TV panel demand heats up, Gen 5+ LCD capacity utilisation rate to rise to 77%

The panel market has become imbalanced due to the continuous addition of new production capacities and a significant slowdown in demand post-pandemic. In response, panel makers have effectively reduced inventory by lowering capacity utilisation rates to below 70% in 2H22.

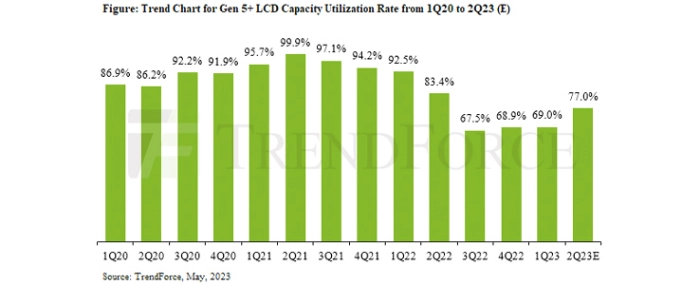

A recent surge in demand for TV panels – coupled with increasing TV prices – is expected to push utilisation rates for Gen 5+ LCD production lines (calculated by area) up to 77% in 2Q23. However, after LG Display scales down its P6, P7, and Guangzhou LCD production lines, total output will still be much lower than the same period last year, according to TrendForce latest research.

TrendForce further emphasises that the current uptick in utilisation rates is driven by actual demand for orders. Consequently, it is believed that a healthy supply-demand ratio in the LCD market will persist in 2Q23 with rising utilisation rates. Panel makers must continue to exercise caution and control and adopt quick response strategies throughout 2H23 in order to maintain market balance.

TV panel inventory has reached a healthy level after more than half a year of adjusting production. In 1Q23, Chinese brands started stocking up early for the 618 Shopping Festival, driving up demand and causing TV panel prices to rise ahead of schedule. This upward trend is expected to continue into 2Q23. TrendForce reports that over 90% of Gen 10.x production lines are being devoted to TV panels, and it’s predicted that their capacity utilisation rates are expected to grow by more than 10 percentage points QoQ, reaching up to 83.2%.

The pandemic led to surging demand for LCD monitors and notebook panels, forcing most panel makers to reallocate a portion of their TV production capacity to IT projects. Despite a resurgence in demand for TV panels contributing to the growth of Gen 8.x utilisation rates, the absence of significant growth in demand for IT products limited the increase in utilisation rates to 7.6 percentage points, resulting in a 79.4% rate when compared to 1Q23. For Gen 7.5 and older production lines, the utilisation rate is projected to climb to 60% due to growing demand in the smartphone panel repair market and a slight increase in demand for IT panels compared to 1Q23. Nevertheless, TrendForce maintains a conservative outlook on growth.

For more information visit TrendForce.