European PCB revenues rise 2.4% as industry shrinks

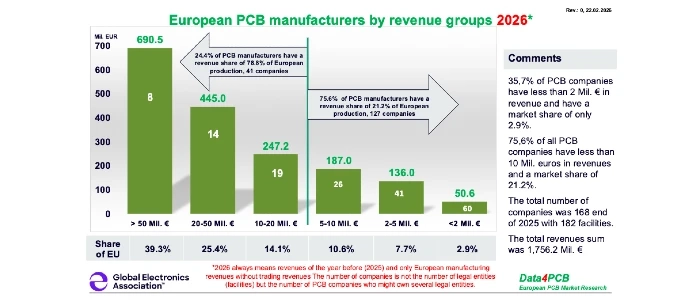

European PCB manufacturing increased by 2.4% in 2025, while the global PCB market expanded by more than 11%, according to Data4PCB. At the same time, 11 manufacturers exited the market, reducing the European PCB base to 168 companies operating 182 facilities.

The figures indicate that Europe’s structural decline remains intact despite marginal annual growth.

On a USD basis, output appeared to rise by 6.9%, largely due to the dollar’s depreciation against the euro, the report states. In 2026, one additional company is expected to enter the count, including TLT-PCB.

By product type, rigid-flex and flexible multilayer boards recorded positive trends, while other segments showed limited movement. In end markets, automotive declined significantly, as anticipated, and medical electronics also contracted. Industrial electronics remained the largest segment, characterised by high-mix, low-volume production, with Germany accounting for approximately 46% of PCB output for this sector. The industry segment grew by more than EUR 43 million in 2025.

Defence electronics posted the strongest growth in absolute terms, increasing by 23% or more than EUR 50 million. Air and space electronics, reported separately at the European level, rose by 15%, corresponding to nearly EUR 23 million. France accounted for around 41% of the defence electronics segment, followed by the UK with more than 28%. Italy led air and space electronics with 33.5%, ahead of France and Belgium.

Medical electronics remained concentrated in Switzerland and Austria, which together represent more than 70% of this segment.

Germany recorded its third consecutive annual decline in PCB manufacturing revenues and has lost more than 27% since 2022. Over the same period, Austria and Switzerland expanded by more than 6%, while France and Belgium grew by 32% and the UK by nearly 22%. Italy increased by 15% between 2022 and 2025, but lost two manufacturers last year.

Like Germany, Central and Eastern Europe declined for a third consecutive year – down 12.5% compared with 2022, driven by a reduction in companies from 47 to 33, primarily smaller producers.

According to Data4PCB, larger manufacturers are increasingly focusing on specialised markets such as air, space and defence or advanced technologies including HDI, flex and rigid-flex multilayers. Smaller firms face sustained price competition from Far East suppliers.

Data4PCB forecasts that the number of European PCB manufacturers could halve by 2035 if current conditions persist. The report cites EU import duties on base materials, combined with tariff-free imports of finished PCBs from Asia, as structural challenges. It also calls for the establishment of a secure European supply chain for system-critical products based on locally manufactured PCBs.