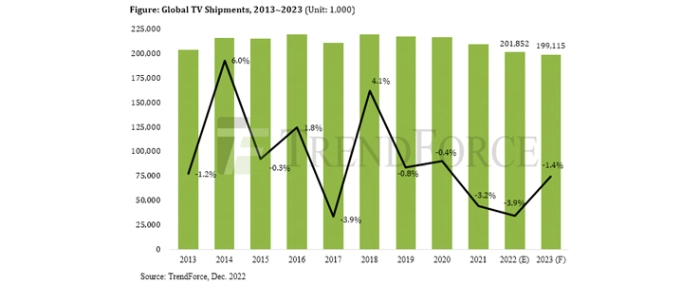

Global TV shipments are projected to drop by 3.9% YoY

TrendForce’s latest research finds that TV brands’ promotional activities related to China’s Singles’ Day were helped by the steep decline in display panel prices.

With panel prices reaching a very low level, TV brands were able to cut their prices further so as to raise shipments of whole TV sets during the promotional period. On the other hand, the major international brands have come into the second half of this year with a high level of inventory as their sales performances were weaker than expected during the first half. In order to effectively consume the existing inventory, TV brands have significantly corrected down the panel procurement quantity for 2H22. As a result, TrendForce now estimates that global TV shipments in 2H22 will reach 109 million units, reflecting a YoY decline of 2.7%. Global TV shipments during the whole 2022 are currently projected to total 202 million units, showing YoY decline of 3.9%. This annual shipment figure represents a decade low.

This year, the TV market has seen a continuous decline in shipments. Fortunately, there has also been a sharp drop in prices of large-sized panels. Furthermore, freight transportation costs have fallen by more than 50%. Thus, TV brands have been able to vigorously promote large-sized products, and the average size of TVs has also risen by 1.4 inches to 56 inches.

TrendForce further points out that moving into 2023, supply will remain fairly plentiful for TV panels. With the chance of a substantial rally in panel prices being extremely low, brands should feel an easing of cost pressure and have more flexibility when it comes to large-scale promotional activities. However, the IMF has downgraded its global economic growth forecast for 2023 to 2.7%. Moreover, the US, the Eurozone, and China as the world’s three largest regional economies will continue to experience stagnation.

Regarding the ongoing inflation, it has recently started to ease a bit in Europe and the US, but the major regional consumer markets on the whole will continue be under its pressure. Because of these factors, TrendForce believes the growth momentum of TV shipments will be severely constrained next year. Global TV shipments are currently forecasted to again register a YoY decline for 2023, falling by 1.4% to 199 million units.

Contrasting Results for Year-End Holiday Promotions: TV Sales in China During Singles’ Day Period Fell by Nearly 10% YoY, Whereas Black Friday Period in North America Saw 13% YoY Gain Despite Economic Headwinds

TV sales in China during this year have been noticeably affected by government measures for controlling local COVID-19 outbreaks. During this second half of the year, TV panel prices have fallen to a new record low, and brands have also been aggressively cutting prices so as to meet their annual shipments targets. However, despite all these, TV sales in China for the Singles’ Day period still fell nearly 10% YoY. Turning to the North America, TV sales there shrank by 16.5% YoY for 1H22 as the rapidly mounting inflationary pressure squeezed consumers’ budgets.

Around that same time, TV brands also reached their limit in terms of inventory accumulation. To reduce the glut, brands conducted inventory check across all sections of their supply chains and made significant revisions to their procurement plans. Now, in 2H22, brands have been aggressively spurring demand. Full-scale promotional activities commenced on Amazon’s Prime Day, and TV sales were then ramped up to a peak on Black Friday. Among brands, TCL made the largest price concession for this year, cutting the price of its 55-inch Mini LED backlit model by 70% to US$199. Other brands also energetically promoted their particular product models in the holiday sales competition.

On account of brands’ efforts, TV sales in North America for the Black Friday period rose by 13% YoY. While China and North America have exhibited very contrasting performances for the busy season, it is also clear that TV brands on the whole have gradually lowered their inventories to a relatively optimal level after months of promotional activities across channels and corrections to panel procurements.

Shipments of 8K TVs Are Projected to Drop for First Time in 2022 by 7.4% YoY, but Growth Will Return Next Year with Unit Figure Rising Above 500,000

Another notable development that TrendForce has observed in the TV market is the tepid performance of high-end products. Due to the lack of supporting broadcasting content and high retail prices, most TV brands have not been particularly keen on pushing 8K models. And after years of advocacy, Samsung remains the single dominant brand for 8K TVs with a market share almost 70%. Additionally, high inflation has eaten into consumers’ budgets this year. TrendForce therefore projects that 8K TV shipments will register a YoY decline for the first time in 2022, dropping by 7.4% to just about 400,000 units.

It is also worth noting that Europe as one of the main sales regions for 8K TVs could be affected by the updated EU energy consumption labelling scheme (i.e., Energy Efficiency Index). Specifically, energy consumption rules have been further tightened so that some older 8K models could be banned from the region starting in March 2023. However, Samsung is planning to launch new 8K models that meet the updated energy consumption standards. Moreover, display panel suppliers continue to promote 8K products so as to widen adoption among TV brands. TrendForce currently forecasts that shipments of 8K TVs will surpass the 500,000 unit mark for 2023, registering a YoY growth of 20%.

Shipments of WOLED TVs Are Projected to Drop by 6.2% YoY for 2022 and Fall Further by 2.7% YoY for 2023

TrendForce’s latest research on panel prices finds that LCD panel prices have plummeted. In fact, the price of a 55-inch UHD LCD was 4.8 times lower than the price of a WOLED (white OLED) O/C panel at the end of 3Q22. With the price difference between the two panels returning to where it was at the start of 2020, selling WOLED TVs have been quite challenging for brands that do offer this kind of product. Therefore, TrendForce estimates that shipments of WOLED TVs will shrink by 6.2% YoY to 6.29 million units for 2022. Assuming that LG Display does not want to sacrifice profitability, it will maintain a conservative pricing strategy when quoting WOLED panels next year. Given this situation, TrendForce forecasts that WOLED TV shipments will dip again by 2.7% YoY for 2023.

For more information visit TrendForce.