© SEMI

Analysis |

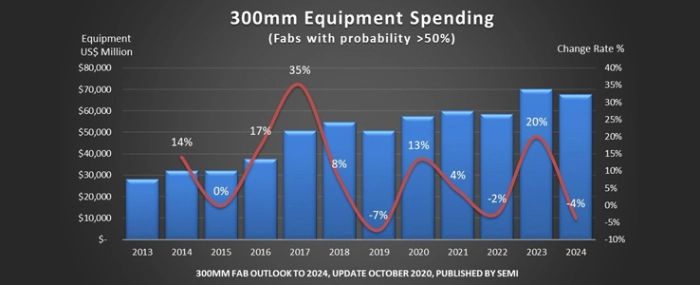

300mm fab spending to boom through 2023 with two record highs

Powering the growth is rising demand for cloud services, servers, laptops, gaming and healthcare technology. Fast-evolving technologies such as 5G, IoT, automotive, AI and machine learning that continue to fuel demand for greater connectivity, large data centers and big data are also behind the increase.

"The COVID-19 pandemic is accelerating a digital transformation sweeping across nearly every industry imaginable to reshape the way we work and live," said Ajit Manocha, SEMI president and CEO. "The projected record spending and 38 new fabs reinforce the role of semiconductors as the bedrock of leading-edge technologies that are driving this transformation and promise to help solve some of the world's greatest challenges."

Growth in semiconductor fab investments will continue in 2021 but at a slower rate of 4% YoY. Mirroring previous industry cycles, the report also predicts a mild slowdown in 2022 and another slight downturn in 2024 following a USD 70 billion record high in 2023.

Adding 38 New 300mm Fabs

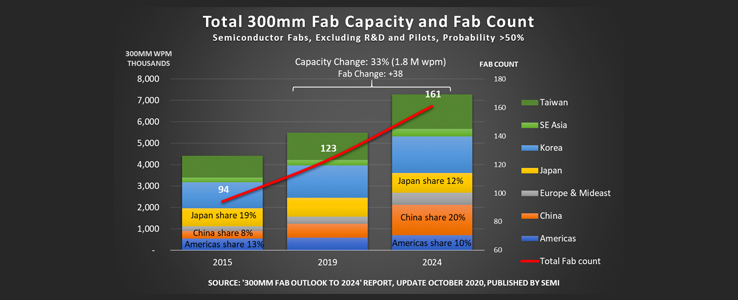

The SEMI 300mm Fab Outlook to 2024 shows the chip industry adding at least 38 new 300mm volume fabs from 2020 to 2024, a conservative projection that does not factor in low-probability or rumored fab projects. During the same period, per-month fab capacity will grow by about 1.8 million wafers to reach over 7 million. See figure 2.

Under a high-probability project forecast, the industry will add at least 38 new 300mm volume fabs from 2019 to 2024. Taiwan will add 11 volume fabs and China eight to account for half of the total. The chip industry will command 161 300mm volume fabs by 2024. Capacity and Spending Growth by Region

China will rapidly increase its global share of 300mm capacity, from 8% in 2015 to 20% in 2024, reaching 1.5 million 300mm wpm in the final year of the reporting period. While non-Chinese companies will account for a substantial portion of that growth, Chinese-owned organizations are accelerating their capacity investments. These companies will represent about 43% of China's fab capacity in 2020, a proportion expected to reach 50% by 2022 and 60% by 2024.

Japan's share of 300mm installed capacity continues to trend downward, from 19% in 2015 to 12% in 2024. The Americas' share is also ticking lower, from 13% in 2015 to a projected 10% in 2024.

The biggest regional spenders will be Korea, with investments between USD 15 billion and USD 19 billion, followed by Taiwan, which will pour between USD 14 billion and USD 17 billion into 300mm fabs, and then China, with between USD 11 billion and USD 13 billion in investments.

Regions spending less will see the steepest increases in investments between 2020 to 2024. Europe/Mideast will lead the pack with impressive 164% growth, followed by Southeast Asia at 59%, Americas at 35%, and Japan at 20%.

Spending Growth by Product Sector

Memory accounts for the bulk of the increase in 300mm fab spending. Actual and forecast investments show a steady rise in the upper single digits for each year from 2020 to 2023, with a stronger increase of 10% in store for 2024.

DRAM and 3D NAND contributions to 300mm fab spending will be uneven from 2020 to 2024. Investments for logic/MPU, however, will see steady improvement from 2021 to 2023. Power-related devices will be the standout sector in 300mm fab investments, with over 200% growth in 2021 and double-digit increases in 2022 and 2023.

Capacity and Spending Growth by Region

China will rapidly increase its global share of 300mm capacity, from 8% in 2015 to 20% in 2024, reaching 1.5 million 300mm wpm in the final year of the reporting period. While non-Chinese companies will account for a substantial portion of that growth, Chinese-owned organizations are accelerating their capacity investments. These companies will represent about 43% of China's fab capacity in 2020, a proportion expected to reach 50% by 2022 and 60% by 2024.

Japan's share of 300mm installed capacity continues to trend downward, from 19% in 2015 to 12% in 2024. The Americas' share is also ticking lower, from 13% in 2015 to a projected 10% in 2024.

The biggest regional spenders will be Korea, with investments between USD 15 billion and USD 19 billion, followed by Taiwan, which will pour between USD 14 billion and USD 17 billion into 300mm fabs, and then China, with between USD 11 billion and USD 13 billion in investments.

Regions spending less will see the steepest increases in investments between 2020 to 2024. Europe/Mideast will lead the pack with impressive 164% growth, followed by Southeast Asia at 59%, Americas at 35%, and Japan at 20%.

Spending Growth by Product Sector

Memory accounts for the bulk of the increase in 300mm fab spending. Actual and forecast investments show a steady rise in the upper single digits for each year from 2020 to 2023, with a stronger increase of 10% in store for 2024.

DRAM and 3D NAND contributions to 300mm fab spending will be uneven from 2020 to 2024. Investments for logic/MPU, however, will see steady improvement from 2021 to 2023. Power-related devices will be the standout sector in 300mm fab investments, with over 200% growth in 2021 and double-digit increases in 2022 and 2023.

Images and data courtesy of © SEMI

Capacity and Spending Growth by Region

China will rapidly increase its global share of 300mm capacity, from 8% in 2015 to 20% in 2024, reaching 1.5 million 300mm wpm in the final year of the reporting period. While non-Chinese companies will account for a substantial portion of that growth, Chinese-owned organizations are accelerating their capacity investments. These companies will represent about 43% of China's fab capacity in 2020, a proportion expected to reach 50% by 2022 and 60% by 2024.

Japan's share of 300mm installed capacity continues to trend downward, from 19% in 2015 to 12% in 2024. The Americas' share is also ticking lower, from 13% in 2015 to a projected 10% in 2024.

The biggest regional spenders will be Korea, with investments between USD 15 billion and USD 19 billion, followed by Taiwan, which will pour between USD 14 billion and USD 17 billion into 300mm fabs, and then China, with between USD 11 billion and USD 13 billion in investments.

Regions spending less will see the steepest increases in investments between 2020 to 2024. Europe/Mideast will lead the pack with impressive 164% growth, followed by Southeast Asia at 59%, Americas at 35%, and Japan at 20%.

Spending Growth by Product Sector

Memory accounts for the bulk of the increase in 300mm fab spending. Actual and forecast investments show a steady rise in the upper single digits for each year from 2020 to 2023, with a stronger increase of 10% in store for 2024.

DRAM and 3D NAND contributions to 300mm fab spending will be uneven from 2020 to 2024. Investments for logic/MPU, however, will see steady improvement from 2021 to 2023. Power-related devices will be the standout sector in 300mm fab investments, with over 200% growth in 2021 and double-digit increases in 2022 and 2023.

Images and data courtesy of © SEMI