© Trendforce

Analysis |

Historical high for notebook panel shipment in 1Q21

The onset of the COVID-19 pandemic in turn generated a high demand for notebook computers. While demand began ramping up in 2Q20, subsequently resulting in a shortage in 3Q20 and 4Q20, the shortage in the notebook market has yet to be resolved even now, according to TrendForce’s latest investigations.

The high demand for notebooks is estimated to propel the quarterly shipment of notebook panels to a historical high of 65.3 million units in 1Q21, which is a 3.5% increase QoQ and a 46.5% increase YoY.

With regards to supply and demand, TrendForce believes that the current shortage of notebook panels can primarily be attributed to the soaring market demand for notebooks. In terms of supply, notebook panel shipment underwent YoY increases of more than 20% during each quarter from 2Q20 to 4Q20. At the moment, panel orders from notebook manufacturers still exceed the order fulfillment capacity of panel suppliers by about 30-50%, as panel suppliers are bottlenecked by the shortage of certain semiconductor components, such as DDICs and T-cons.

Given the extremely tight supply of panels relative to demand, notebook panel prices have skyrocketed accordingly. Case in point, quotes for 11.6-inch panels, which are among the mainstream and are widely used for Chromebooks, are now closing in on quotes for 14-inch and 15.6-inch panels. As such, the high profitability of notebook panels have led panel suppliers to set more aggressive shipment targets this year.

In particular, after CEC-Panda sold its Nanjing-based Gen 8.5 fab and Chengdu-based Gen 8.6 fab last year, the company currently possesses a sole remaining Gen 6 fab in Nanjing. While this fab has never manufactured notebook panels in the past, plans for manufacturing 11.6-inch panels are now underway, with mass production expected to start in 2Q21, owing to the extremely high market demand for notebook panels. It should also be pointed out that HKC has been mass producing 11.6-inch panels since February 2021. The company is expected to start mass producing 14-inch panels in 2Q21 and 15.6-inch as well as 13.3-inch panels in 2H21. HKC aims to ship about 10 million notebook panels this year.

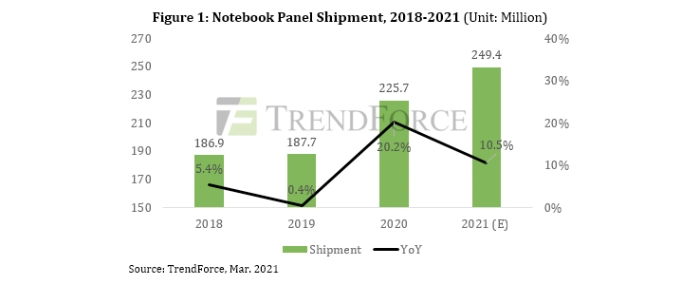

TrendForce indicates that the current demand for notebook panels will likely persist through 3Q21. However, as the shortage situation has persisted for more than three quarters since it surfaced in 2Q20, some notebook manufacturers may begin overbooking panel orders due to the expectation of further shortages. Therefore, if the actual market demand were met ahead of expectations, panel suppliers may potentially slow down their panel shipments in 2H21. Even so, the new normal brought about by the pandemic will continue to power the global digital transformation. For instance, in response to the digitization of distance learning, the education sector is expected to generate recurrent demand for Chromebooks. As a result, TrendForce has a positive outlook on the annual shipment volume of notebook panels for 2021, which is expected to reach 249 million units, a 10.5% increase YoY.