© Trendforce

Analysis |

EV market continue to drive demand for 6” SiC wafers

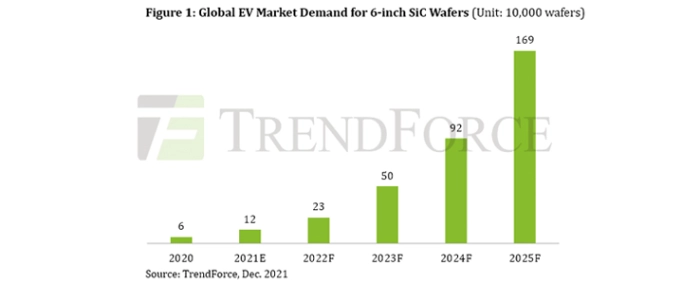

Demand from the global automotive market for 6-inch SiC wafers is expected to reach 1.69 million units in 2025 thanks to the rising penetration rate of EVs and the trend towards high-voltage 800V EV architecture, according to TrendForce’s latest investigations.

Owing to the EV market’s substantial demand for longer driving ranges and shorter charging times, automakers’ race towards high-voltage EV platforms has noticeably intensified, with various major automakers gradually releasing models featuring 800V charging architectures, such as the Porsche Taycan, Audi Q6 e-tron, and Hyundai Ioniq 5.

The arrival of the 800V EV charging architecture will bring about a total replacement of Si IGBT modules with SiC power devices, which will become a standard component in mainstream EV VFDs (variable frequency drives). As such, major automotive component suppliers generally favor SiC components. In particular, Tier 1 supplier Delphi has already begun mass producing 800V SiC inverters, while others such as BorgWarner, ZF, and Vitesco are also making rapid progress with their respective solutions.

At the moment, EVs have become a core application of SiC power devices. For instance, SiC usage in OBC (on board chargers) and DC-to-DC converters has been relatively mature, whereas the mass production of SiC-based VFDs has yet to reach a large scale. Power semiconductor suppliers including STM, Infineon, Wolfspeed, and Rohm have started collaborating with Tier 1 suppliers and automakers in order to accelerate SiC deployment in automotive applications.

It should be pointed out that the upstream supply of SiC substrate materials will become the primary bottleneck of SiC power device production, since SiC substrates involve complex manufacturing processes, high technical barriers to entry, and slow epitaxial growth. The vast majority of n-Type SiC substrates used for power semiconductor devices are 6 inches in diameter. Although major IDMs such as Wolfspeed have been making good progress in 8-inch SiC wafer development, more time is required for not only raising yield rate, but also transitioning power semiconductor fabs from 6-inch production lines to 8-inch production lines. Hence, 6-inch SiC substrates will likely remain the mainstream for at least five more years.

On the other hand, with the EV market undergoing an explosive growth and SiC power devices seeing increased adoption in automotive applications, SiC costs will in turn directly determine the pace of 800V charging architecture deployment in EVs.