June swoon – IC sales turn negative

A never-before-seen decline in June IC market driven by steep drop in memory pricing, says IC Insights.

The IC market recorded its first-ever June sequential sales decline this year, based on data from WEMA, SIA, and WSTS dating back to 1976. Typically, high single-digit or double-digit sales gains have been the pattern for June IC sales. Even in its previously weakest year (1985), June IC sales increased by 1%. Never, until this year, have June IC sales declined.

This extraordinary result was startling for at least two reasons. First, June is a quarter-ending five-week month and that alone has historically been enough to generate a sales uptick compared to the four-week month of May. Second, June is normally one of the strongest months of the year for IC sales since OEMs are buying chips to build into their new systems in time for back-to-school and end-of-year holiday sales.

The biggest contributor to June’s total IC market decline was the sudden and dramatic drop in memory IC sales. A dramatic revenue downturn is not readily evident in the 2Q22 financial results from Samsung, SK Hynix, and Micron since June’s decline offset gains made in April and May. However, Micron is forecasting a -17% sales drop for its fiscal 4Q (ending in August). Samsung and SK Hynix do not provide next-quarter sales guidance, but it is reasonable to presume that their 3Q outlooks are somewhat similar to what Micron has forecast.

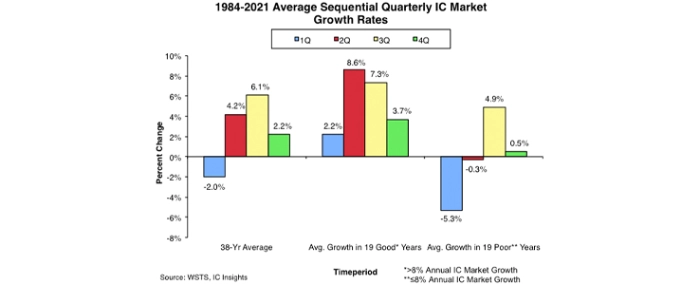

The second and third quarters of the calendar year are typically the strongest two quarters for IC sales. Since 1984, 2Q sales results have grown by an average of 4.2% and 3Q sales have increased an average of 6.1%. Naturally, these figures swing higher or lower depending on where the industry is in its supply-demand cycle, economic strength, and other factors.

In 2Q22, IC market growth was flat, falling below the long-term average. Based on IC Insights’ assessments of company sales outlooks for the rest of this year, it appears that 3Q and 4Q IC sales stand a good chance of falling short of their long-term average growth rates, as well.

Much of the current IC market weakness is due to economic concerns caused by rising inflation, ongoing supply chain disruptions, and from suppliers and OEMs working to reduce IC inventory levels. Several semiconductor companies noted during their 2Q22 financial earnings calls that inflation has put a dent in consumer discretionary spending. Weakness was particularly evident for shipments of consumer PCs, low- and mid-level smartphones, televisions, game consoles, and personal electronic devices.