Global notebook shipments on the rebound

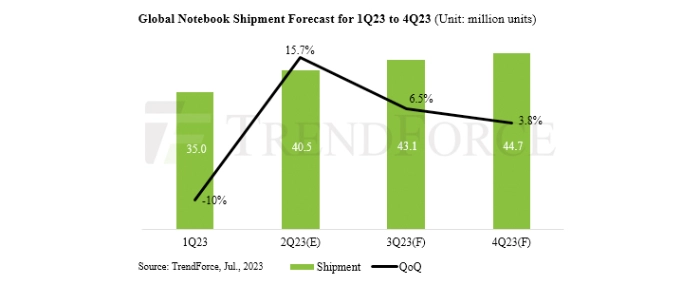

TrendForce has predicted a noticeable recovery in the global notebook market for 2Q23. Shipments are projected to hit 40.45 million units – a QoQ increase of 15.7%.

This marks a pivotal turnaround after six consecutive quarters of decline. However, despite this growth, shipments are still down by 11.6% YoY. TrendForce expects this upward trend to persist into the third quarter, estimating global notebook shipments to reach 43.08 million units, albeit at a decelerated growth rate of 6.5%.

Notebook brands were primarily focused on reducing excess terminal inventory in 1Q23, which led to slower procurement and subsequently impacted ODM sell-in sales. However, as Q2 unfolds and inventory levels of finished products and components start to stabilise, supply chain pressures should ease, triggering a wave of restocking demand. This trend is expected to extend into Q3—a season typically characterised by robust sales due to back-to-school demand and shopping promotions, further stimulating inventory demand and fostering further growth in global notebook shipments.

Entry-level consumer models and Chromebook demand show early recovery in Q2

Although the notebook market has yet to fully recover, TrendForce reports that since March, restocking orders for certain notebook models have started to surface in several markets, including North America, Europe, and Southeast Asia. Ongoing economic constraints, which limit consumers’ disposable income, mean that restocking demand is primarily for low-to-mid-range and budget-friendly consumer models, predominantly those that retail between USD 400 and USD 600.

Meanwhile, after seven quarters of adjustment, Chromebook tender orders have begun to emerge in North America, Indonesia, and India. Additionally, with UNICEF’s support, educational reconstruction has also been emerging in Ukraine. Notably, Google’s decision to initiate a Chromebook licensing fee from July 1, 2023, could potentially impact Chromebooks’ competitiveness in the entry-level market. Nevertheless, this impending fee has catalyzed a boost in overall Chromebook shipments for 2Q23 as brands attempt to pre-emptively circumvent these costs.

TrendForce asserts that global notebook shipments likely hit their lowest point in Q1, and Q2 should see a more distinct quarterly growth. Nonetheless, a widening consumer price gap could dampen this market momentum, leading to a forecasted slowdown in growth from Q3 onwards. Given the persistent economic downturn, TrendForce expects the notebook market to remain in a consolidation phase throughout 2023, with an estimated total shipment volume of about 163 million units—a YoY reduction of 12.2%.

For more information visit TrendForce.