© TrendForce

Analysis |

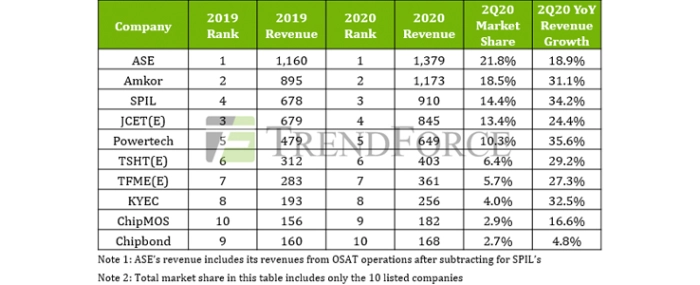

ASE takes the lead among Top10 largest OSAT companies in 2Q20

The border restrictions and national lockdowns instituted by various governments due to the COVID-19 pandemic’s impact in 1Q20 resulted in low inventory levels for clients of packaging and testing (OSAT, outsourced semiconductor assembly and test) companies and for distribution channels as well, according to TrendForce’s latest investigations.

As the supply chain gradually recovered in 2Q20, governments began instituting fiscal policies to stimulate the economy. These factors, combined with the rise of the stay-at-home economy, led to an increased restocking demand from downstream clients, in turn providing a boost to OSAT revenue, which reached USD 6.325 billion in 2Q20, a 26.6% increase YoY.

TrendForce analyst John Wang indicates that, in spite of downstream OSAT clients’ restocking demand, end-market demand is still likely to be limited in 2H20 because of hostile China-U.S. relations, which have recently reached rock bottom owing to issues such as restrictions placed on Huawei, passage of the Hong Kong national security law, and territorial disputes in the South China Sea. Also contributing to the gloomy outlook of the OSAT industry is the continued spread of the pandemic in areas including the U.S., South America, India, and Southeast Asia.

China-U.S. relations and the pandemic’s outlook are key factors determining global OSAT revenue in 2H20

Market leader ASE recorded quarterly revenue of USD 1.379 billion in 2Q20, an 18.9% increase YoY. Although ASE’s growth in 2Q20 tempered somewhat compared with 1Q20, the company’s upward momentum remained steady, thanks to increased OSAT demand from the 5G telecommunications and consumer electronics industries. On the other hand, Amkor, SPIL, Powertech, and KYEC benefitted from their increased OSAT capacity for consumer electronics, memory products, and 5G chips. The four companies each registered more than 30% YoY growths in revenue. Furthermore, these OSAT companies accelerated their shipment schedules in 2Q20, driven by redirected orders resulting from the pandemic and by the September 15th deadline after which U.S.-based OEMs will terminate manufacturing services for Huawei.

Chinese OSAT giants JCET, TSHT, and TFME each saw an estimated near-30% YoY increase in revenue in 2Q20 as a result of high OSAT demand from smartphones, AI chips, and wearables in China, where the pandemic was effectively brought under control. Finally, ChipMOS and Chipbond each posted a 16.6% and 4.8% YoY increase in revenue in 2Q20. Their performances were mostly attributed to the recovering large-sized display panel demand and sales performances in the retail markets, which led to high LDDI and TDDI capacity utilization rates.