China retains market advantage in battery development

On May 14, the White House announced significant tariff increases on Chinese EVs and batteries. EV tariffs will jump from 25% to 100%, and battery tariffs will rise from 7.5% to 25%. TrendForce posits that Chinese EVs account for less than 2% of the US EV market, making the actual impact of these tariff hikes minimal.

However, the increased battery tariffs are expected to raise EV production costs for US automakers. This could complicate efforts to reduce overall vehicle costs and incentivize consumer purchases.

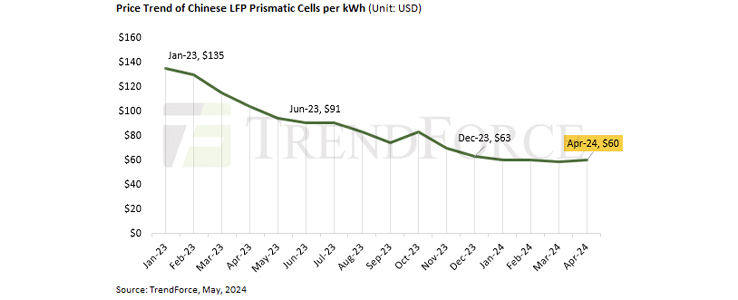

TrendForce research indicates that Chinese LFP batteries already have a price advantage; the cost of Chinese batteries remains lower than US-manufactured ones—which are more than double in price—even with increased tariffs. Additionally, a recent temporary exemption in the IRA regarding critical minerals from a foreign entity of concern (FEOC) for battery production highlights the US’s continued reliance on Chinese batteries. US automakers still require more time to transition away from Chinese suppliers.

In the short term, increased tariffs and IRA regulations underscore the growing geopolitical influence on the EV industry. US automakers can mitigate these impacts by partnering with established battery makers from Japan and South Korea or investing in solid-state battery technology. In the long term, scaling up EV sales to achieve economies of scale is crucial for reducing battery costs. Traditional US automakers must decide between focusing on fuel vehicles or EVs to avoid resource misallocation. One pertinent example is BYD, which ceased production of fuel vehicles and, within two years, surpassed Tesla in annual sales (combining pure electric and plug-in hybrid vehicles) to become the world’s largest EV producer.

Moreover, the ability to produce LFP batteries domestically is critical for the US. While most US EVs currently use NCM batteries, market reports suggest Tesla has established an LFP battery production line in its Sparks, Nevada factory, with an estimated capacity of 10 GWh—sufficient for approximately 130,000 vehicles with 75 kWh batteries.

LG Energy Solution (LGES) is also setting up an LFP production line in Arizona, which is slated for mass production by 2026. Other companies, including Gotion, American Battery Factory Inc., FREYR Battery, and Our Next Energy, have plans to establish LFP production lines. However, LFP batteries are expected to be primarily used in ESS rather than exclusively in the EV sector.

For more information visit TrendForce.