Notebook shipments projected to reach a 10-Year low in 1Q23

Due to the various major events that affected the global economy and politics, the overall demand for consumer electronics made a sharp downward turn in 2022, and global shipments of notebook (laptop) computers began to fall over the quarters.

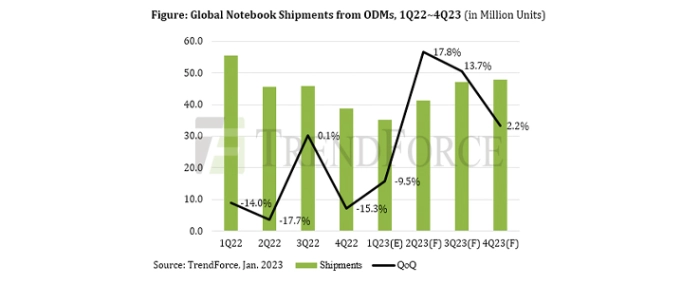

TrendForce’s latest analysis finds that global shipments of notebook computers (from ODMs) reached just around 186 million units for 2022, showing a YoY drop of 24.5%. As for 2023, the outlook on the performance of the notebook computer market remains uncertain at this moment. TrendForce expects the YoY decline to moderate to about 7.8%, but shipments are projected to total only 171 million units.

Because market demand was anemic in 4Q22, promotional activities related to the traditional year-end peak season did not generate a lot of sales momentum. Looking at regional markets, notebook brands (PC OEMs) slashed prices in the US and China, but their sales results still did not meet expectations. This development was mainly attributed to factors such as high inflation suppressing consumers’ disposable income. Since the sales results for 4Q22 were lacklustre, efforts to get rid of the existing stockpile of whole devices might continue through 2Q23. Furthermore, order placements from channels are going to be much more restrained.

Additionally, the Lunar New Year holiday for 2023 is going to arrive earlier compared with the previous years, and notebook brands have anticipated that the course of the ongoing COVID-19 outbreaks in China will become a huge market variable after the holiday. Besides low demand visibility, whether device shipments will be impacted by another round of pandemic-induced component shortages has also been a major concern. In view of this situation, notebook brands have raised inventory for their popular device models. Moreover, they completed shipments for some orders ahead of schedule before the end of 2022. Because of these actions, global notebook shipments are forecast to drop by 9.5% QoQ to 35.1 million units for 1Q23. This projection is a 10-year low for the first-quarter result.

The supply chain is shifting, and US-based brands are the main driving force behind ODMs’ relocation efforts

The continuation of the US-China trade dispute has led to increasing geopolitical tensions across the globe. Hence, the major electronics brands have revamped their supply chain strategies in recent years. Among them, US-based brands have been the most aggressive in relocating device production and finding alternative sources of component supply. While political and economic pressures are the well-recognised factors that propel US-based brands to change their strategies, these major brands themselves also have the scale to persuade the rest of the participants in the supply chain to follow their lead. According to TrendForce’s latest observations, strategic considerations about future geopolitical developments could lead to two models for notebook production located outside China.

The first model will be centered on Vietnam as the country has both geographical and demographical advantages. Materials and components from China can be quickly transported to assembly plants in Vietnam. At the same time, Vietnam has a relatively young and low-cost labor pool. The demographical advantage might be the more significant incentive for brands and ODMs to set up shop there. Presently, ODMs such as Compal, Wistron, and Foxconn have begun to build notebook assembly lines in Vietnam in response to the requests made by their clients from the US. Additionally, among the US-based notebook brands, the leader in commercial models has set the target of raising the share of its device shipments from Vietnam to 20% for 2023. Moreover, this brand will reduce the share of its device shipments from China to just 20~30% by 2027.

Likewise, another US-based electronics brand that has gained substantial brand influence with its in-house SOCs has decided to establish a complete manufacturing cluster for its products in Vietnam. From that country, this brand will ship not only notebook computers but also earphones, smartphones, etc. TrendForce estimates that Vietnam will account for 10% of its notebook computer shipments in 2023.

As for the second model, it involves setting up assembly lines and raising device production in or near a sizable consumer market. One US-based brand (that is separate from the two that are mentioned above) will be raising device production volume at its assembly lines in Mexico in order to better serve the North American market. Moreover, the same brand is seeking partners in India so as to set up local assembly lines that manufacture products targeting local consumers. Since foreign manufacturers that set up shop in India will benefit from a substantial tax incentive, this brand will be able to attain a considerable price advantage as well. Data from the UN indicate that India’s population will surpass that of China within 2023 to become the world’s most populous country. Hence, electronics brands around the world are preparing to make the Indian market their main battleground. A potential development that the market looks forward to in the near future is whether India can replicate the same kind of model that has existed in China for outsourcing and selling electronics.

For more information, visit TrendForce.