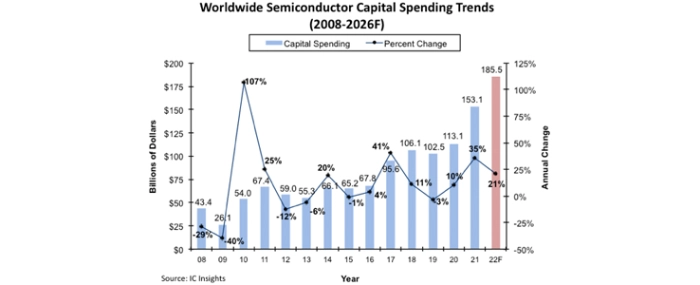

Semi Capex on pace for 21% growth to $185.5B this year

IC Insights has adjusted its 2022 worldwide semiconductor capital-spending forecast that now shows a 21% increase this year, to USD 185.5 billion.

The analysts expect 2020-2022 to be the first three-year period of double-digit Capex growth since 1993-1995.

The revised outlook represents a decrease from USD 190.4 billion and 24% growth that was forecast at the beginning of this year. Even though its lowered, the revised Capex forecast still represents a new record high level of spending. In fact, if industry capital spending rises as forecast by a double-digit amount this year, it will – as stated earlier – mark the first three-year period of double-digit capital expenditure gains in the semiconductor industry since 1993-1995.

Wafer fab utilisation rates at many integrated device manufacturers (IDMs) remained well above 90% through the first half of this year and many semiconductor foundries operated at 100% utilisation rates, as orders remained robust during the economic recovery from the Covid-19 pandemic.

Combined two-year semiconductor capital spending in 2021 and 2022 is now expected to reach USD 338.6 billion. IDMs and foundries are spending heavily on new manufacturing capacity for logic and memory devices built with leading-edge process technology. However, strong demand and ongoing shortages of many other essential chips such as power semiconductors, analog ICs, and various MCUs, have caused suppliers to boost manufacturing capacity for those products as well.

While all of that is positive news, a menacing cloud of uncertainty looms on the horizon. Soaring inflation and a rapidly decelerating worldwide economy caused semiconductor manufacturers to re-evaluate their aggressive expansion plans at the mid-point of the year. Several (but not all) suppliers – particularly many leading DRAM and flash memory manufacturers – have already announced reductions in their Capex budgets for this year. Many more suppliers have noted that capital spending cuts are expected in 2023 as the industry digests three years of robust spending and evaluates capacity needs in the face of slowing economic growth.

For more information visit IC Insights