© IHS Markit

Analysis |

Copper-based Wire & Cable index highest in almost five years

"Both events are temporary, though they do tighten the market and support higher prices, at least for a time."

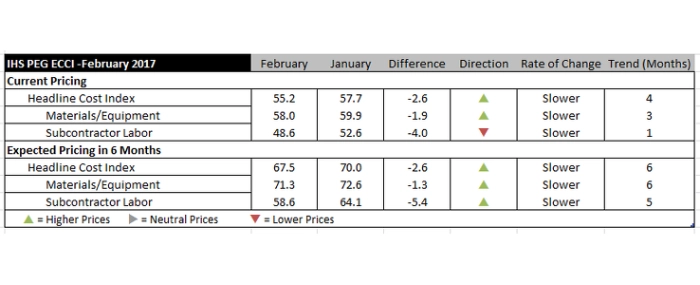

Construction costs rose again in February, recording the fourth consecutive month of price recovery, according to IHS Markit and the Procurement Executives Group (PEG). The headline IHS PEG Engineering and Construction Cost Index registered 55.2 in February, down from 57.7 in January. Strength was evident for materials markets, though for labor markets, the headline index tipped below the neutral point.

The materials/equipment price index came in at 58.0 in February, with the materials sub-index showing rising prices in 10 of the 12 categories tracked. Ocean freight from Europe to the U.S. recorded another month of falling prices and electrical equipment prices were flat. Of the remaining 10 categories, the index figure for exchangers, alloy steel pipe, and wire and cable rose compared to January. The copper-based wire and cable index experienced the highest escalation compared to January. The last time the copper index registered this level was back in March 2012.

"Copper prices are reacting to the closure of two of the world's largest mines: Grasberg in Indonesia, because of a dispute with government over its export permit, and Escondida in Chile, because of a strike,” said John Mothersole, research director at IHS Pricing and Purchasing. “Both events are temporary, though they do tighten the market and support higher prices, at least for a time.”

The subcontractor labor index fell in February. The index came in at 48.6, falling back to its October 2016 level. Regionally, weakness was recorded in the U.S. Midwest and Western Canada. Labor costs rose in the Northeastern United States and Eastern Canada; in the U.S. South and U.S. West, costs remained the same compared to January.

The six-month headline expectations index recorded another month of increasing prices. The index moved down slightly from 70.0 in January to 67.5 this month. The materials/equipment index stayed positive, at 71.3, marginally lower than the 72.6 recorded in January. Despite the slight give-back, this figure affirms widespread expectations of higher future prices. Every component showed rising prices, with steel related indexes leading the way. Subcontractor labor price expectations came in at 58.6 in February, lower than the 64.1 recorded in January. Labor costs are expected rise in all regions of the United States and Eastern Canada; they are expected to be soft in Western Canada.

In the survey comments, respondents have noted no shortages in supply of materials. Proposal activity has registered an uptick in the recent months, and participants are expressing cautious optimism for 2017.