Global notebook market to rebound in 2024

TrendForce reports that the second quarter revealed notebook inventory channels displaying healthy levels. Both North America and Asia-Pacific regions are demonstrating a healthy appetite for mid and low-tier consumer models.

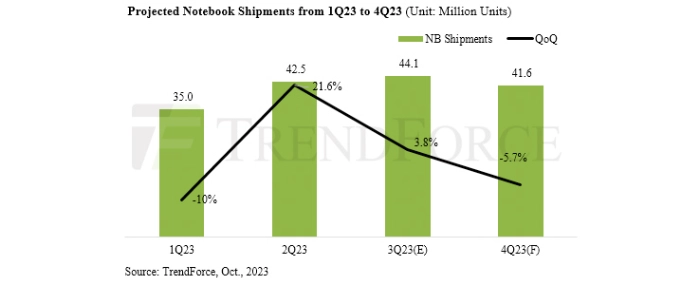

This isn’t just a race to restock; it’s a strategic move to gear up for the anticipated back-to-school wave in the third quarter. And here’s the zinger – just as Google prepped to roll out its licensing fees, Chromebook shipments hit a peak. This surge propelled Q2 notebook shipments to 42.52 million units, marking a 21.6% quarterly leap. However, a look at the overall picture reveals a total of 77.5 million units shipped in the first half of the year—down 23.5% YoY.

TrendForce further points out that for 2H23, growth momentum is anchored in the purchasing power of end consumers. However, with the economic outlook of the two major notebook markets – the US and Europe – shrouded in uncertainty, the typical seasonal purchasing demand is muted. What’s more, some of this demand was already met in Q2. As a result, Q3 notebook shipments are forecast to witness a moderate growth of 3.8%, tallying up to 44.13 million units. Annual notebook shipments are projected to hit 163 million units, marking a YoY decline of 12.2%.

Gearing up for 2024, the tech horizon looks promising. As market inventories align with healthier metrics and anticipated inflationary pressures begin to stabilise, global notebook shipments are poised for a potential rebound. Yet, it’s not all roses. With the global consumer environment still feeling the pinch, even as demand gradually ticks up, the market hasn’t flashed strong bullish signs just yet. TrendForce projects an annual growth rate hovering between 2–5% for 2024, pushing shipments slightly above pre-pandemic levels. Post inventory adjustments, the broader market is set for a gentle recovery. However, all eyes remain on the twin giants of consumer markets—China and the US—to gauge if we can indeed anticipate a more robust shipment surge.

In the latter half of the year, the absence of seasonal market activity paired with subdued demand has not only impacted corporate profitability but also posed challenges for the upcoming year’s budgeting. Concurrently, the rise of AI and the emphasis on its foundational infrastructure might sideline IT expenditures. While Windows 10 is set to end its support in October 2025, it’s anticipated to spur a wave of business device upgrades starting in 2024. However, TrendForce believes that based on the demand for commercial notebooks, the momentum and urgency of this upgrade wave might be delayed and subdued, making significant shipment growth less probable.

On the consumer demand front, when examining the world’s economic powerhouses, China faces challenges due to a subdued economic and employment environment, casting a somewhat pessimistic view on its market development. In contrast, the US saw a robust rebound in demand in 2023, but anticipations hint at tempered growth in 2024. Europe, after undergoing a two-year demand recalibration, might witness a consumer resurgence in the latter half, should the broader economic climate brighten. Finally, Southeast Asia, buoyed by a burgeoning consumer segment, forecasts upward-trending shipments, indicating a modest growth in consumer-focused devices.

For more information visit TrendForce.