© TrendForce

Analysis |

Cree divest its LED operations as LED supply chain continues its shift to Asia

After global LED giant Cree divested its lighting business in 2019, the company has announced its plan to sell its LED business to SMART Global Holdings (SGH) for USD 300 million. TrendForce indicates that Chinese manufacturers have quickly risen in the LED industry in recent years, benefiting from superior production capacities and cost optimization measures.

These manufacturers are continuing to capture the existing market shares of major overseas LED companies, such as Nichia, OSRAM OS, Lumileds, and Cree. Furthermore, given the poor state of the global economy in the past two years, companies that were previously dominant in the LED industry must now deal with the difficult reality of having their business operations or stocks sold off to other companies.

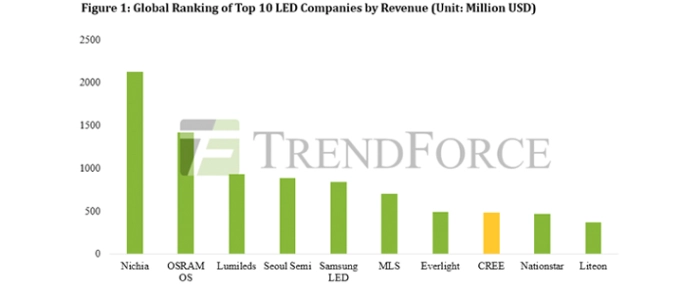

Cree’s LED packaging and lighting businesses generated more than USD 1 billion in yearly revenues for the 2013-2014 period. At the time, its LED business ranked second only to that of Nichia in terms of revenue. However, in light of competition from Chinese companies fielding aggressive pricing strategies and the gradually slowing growth of the LED lighting market in recent years, Cree’s yearly LED revenue reached a mere USD 480 million in 2019, and the company’s global ranking slid from among the top three to eighth place.

Final price of Cree’s LED business is limited by regulatory complications with U.S. aerospace and military technologies

According to TrendForce, Cree is estimated to sell its LED business for a mere USD 300 million, a far lower price compared to similar transactions by Lumileds and OSRAM OS. This low price is primarily due to the myriad restrictions and export controls by the U.S. government specifically targeting sales of technology companies. In addition to Cree’s role as a supplier of LED lighting products, the company’s subsidiary WolfSpeed offers a range key components made from SiC (silicon carbide), a third-generation compound semiconductor material. As WolfSpeed has been in close collaboration with the aerospace and defense industries in the U.S., it possesses a significant number of sensitive technologies. On the other hand, the primary advantage of Cree’s LED technologies comes from the fact that its SiC substrates massively raises the overall performance of its LED products. Since it is difficult to separate Cree’s LED-related patents/technologies from its SiC technologies, potential buyers of Cree’s business are therefore limited to U.S.-based parties, in turn placing a limit on the final sales price.

The LED supply chain will continue its gradual transition to Asia, while Cree may potentially look for chip OEM partners in the future

Under intense pricing pressure from its competitors, Cree has in recent years gradually outsourced its LED business to OEM partners with mature technologies, including Fujian Lightning Optoelectronic and Lextar. TrendForce indicates that, even with the upcoming ownership transfer of Cree’s LED business, Cree is at the moment still an important client of its OEM partners, and its management structure will not change in the short run. That is why the overall trend of LED supply chain shifting to Asia has not changed. As well, SGH does not have a need for SiC substrate development, meaning SGH will likely adopt a more flexible business strategy which involves looking for Asia-based chip OEM partners in the future.