demand from these companies have led TSMC to begin expanding its 5nm capacity. Furthermore, based on current data, Apple is highly likely to continue manufacturing its A16 SoCs with the 4nm process technology (a process shrink of the 5nm node). This may lead TSMC to further expand its 5nm capacity at that time to fulfill high demand from clients. Likewise, Samsung is also planning to expand its 5nm capacity in 2021 in response to continuing manufacturing orders from Nvidia for GeForce GPUs based on the Hopper architecture, in addition to the Qualcomm Snapdragon 885 and Samsung’s own Exynos flagship SoCs. Even so, Samsung is expected to trail TSMC by about 20% in terms of 5nm capacity.

In light of the aforementioned situations, UMC and GlobalFoundries have in recent years successively bowed out of the race for advanced process development. Excluding SMIC, which is embroiled in U.S. sanctions-related complications, only TSMC and Samsung remain in the 7nm (and below) market. With regards to the client retention of foundries, Samsung is actively expanding its 5nm capacity at its new Pyeongtaek fab after receiving major orders from Nvidia. However, as Qualcomm will likely adopt TSMC’s 4nm process technology for Snapdragon 895 manufacturing, Samsung may have only Nvidia and Samsung (LSI) remaining as its major 5nm clients. Conversely, TSMC is likely to welcome Intel as a CPU manufacturing client, in addition to the existing clientele of Apple, AMD, MediaTek, Nvidia, and Qualcomm. TrendForce believes that demand for TSMC’s 5nm process technology will remain relatively strong and stable, and the 2H22 mass production of the 3nm process will further increase TSMC’s market share.

For more information visit © Trendforce

For more information visit © Trendforce