© TrendForce

Electronics Production |

Automotive applications to account for 3%+ of total DRAM Bit consumption in 2024

There are four major categories of automotive DRAM applications, including infotainment, ADAS, telematics, and D-clusters (digital instrument clusters), according to TrendForce’s latest report.

Of the four categories, infotainment applications require the highest DRAM content, although DRAM consumption per vehicle across all four categories remains relatively low at the moment. In contrast to ADAS, infotainment applications present a lower barrier to entry for companies, since current legislations and automotive safety standards governing infotainment are not as stringent, making infotainment a highly attractive market for various semiconductor companies and memory suppliers. TrendForce expects infotainment to remain the primary driver of automotive DRAM consumption through 2024, while all four automotive DRAM applications will together likely comprise more than 3% of total DRAM consumption as autonomous driving technology progresses toward higher levels. As such, automotive DRAM applications represents an emerging sector whose potential for growth should not be underestimated.

TrendForce further indicates that the safety requirements of automotive parts are far higher than those of consumer electronics in terms of both quality and durability. As a result, the release of new vehicle models may take up to 3-5 years from development and verification to release. Vehicles still under development are therefore likely to greatly surpass existing models in terms of both memory content and specifications.

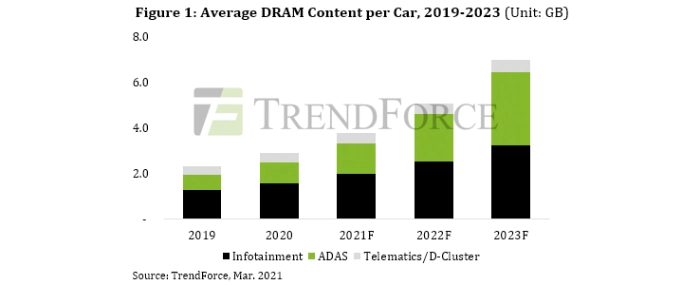

Infotainment will comprise the majority of automotive DRAM consumption, while total automotive DRAM consumption is still relatively low

Infotainment applications represent the highest bit consumption among the major automotive DRAM applications, due to the computing demand of basic media entertainment functionalities in vehicles now. However, most vehicles with these functionalities require only about 1-2GB (gigabytes) of DRAM, which is the current mainstream, since infotainment applications are still relatively basic. As infotainment systems evolve towards higher image qualities and higher video bitrates, solutions requiring 4GB in DRAM content are also under development, with high-end systems transitioning to 8GB in DRAM content. On the other hand, given the close viewing distance involved in automotive infotainment, video bitrates must be sufficiently high to minimize lag. DRAM specifications for infotainment applications are therefore gradually shifting from DDR3 2/4Gb (gigabits) to LPDDR4 8Gb in order to satisfy the high data transfer speed and bandwidth required to achieve a sufficiently high video bitrate and optimal viewing experience.

With regards to ADAS, development is currently divided into two architectures: centralized vs. decentralized (or distributed) systems. Decentralized systems include such devices as reverse parking sensors, which require about 2/4Gb of DRAM. Centralized systems, however, require 2/4GB of DRAM, since data collected from various sensors located throughout the vehicle are transferred to and computed in a central control unit in centralized ADAS. Most vehicles with autonomous driving capabilities currently available on the market are still equipped with ADAS levels 1-2 and therefore require relatively low DRAM content. Going forward, as the development of autonomous driving technologies moves to level 3 and beyond, along with the potential inclusion of AI functionalities, vehicles will need to be able to integrate and process enormous amounts of data collected from sensors in real-time, as well as perform immediate decision-making with the collected data. Given the high bandwidth required for such operations, there will be a corresponding increase in automotive demand for higher-spec DRAM as well, and automotive DRAM for ADAS applications is expected to transition from DDR3 to LPDDR4/4X and even LPDDR5 or GDDR5/HBM later on, though this transition will require more time before it can take place, due to existing regulations.

The mainstream memory products used for telematics, or automotive communication systems, are MCP (Multi Chip Package) solutions. Due to the frequency and compatibility requirements of baseband processors contained in these systems, all telematics applications require the use of LPDRAM. As V2V and V2X gradually become necessities in the auto industry, automakers will place a high importance on memory bandwidth, meaning automotive DRAM for telematics will gradually shift from mainstream LPDDR2 solutions to LPDDR4/LPDDR5. Even so, the growth of telematics will depend on the pace of global 5G infrastructure build-out, since telematics requires 5G networks for fast peer-to-peer connections. As for D-clusters, DRAM bit consumption per vehicle for this application category comes to either 2Gb or 4Gb, depending on the individual vehicle’s degree of digitization for its instrumental panel. However, DRAM consumption for D-clusters is not expected to undergo significant future growths, and D-clusters may potentially be merged with infotainment into a single centralized system going forward.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please visit their website.