© IC Insights

Components |

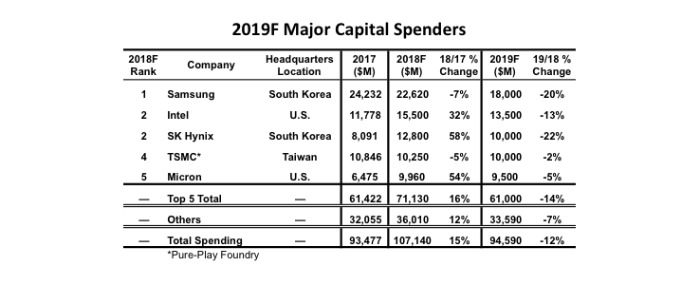

Samsung's USD 46.8bn match Intel and TSMC's combined USD 48.4bn

Samsung is expected to have the largest capex budget of any IC supplier again in 2018. After spending USD 24.2 billion for semiconductor capex in 2017, IC Insights forecasts that Samsung’s spending will edge slightly downward, but remain at a very strong level of USD 22.6 billion in 2018.

If it comes in at this amount, Samsung’s two-year semiconductor capital spending will be an astounding USD 46.8 billion.

Samsung’s semiconductor capital outlays from 2010, the first year the company spent more than USD 10 billion in semiconductor capex, through 2016 averaged USD 12.0 billion per year. However, after spending USD 11.3 billion in 2016, the company more than doubled its 2017 capex budget. The fact that Samsung’s continued its strong capex spending in 2018 is just as impressive.

IC Insights believes that Samsung’s massive spending outlays in 2017 and 2018 will have repercussions far into the future. One effect that has already begun is a period of overcapacity in the 3D NAND flash market. This overcapacity situation is due not only to Samsung’s huge spending for 3D NAND flash, but also from spending by competitors (e.g., SK Hynix, Micron, Toshiba, Intel, etc.) that attempt to keep pace in this market segment.

With the DRAM and NAND flash memory markets showing strong growth through the first three quarters of 2018, SK Hynix ramped up its capital spending this year. In 1Q18, SK Hynix said that it intended to increase its capex spending by “at least 30%” this year. In the November Update, IC Insights forecasts that SK Hynix will see a 58% surge in its semi capex spending. The increased spending by SK Hynix this year is focused primarily on bringing new capacity online at two of its large memory fabs—M15, a 3D NAND flash fab in Cheongju, South Korea, and the expansion of its huge DRAM fab in Wuxi, China. The Cheongju fab is being pushed to open before the end of this year. The Wuxi fab is also targeted to open by the end of this year, a few months earlier than its original start date of early 2019.

Overall, IC Insights’ now forecasts total semiconductor industry capital spending will climb 15% to $107.1 billion this year, the first time that annual industry capex is expected to top $100.0 billion. Following the industry-wide growth this year, semiconductor capex is expected to decline 12% in 2019 (Figure 2).

Given that the current softness in the memory market is expected to extend into at least the first half of next year, the combined capital spending by the three largest memory suppliers—Samsung, SK Hynix, and Micron—is forecast to drop from USD 45.4 billion in 2018 to USD 37.5 billion in 2019, a decline of 17%.

In total, the top five spenders, which are expected to represent 66% of total outlays this year, are forecast to cut their capital spending by 14% in 2019 with the remaining semiconductor industry companies registering a 7% decline.

.png)