© melpomenem dreamstime.com

Analysis |

DRAM capex spending expected to decline 20% in 2020

The DRAM market is poised for a modest recovery in 2020, but suppliers are being very cautious, strategic, and thorough in their analysis of market conditions before they consider any further upgrades or decide to move ahead with any new DRAM wafer fab plans, says IC Insights.

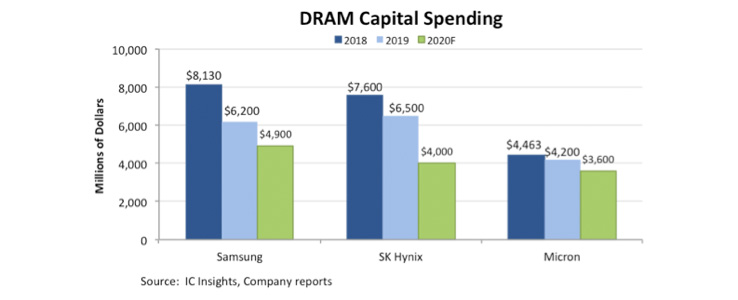

The graph below shows DRAM capex budgets for the three major suppliers. Each is expected to make further cuts in its DRAM capital spending in 2020 as most new facilities and upgrades to current fabs are in place to handle near-term demand. Among the three big DRAM players, IC Insights forecasts that Samsung’s DRAM capital expenditure budget will decline 21% to USD 4.9 billion this year, SK Hynix is expected to trim its DRAM capex budget 38% to USD 4.0 billion, and Micron is forecast to trim its DRAM capex by 16% this year to USD 3.6 billion.

New fabs, once built, must run at very high or full capacity given the high levels of capital expenditures required to build and equip them. Investing USD 6-10 billion in a wafer fab only to see it operate at partial capacity would have a destructive financial impact on any supplier. Consequently, DRAM makers will continue to closely monitor capacity and expansion plans in the coming months in order to limit potential damage from another supply/demand imbalance.

Samsung, SK Hynix, and Micron are wrapping up their significant DRAM capacity expansions in 2020, and each has made it clear that they will be restrained about how fast they progress with building and ramping their new manufacturing lines.

Even smaller niche DRAM suppliers like Winbond are being guarded. Winbond is building a new fab in Kaohsiung, southern Taiwan. It was originally scheduled for completion at the end of 2020 with commercial production slated for 2021. However, the company has now rescheduled equipment move-in for January 2022.

Collectively, suppliers are expected to allocate $15.1 billion to DRAM capex spending this year, a 20% decline from USD 19.1 billion in 2019 and down from the record high of USD 23.2 billion spent for DRAM in 2018.

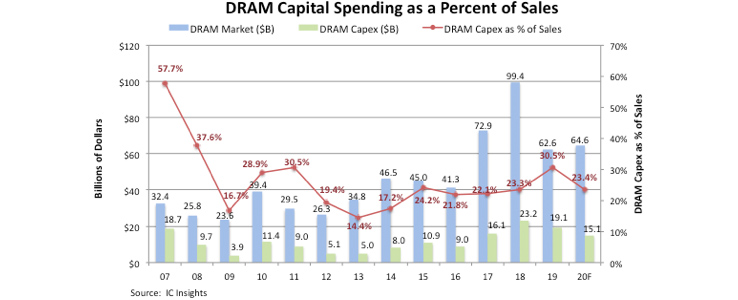

Even with elevated capital spending levels the past few years, DRAM capex as a percent of DRAM sales was not terribly out of line with what the industry has seen since 2015. It is interesting to note, however, that with the 37% DRAM market collapse in 2019, DRAM capex spending as a percent of sales jumped to 30.5%, the highest level since 30.5% in 2011.

New fabs, once built, must run at very high or full capacity given the high levels of capital expenditures required to build and equip them. Investing USD 6-10 billion in a wafer fab only to see it operate at partial capacity would have a destructive financial impact on any supplier. Consequently, DRAM makers will continue to closely monitor capacity and expansion plans in the coming months in order to limit potential damage from another supply/demand imbalance.

Samsung, SK Hynix, and Micron are wrapping up their significant DRAM capacity expansions in 2020, and each has made it clear that they will be restrained about how fast they progress with building and ramping their new manufacturing lines.

Even smaller niche DRAM suppliers like Winbond are being guarded. Winbond is building a new fab in Kaohsiung, southern Taiwan. It was originally scheduled for completion at the end of 2020 with commercial production slated for 2021. However, the company has now rescheduled equipment move-in for January 2022.

Collectively, suppliers are expected to allocate $15.1 billion to DRAM capex spending this year, a 20% decline from USD 19.1 billion in 2019 and down from the record high of USD 23.2 billion spent for DRAM in 2018.

Even with elevated capital spending levels the past few years, DRAM capex as a percent of DRAM sales was not terribly out of line with what the industry has seen since 2015. It is interesting to note, however, that with the 37% DRAM market collapse in 2019, DRAM capex spending as a percent of sales jumped to 30.5%, the highest level since 30.5% in 2011.

For more information visit © IC Insights

New fabs, once built, must run at very high or full capacity given the high levels of capital expenditures required to build and equip them. Investing USD 6-10 billion in a wafer fab only to see it operate at partial capacity would have a destructive financial impact on any supplier. Consequently, DRAM makers will continue to closely monitor capacity and expansion plans in the coming months in order to limit potential damage from another supply/demand imbalance.

Samsung, SK Hynix, and Micron are wrapping up their significant DRAM capacity expansions in 2020, and each has made it clear that they will be restrained about how fast they progress with building and ramping their new manufacturing lines.

Even smaller niche DRAM suppliers like Winbond are being guarded. Winbond is building a new fab in Kaohsiung, southern Taiwan. It was originally scheduled for completion at the end of 2020 with commercial production slated for 2021. However, the company has now rescheduled equipment move-in for January 2022.

Collectively, suppliers are expected to allocate $15.1 billion to DRAM capex spending this year, a 20% decline from USD 19.1 billion in 2019 and down from the record high of USD 23.2 billion spent for DRAM in 2018.

Even with elevated capital spending levels the past few years, DRAM capex as a percent of DRAM sales was not terribly out of line with what the industry has seen since 2015. It is interesting to note, however, that with the 37% DRAM market collapse in 2019, DRAM capex spending as a percent of sales jumped to 30.5%, the highest level since 30.5% in 2011.

For more information visit © IC Insights

.png)