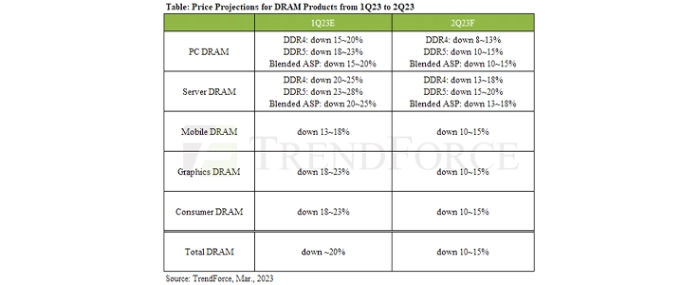

Decline in DRAM ASP narrows to 10~15% in 2Q23

TrendForce reports that several suppliers, such as Micron and SK hynix, have started scaling back DRAM production. The ASP of DRAM plunged 20% in 1Q23, and this price decline is predicted to slow down to 10~15% next quarter.

It’s uncertain whether or not demand will recover in 2H23. Therefore, the ASP of DRAM has continued to fall as inventory levels are high from the suppliers’ side, and prices will only rebound if there is a significant decrease in production.

PC DRAM: Purchase quantity from buyers has fallen drastically over the past three quarters; buyers have around 9~13 weeks of PC DRAM stock remaining. Despite suppliers having already cut production in the PC DRAM segment, DDR4 8 GB module is still likely to fall by more than 10% in 2Q23. There is a possibility that PC OEMs may purchase more DRAM because prices have been down to a relatively low level, but it is still under observation whether or not this can mitigate the inventory overstock situation from the suppliers’ side. TrendForce predicts the ASP of PC DRAM will fall between 10~15%.

Server DRAM: Demand for server DRAM from OEMs and cloud service providers has been sluggish due to inventory adjustments. In addition, consumer demand looks less than promising, prompting suppliers to increase the ratio of server DRAMs in their product mixes. However, this resulted in a massive inventory pile-up during 1Q23. While most suppliers have lowered their capacity utilization rates, their efforts have yet to make a noticeable impact on declining prices. TrendForce predicts that the ASP of server DRAM will fall 13~18% in 2Q23.

Mobile DRAM: The DRAM inventories of smartphone brands have returned to a relatively healthy level. However, these brands have mostly adopted a conservative plan of action for smartphone production, which means that buyer demand for mobile DRAM will be constrained in 2Q23. As a result, suppliers are under a great deal of pressure to sell off as much stock as possible. Even with cutbacks being made in mobile DRAM production, reversing their current overstock will continue to be a challenge for these companies. TrendForce predicts the ASP of mobile DRAM to continue falling as we move into 2Q23. Nevertheless, there is a possibility that the decline will shrink to 10~15%.

Graphics DRAM: Buyers have been stocking up on graphics DRAM rather conservatively, while even AI has failed to make a considerable impact on demand. Taking a mainstream product, the GDDR6 16 Gb, for example, TrendForce predicts ASP will fall 10~15% QoQ in 2Q23 due to constrained demand. The DRAM industry is currently in the midst of transitioning from 8 to 16 Gb; Samsung’s GDDR6 8 Gb will reach its EOL at the end of the year. Beginning 2024, SK hynix will be the only company still offering 8 Gb products. Rolling back production could finally present an opportunity for the price of GDDR6 8 Gb to stop fluctuating aggressively.

Consumer DRAM: Demand for networking devices has been relatively stable. However, buyers have dialed back their procurement activities as of late given that existing orders have been completed. These buyers appear to have conservative estimations of the growth potential of network-related demand this year, and the application market, which includes television, will be unable to support demand for the consumer DRAM market. Supply continues to outpace demand even as suppliers reduce their production considerably. TrendForce predicts that the ASP of consumer DRAM will fall 10~15% in 2Q23.

For more information visit TrendForce