© TrendForce

Analysis |

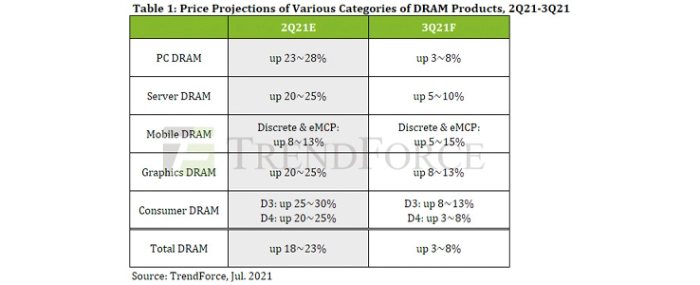

DRAM prices for 3Q21 to undergo minor QoQ increase

As third quarters have typically been peak seasons for the production of various end-products, the sufficiency ratio of DRAM is expected to undergo a further decrease in 3Q21, according to TrendForce’s latest investigations.

However, DRAM buyers are now carrying a relatively high DRAM inventory due to their amplified purchases of electronic components in 1H21. The QoQ increase in DRAM contract prices are hence expected to slightly narrow from 18-23% in 2Q21 to 3-8% in 3Q21. Looking ahead to 4Q21, TrendForce believes that DRAM supply will continue to rise, thereby leading to either a further narrowing of price hikes or pressure constraining the potential price hike of DRAM products.

PC DRAM prices are expected to rise by 3-8% QoQ due to continued constraints on production capacities

From the perspective of demand, the stay-at-home economy has resulted in persistently high demand for notebook computers. Although discrepancies still exist among notebook brands’ inventory levels of various components, these brands are still making an aggressive attempt at maximizing their production of notebooks. However, as most of these brands are still carrying about 8-10 weeks’ worth of PC DRAM inventory (which is relatively high), PC DRAM purchasing strategies from the buyers’ side will therefore remain relatively conservative. From the perspective of supply, due to the rising demand for server DRAM, the production capacity allocated to PC DRAM is still in a severe supply crunch. Hence, DRAM suppliers are firm in their attitudes to raise PC DRAM quotes, and TrendForce expects the price negotiations between PC DRAM buyers and suppliers in 3Q21 to become both lengthier and more difficult as a result, with contract prices likely finalized at the end of July. Even so, what is now certain is that both sides have reached some level of understanding regarding the ongoing price hike of PC DRAM products. TrendForce forecasts a 3-8% increase in PC DRAM contract prices for 3Q21.

QoQ increase in server DRAM prices for 3Q21 are expected to narrow to 5-10% due to buyers carrying a relatively high inventory

With regards to demand, in spite of the minor increase in the shipment of whole servers, server DRAM buyers are less aggressive in their server DRAM procurement compared to the previous quarter. For instance, CSPs in North America and in China are currently carrying more than eight weeks of server DRAM inventory. In other words, procurement activities for server DRAM will gradually decline in the coming quarters in accordance with market demand. Notably, some Tier 2 clients will continue to procure server DRAM in 3Q21 since they did not sufficiently stock up in the prior quarters, and this demand will likely result in upward momentum for server DRAM prices. With regards to supply, the three major DRAM suppliers (Samsung, SK Hynix, and Micron) are limited by the fact they are currently carrying a relatively low inventory of server DRAM. As such, these suppliers will attempt to maintain their profitability by increasing prices each quarter. It should also be pointed out that the decreased DRAM demand from smartphone brands has in fact allowed more wiggle room for server manufacturers to negotiate for more favorable server DRAM prices. TrendForce thus believes that, before the supply side and demand side can reach an agreement, negotiations for server DRAM prices will become increasingly lengthy, and that server DRAM contract prices for 3Q21 will likely increase by 5-10% QoQ once negotiations are finalized.

Mobile DRAM prices are expected to defy market realities and increase by 5-15% QoQ, with potential risks of high price and low demand

In terms of demand, certain smartphone brands are now carrying a relatively higher inventory of mobile DRAM owing to Southeast Asia’s worsening COVID-19 pandemic, which led smartphone brands that primarily manufacture and sell their products there to begin lowering their production targets in 2Q21. In addition, some smartphone brands have set overly ambitious production targets; combined with the current shortage of foundry capacities, the discrepancies among the supply of smartphone components have now become more apparent, in turn forcing brands to slow down their mobile DRAM procurement in order to adjust their component inventories first. Demand has remained strong from clients in the smartphone market since 4Q21, so the supply fulfillment rate of the three major DRAM suppliers for their smartphone clients will be consistently higher compared to clients in other markets. As DRAM demand from non-smartphone applications ramps up and results in higher profitability than mobile DRAM, the three major DRAM suppliers will continue to adjust their production capacities in accordance with the shifting supply and demand from various segments, thus resulting in an increasingly constrained supply of mobile DRAM.

It should be pointed out that DRAM market leader Samsung has generally tried to minimize the profit discrepancies among its various products. Furthermore, the price hike in Samsung’s mobile DRAM products was relatively lower compared to Micron in 1H21. As a result, in view of the weakening mobile DRAM demand in 3Q21, Samsung will increase its mobile DRAM prices to a more notable extent compared to its US competitors. Going forward, Samsung’s price hike will lead its competitors to retool their pricing strategies, subsequently leading to an even wider price increase across the entire mobile DRAM market. As such, TrendForce expects mobile DRAM prices to increase by 5-15% QoQ in 3Q21, which is a step up compared to 2Q21. On the other hand, this price hike against market realities may potentially lead to a further decline in mobile DRAM demand, resulting in a situation with high price and low demand.

Graphics DRAM prices are expected to increase by 8-13% QoQ due to tight supply of GDDR6

Regarding graphics DRAM demand, many cryptocurrency miners were previously intent on mining ETH with older graphics cards as it reached peak prices. Nevertheless, the recent bearish turn of the cryptocurrency market has indirectly had an impact on demand for graphics cards equipped with GDDR5, although most of this impact primarily affected the spot market. For the contract market, more than 90% of graphics DRAM applications have migrated to GDDR6 products, which are now in short supply since new graphics cards are equipped with GDDR6 memory and are in high demand. In addition, the vast majority of GDDR6 stock from DRAM suppliers is currently cornered by graphics card manufacturers and game console manufacturers, thereby further limiting the graphics DRAM supply available to small and medium OEMs/ODMs. Regarding graphics DRAM supply, although GDDR6 accounts for more than 90% of the three major DRAM suppliers’ graphics DRAM production, demand for GDDR6 still far exceeds supply because end product demand has also migrated to GDDR6. As orders for server DRAM gradually ramp up in 3Q21, DRAM suppliers will prioritize fulfilling demand from the server market first. Hence, graphics DRAM contract prices for 3Q21 are expected to increase by 8-13% QoQ.

Consumer DRAM prices are expected to increase by up to 13% QoQ in light of strong demand

At the moment, consumer DRAM demand is relatively robust from the consumer electronics market and the telecom market. In addition, as China has been accelerating its build-out of 5G infrastructures and its rollout of WiFi 6 in the post-pandemic era, the overall demand for consumer DRAM remains strong going forward. On the other hand, the three dominant DRAM suppliers are slowing down their transition of production capacities from DDR3 products to CMOS Image Sensors or other Logic IC products now that the consumer DRAM market has taken a bullish turn. However, in the medium-to-long term, the general trend in the DRAM industry will still point to the elimination of the older 25/20nm process technologies and the continued migration towards more advanced 1Znm and 1αnm processes. As a result, given DDR3 products’ declining supply and strong demand, DDR3 prices for 3Q21 are expected to increase by 8-13% QoQ, while DDR4 prices are expected to undergo a minor growth of 3-8% QoQ in accordance with mainstream PC and server DRAM prices.