Global semiconductor manufacturing industry poised for 2024 recovery

The global semiconductor manufacturing industry recovery is taking hold with electronics and IC sales increasing in the final quarter of 2023 and more growth projected for 2024, SEMI and TechInsights report.

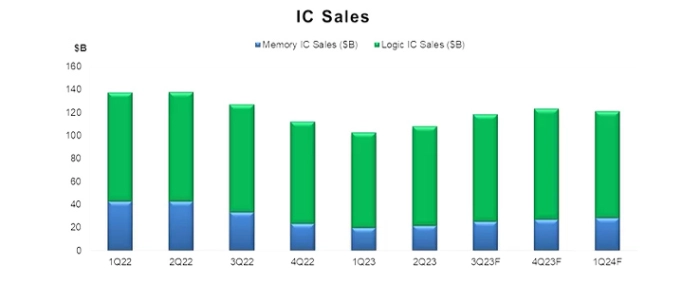

In Q4 2023, electronics sales edged up 1% Year-over-Year (YoY), marking the first annual rise since the second half of 2022, and growth is projected to continue in Q1 2024 with a 3% YoY increase. At the same time, IC sales returned to growth with a 10% YoY jump in Q4 2023 as demand improved and inventories started to normalise. IC sales are forecast to strengthen in Q1 2024 with 18% YoY growth.

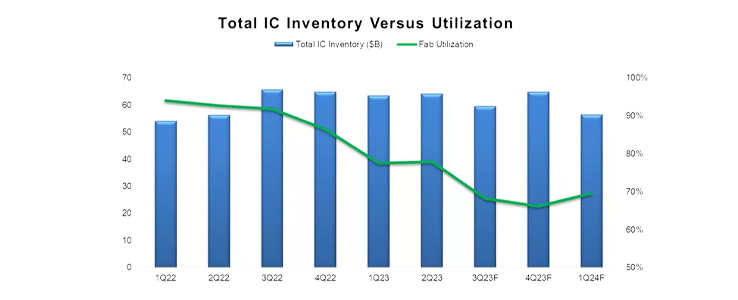

Capital expenditures and fab utilisation rates are expected to see a mild recovery starting in Q1 2024 after significant declines in the second half of 2023.

In Q1 2024, Memory CapEx is projected to increase 9% Quarter-on-Quarter (QoQ) and 10% YoY, while Non-Memory CapEx is on track to climb 16% during the quarter but remain at lower levels than recorded in Q1 2023. Fab utilization rates saw a modest improvement from 66% in Q4 2023 to 70% in Q1 2024. Meanwhile, fab capacity grew 1.3% in Q4 2023 and is projected to match those gains in Q1 2024.

Equipment billings in 2023 surpassed projections though growth is expected to be muted in the first half of 2024 mostly due to seasonality.

“The electronics and IC markets are recovering from a slump in 2023 with growth expected this year,” said Clark Tseng, Senior Director of Market Intelligence at SEMI. “Although fab utilisation remains low at the moment, improvement as 2024 unfolds is anticipated.”

Boris Metodiev, Director of Market Analysis at TechInsights, says that semiconductor demand is well on its way in the recovery.

“While the overall IC market is growing this year, slowing automotive and industrial markets are hampering the analog expansion. AI will be a huge catalyst for leading-edge semiconductors as the technology proliferates from the cloud to the edge. At the same time, geopolitics is driving excess capacity at the trailing edge.”