Suppliers amp up production, HBM bit supply projected to soar

TrendForce highlights in its latest report that memory suppliers are boosting their production capacity in response to escalating orders from NVIDIA and CSPs for their in-house designed chips.

These efforts include the expansion of TSV production lines to increase HBM output. Forecasts based on current production plans from suppliers indicate a remarkable 105% annual increase in HBM bit supply by 2024. However, due to the time required for TSV expansion, which encompasses equipment delivery and testing (9 to 12 months), the majority of HBM capacity is expected to materialize by 2Q24.

TrendForce analysis indicates that 2023 to 2024 will be pivotal years for AI development, triggering substantial demand for AI Training chips and thereby boosting HBM utilisation. However, as the focus pivots to Inference, the annual growth rate for AI Training chips and HBM is expected to taper off slightly. The imminent boom in HBM production has presented suppliers with a difficult situation: they will need to strike a balance between meeting customer demand to expand market share and avoiding a surplus due to overproduction. Another concern is the potential risk of overbooking, as buyers, anticipating an HBM shortage, might inflate their demand.

HBM3 is slated to considerably elevate HBM revenue in 2024 with its superior ASP

The HBM market in 2022 was marked by sufficient supply. However, an explosive surge in AI demand in 2023 has prompted clients to place advance orders, stretching suppliers to their capacity limits. Looking ahead to 2024, TrendForce forecasts that due to aggressive expansion by suppliers, the HBM sufficiency ratio will rise from -2.4% to 0.6% in 2024.

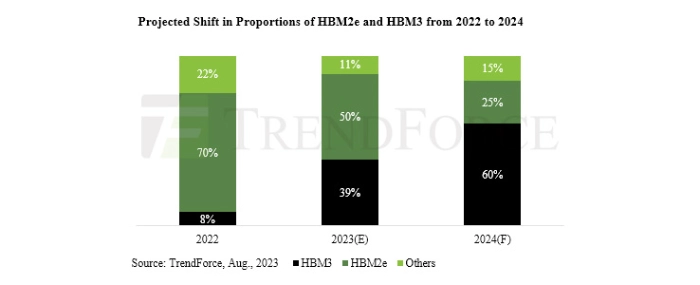

TrendForce believes that the primary demand is shifting from HBM2e to HBM3 in 2023, with an anticipated demand ratio of approximately 50% and 39%, respectively. As an increasing number of chips adopting HBM3 hit the market, demand in 2024 will heavily lean toward HBM3 and eclipse HBM2e with a projected share of 60%. This expected surge—coupled with a higher ASP—is likely to trigger a significant increase in HBM revenue next year.

SK hynix currently holds the lead in HBM3 production, serving as the principal supplier for NVIDIA’s server GPUs. Samsung, on the other hand, is focusing on satisfying orders from other CSPs. The gap in market share between Samsung and SK hynix is expected to narrow significantly this year due to an increasing number of orders for Samsung from CSPs. Both firms are predicted to command similar shares in the HBM market sometime between 2023 to 2024—collectively occupying around 95%. However, variations in shipment performance may arise across different quarters due to their distinct customer bases. Micron, which has focused mainly on HBM3e development, may witness a slight decrease in market share in the next two years due to the aggressive expansion plans of these two South Korean manufacturers.

| Company | 2022 | 2023 (E) | 2024 (F) |

| Sk Hynix | 50% | 46~49% | 47~49% |

| Samsung | 40% | 46~49% | 47~49% |

| Micron | 10% | 4~6% | 3~5% |

| Total | 100% | 100% | 100% |

Prices for older HBM generations are expected to drop in 2024, while HBM3 prices may remain steady

From a long-term perspective, TrendForce notes that the ASP of HBM products gradually decreases year on year. Given HBM’s high-profit nature and a unit price far exceeding other types of DRAM products, suppliers aim to incrementally reduce prices to stimulate customer demand, leading to a price decline for HBM2e and HBM2 in 2023.

Even though suppliers have yet to finalize their pricing strategies for 2024, TrendForce doesn’t rule out the possibility of further price reductions for HBM2 and HBM2e products, given a significant improvement in the overall HBM supply and suppliers’ endeavors to broaden their market shares. Meanwhile, HBM3 prices are forecast to stay consistent with 2023. Owing to its significantly higher ASP compared to HBM2e and HBM2, HBM3 is poised to bolster suppliers’ HBM revenue, potentially propelling total HBM revenue to a whopping US$8.9 billion in 2024—a 127% YoY increase.

For more information visit Trendforce.