© FBDi

Analysis |

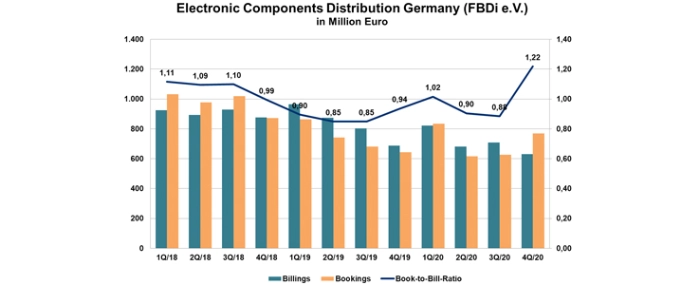

German components distribution: Downturn stopped

German distribution of components, according to the FBDi, increases order intake by 23% in the fourth quarter. Sales down "only" by 8.1%. Full year 2020 shows deep traces of the pandemic.

While other regions of the world achieved - in some cases significant - growth in 2020 despite the pandemic, Europe and particularly the German electronic components market were slow. Sales of the distribution companies organised in the Fachverband Bauelemente-Distribution (FBDi e.V.) fell by 14.6% to EUR 2.85 billion, dropping well below the former peak of EUR 3.6 billion in 2018. At the end of the year, the situation became somewhat friendlier, with the fourth quarter ending with a minus of 8.1% and EUR 632 million. By contrast, order intake grew at an above-average rate of just under 23% to EUR 769 million, corresponding to a book-to-bill ratio of 1.22.

At product level, Passive Components suffered most, with -21% over the whole year. At Q4, with a minus of 3.4% and EUR 77.5 million, they lagged behind electromechanical components, which fell by 9.5% to EUR 87 million, but were significantly more stable in a full-year comparison (-5.3%) and represented a good 13% of the sales pie (passives: 11.7%). Semiconductors were down 15.6% year-on-year, bringing Q4 sales to around EUR 414 million. The share of the total market remained stable at 68%. The smaller product areas such as sensors (-8.9%), power supplies (-8.2%) and displays performed better, with the latter even increasing significantly (but this is probably due to the reporting mechanism of some members).

"This was a surprisingly positive end to a thoroughly bad year. The fact that we are now sliding into a supply crisis for components, with in some cases extreme bottlenecks and equally significant price increases by many manufacturers, is due to two significant circumstances: First, many market participants behave too digitally and reduce their inventory at the slightest sign of a crisis, only to immediately go into panic action in the opposite case. And secondly, Europe is a sub-strategic region whose total component requirements correspond to those of a single large contract manufacturer in China. The fact that, in the event of shortages, large smartphone giants are supplied in a different way than the multitude of European OEMs and also differently than the "system-critical" automotive industry should come as no surprise to anyone who has read the FBDI's market statistics for the past 15 years," says FBDi Chairman Georg Steinberger in a press release.

The FBDI takes a skeptical view of the German government's recent offensive to secure greater independence from Asian contract manufacturers in the semiconductor industry.

"We know of many programs from the past that have not changed the current situation. The semiconductor industry thrives on innovative chip designs and intellectual property, on know-how and billions invested in groundbreaking manufacturing technology, and last but not least on huge volumes that usually only come from large platforms (smartphones, tablets, laptops, etc.) and thus global key customers. 50 billion euros in funding sounds nice, but where will the money go? If this is managed in a similar way to Corona aid, then good night," says Steinberger.