Reducing the cost of batteries will become more important

As a consequence of rising power battery raw material prices, a number of global new energy vehicle (NEV) brands including Tesla, BYD, NIO, Li Auto, and Volkswagen, have successively raised the sales prices of electric vehicles in 1Q22.

TrendForce believes that power batteries are the core component that account for the greatest portion of an EV’s overall cost and reducing the cost of power batteries will be an important strategy for companies to remain competitive in the future. As technology continues to innovate, lithium iron phosphate batteries are expected to account for more than 60% of installed capacity in the global power battery market by 2024.

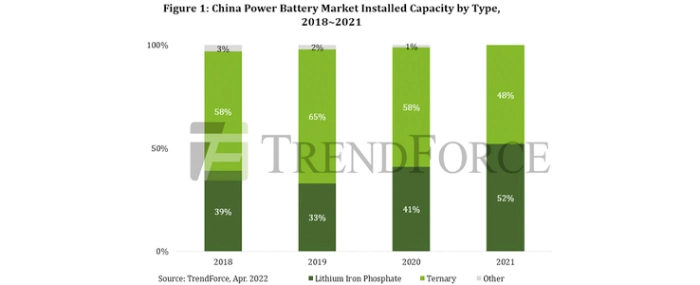

TrendForce indicates, from the perspective of the world's largest EV market, China, the power battery market reversed in 2021 and lithium iron phosphate batteries officially surpassed ternary batteries with 52% of installed capacity. Lithium iron phosphate installed capacity continued to grow in 1Q22, rising to 58%, and demonstrating a growth rate far beyond that of ternary batteries. However, from the perspective of the global EV market, thanks to the increase in the penetration rate of NEVs in Europe and the United States, ternary batteries still accounted for a market share of more than 60% in 2021, far exceeding that of lithium iron phosphate batteries, which captured a market share of approximately 32~ 36%.

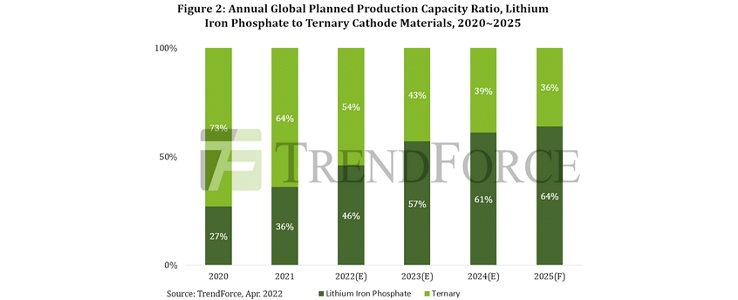

Although the current gap between these two materials remains substantial, according to production capacity planning of global new energy battery cathode material manufacturers in the past two years, the scale and speed of lithium iron phosphate materials expansion will far exceed that of ternary materials. According to TrendForce investigations, planned expansion projects announced by global cathode material manufacturers are currently concentrated in China and South Korea, with a nominal total planned production capacity of over 11 million tons, of which planned production capacity of lithium iron phosphate cathodes accounts for approximately 64%. However, since planned production capacity exceeds market demand, there will be a certain shortfall between the industry’s total planned production capacity and actual future production capacity. It remains to be seen to what level actual effective production capacity can rise in the future.

It is worth noting, as the price of core battery raw materials such as lithium, cobalt, and nickel has moved up clearly since 2H21 and the global power battery supply chain is plagued by uncertainty including the Russian-Ukrainian war and the global pandemic, there will be a short-term disparity between the growth rate of supply and demand and companies will focus more on reducing the cost of battery materials and supply chain security, two major issues related to future competitiveness. As a result of this trend, TrendForce expects the cost-effective advantage of lithium iron phosphate batteries to become more prominent and this type of battery has an opportunity to become the mainstream of the terminal market in the next 2-3 years. The global installed capacity ratio of lithium iron phosphate batteries to ternary batteries will also move from 3:7 to 6:4 in 2024