© Trendforce

Analysis |

Sluggish server production in 4Q20 to be joined by decline in server DRAM prices

Due to server ODMs’ higher-than-expected inventory of server barebones in 3Q20, additional server orders from the ODMs’ clients came to a screeching halt, therefore resulting in a QoQ decrease in overall server orders for the quarter, according to TrendForce’s latest investigations.

As ODMs gradually destock their inventories of server barebones in 4Q20, data center operators are expected to step up their server procurement activities as well, albeit to a far lesser extent than 2Q20. However, given the excess inventory of server barebones, one to two quarters are needed to correct this situation, meaning ODMs will be unlikely to restart their procurement of server DRAM and server components until late 2020 or early 2021. In light of the fact that server manufacturers still hold a relatively high inventory of server DRAM, TrendForce is now forecasting a 13-18% QoQ decline in server DRAM prices for 4Q20.

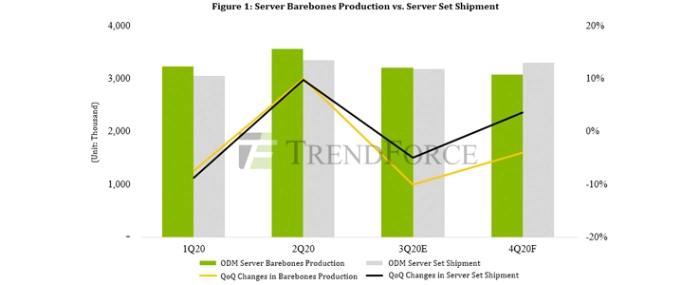

Momentum of ODM server shipment is expected to slightly improve in 4Q20, though shipment still falls short of 2Q20 figures

TrendForce’s demand analysis indicates that enterprises have massively cut down on their server procurement in light of market uncertainties brought about by the COVID-19 pandemic. Most of these enterprises have also transitioned their infrastructure spending from CAPEX to OPEX, in turn suspending some of their existing server orders.

Despite the recovery of labor back to normal levels at overseas ODM assembly sites at the end of June, server barebones production and server set (whole server) shipments for 3Q20 are expected to decline by 10% QoQ and 4.9% QoQ, respectively, thus falling short of previous forecasts. Looking ahead to the fourth quarter, the shipment performance of server barebones is expected to benefit somewhat from data centers’ procurement efforts, while ODMs gradually destock their inventory of server barebones, but the resultant QoQ growth of server shipment in 4Q20 is projected to be lower than 2Q20 figures.

Huawei’s server DRAM procurement ahead of time is unable to reverse the downswing of server DRAM prices, which is expected to further decline in 4Q20

DRAM suppliers have been entering the server DRAM market in droves owing to the fact that server DRAM is the most profitable product category out of all DRAM offerings. As a result, the supply of server DRAM has been on a steady upswing. However, server manufacturers have been slowing down their server production since 3Q20, leading to an excess inventory of server DRAM. This, combined with their reluctance to source more server DRAM from suppliers due to an anticipated price drop, has led to an oversupply situation in the server DRAM market. On the other hand, Huawei has been very aggressive in procuring memory products during the recent two weeks as it wants to extend its component inventories as far as it can before the latest export control rules imposed by the US government come into effect after mid-September. Server DRAM modules are among the items that the Chinese technology conglomerate are stocking up on, and most of these upside orders have been directed to the major DRAM suppliers based in South Korea.

Even so, the server DRAM segment is still experiencing significant oversupply, while the demand side is also affected by the fact that buyers including data centers are dealing with high inventory. Therefore, contract prices of server DRAM products continue to descent to new lows. Even though prices for 4Q20 contracts have yet to be finalized, the overall trend suggests that the decline in contract prices of 32GB server DRAM modules may likely widen to a QoQ drop of about 15% or more. In view of the market situation, TrendForce has formally widened the forecast of QoQ decline in server DRAM prices to 13-18% compared with the earlier projection of 10-15%.