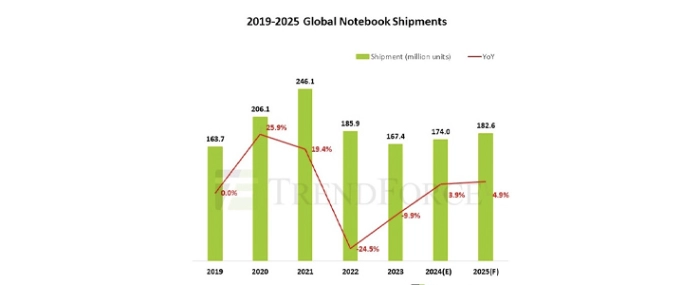

Global notebook shipments expected to grow by 4.9% in 2025

TrendForce reports that the global notebook market in 2024 is projected to recover at a moderate pace, hindered by high interest rates and geopolitical uncertainties.

Annual shipments are forecast to reach 174 million units, marking a 3.9% YoY increase. Looking ahead to 2025, reduced political uncertainty following the U.S. presidential election and the Federal Reserve’s rate cuts in September 2024 are expected to stimulate capital flow. Combined with the end-of-service for Windows 10 and demand for commercial device upgrades, global notebook shipments are predicted to grow by 4.9% to 183 million units in 2025.

TrendForce notes that notebooks remain primarily productivity tools, with shipment growth driven largely by deferred replacement demand. The impact of AI-integrated notebooks on the overall market remains limited for now. However, AI features are expected to naturally integrate into notebook specifications as brands gradually incorporate them, resulting in a steady rise in the penetration rates of AI notebooks.

In terms of market segmentation, commercial notebooks faced headwinds in 2024 due to global layoffs and economic and political instability, leading to a more cautious demand environment. However, as these negative factors subside and rate cuts improve capital liquidity, the commercial market is expected to recover in 2025, with annual shipment growth surpassing 7%.

Conversely, the consumer market is driven by aggressive promotions in 2024, with entry-level models dominating sales, particularly in North America. For 2025, TrendForce predicts a more stable consumer market, with brands refocusing on high-value, high-margin models. While consumer notebook shipment growth may slow to 3%, the product mix will see significant optimisation.

Chromebook demand in 2024 has been bolstered by educational procurement in North America and growing demand from emerging markets. In 2025, Japan’s GIGA School 2.0 initiative is expected to further drive Chromebook momentum, with shipment growth accelerating to 8% and sustaining a strong growth trajectory.

The global notebook market remains closely tied to U.S. trade policies, particularly the potential impact of heightened import tariffs under the “America First” policies introduced by the Trump administration. These measures could influence domestic demand in the U.S., pending the new administration’s implementation of such policies.

China remains the dominant manufacturing hub for global notebook production, accounting for approximately 89% of total capacity. While some ODMs are expanding production lines in Vietnam, Thailand, India, and Mexico, establishing a fully integrated supply chain ecosystem in these regions will require time. Additionally, there will likely be a transition period between the announcement and enforcement of related policies.

Consequently, TrendForce notes that the 2025 shipment forecast for notebooks may be subject to adjustments based on evolving market conditions.

For more information visit TrendForce.