© TrendForce

Analysis |

Smartphone production see modest 5.7% QoQ increase in 3Q21

The smartphone market is showing an improvement in demand during the second half of this year due to the peak season for e-commerce promotional activities and the easing of COVID-19 outbreaks in regions such as Southeast Asia, according to TrendForce’s latest investigations.

However, there have been significant shortages of components including 4G SoCs, low-end 5G SoCs, display panel driver ICs, etc. The persistent component gaps are constraining smartphone brands from raising device production for the second half of the year. Looking at 3Q21, the quarterly total smartphone production came to around 325 million units, a 5.7% QoQ increase. Even so, not only does the QoQ increase in smartphone production for 3Q21 fall short of the QoQ increase for the same quarter last year, but the quarterly production volume for 3Q21 also shows a weaker performance result when compared with figures from 3Q20 or from 3Q19, prior to the emergence of the pandemic.

As for the total production for the whole 2021, TrendForce has lowered the projection to 1.335 billion units with a YoY growth rate of 6.5%. The previous projection was 1.345 billion units with a YoY growth rate of 7.3%. This downward correction mainly reflects the impact of the component gaps on device production. Going forward, an important point of observation in the smartphone market is whether the pandemic will further weaken demand. Also, the other significant variables that will influence future smartphone demand include geopolitical tensions, distribution of production capacity in the foundry market, and global inflationary pressure.

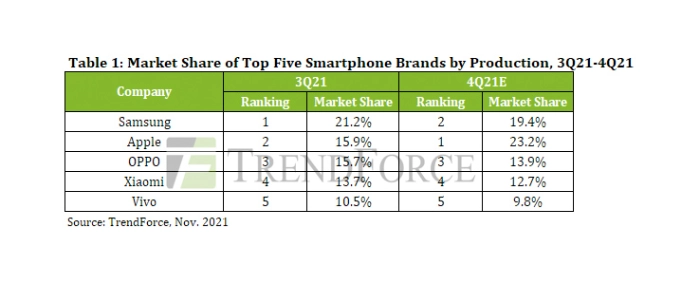

While smartphone production for 3Q21 reached about 325 million units, the release of new models helped Apple retake second place in the global ranking

Samsung raised its smartphone production by 17.9% QoQ to 69 million units for 3Q21. The growth was mainly attributed to the stabilization of the capacity utilization rates of its device assembly plants in Vietnam. Samsung continued to top the global ranking of smartphone brands with the largest market share in production terms. Apple released four new iPhone models under the iPhone 13 series in 3Q21. Thanks to their contribution, the total iPhone production for 3Q21 registered a QoQ increase of 22.6% to 51.5 million units. With this result, Apple was also able to climb to second place in the global ranking. In terms of product development, Apple is staying with the plan to release its third-generation iPhone SE in 1Q22 and four models under a new series in 2H22. The third-generation iPhone SE is expected to be a major instrument in helping Apple establish a presence in the market segment for mid-range 5G smartphones. Its production volume for 2022 is forecasted to reach 25-30 million units.

OPPO marginally raised its smartphone production by 3% QoQ to 51 million units for 3Q21, thereby capturing third place in the ranking. Xiaomi held fourth place as its smartphone production for the same quarter fell by 10% QoQ to 44.5 million units. Vivo’s smartphone production for 3Q21 was relatively constant compared with the previous quarter, coming to around 34 million units. With this result, Vivo was ranked fifth. The production figures of these three Chinese brands include devices under their respective sub-brands (i.e., OPPO’s Realme and OnePlus; Xiaomi’s Redmi, POCO, and Black Shark; and Vivo’s iQoo). Looking at the three brands’ production performances in 3Q21, TrendForce notes that there is a high degree of overlap in terms of target market as well as a high degree of similarity in offerings. Hence, their production performances directly hinge on their ability to acquire enough of the components that are now in short supply.

Honor will expand into the overseas markets next year as part of its plan for a comeback

After spending the first half of this year stocking up on components and undergoing business restructuring, Honor is now on a more solid footing and will attain an annual smartphone production of 43.5 million units. In the global ranking of smartphone brands by annual production for 2021, Honor is expected to take eighth place. Also, Honor as an independent brand has obtained access to Google Mobile Services. Therefore, it plans to expand to other markets outside China next year and leverage the sales expertise that it has acquired from Huawei in order gain a bigger share of the overseas markets. Regarding Honor’s sales strategy as a whole, the main focus is still on the domestic market. As for the overseas markets, Honor will continue Huawei’s strategy and avoid India where competition revolves around low pricing. Instead, Honor will attempt to establish itself in regions such as Russia, the wider Europe, and South America. In general, Honor’s rise will likely affect the market shares of the other aforementioned brands. How much market share Honor will gain depends on its ability to have sufficient inventory of components that are now in short supply.