© Trendforce

Analysis |

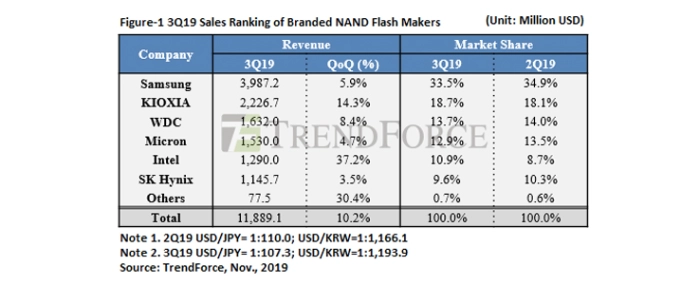

3Q19 NAND Flash revenue grows amidst resurging pre-peak season demand

3Q19 NAND flash industrial revenue showed a nearly 15% growth of total bit shipment, owing to the seasonality-driven demand for products shipments and the additional product shipment made available in preparation for U.S. tariffs, says the DRAMeXchange research division of TrendForce.

On the other hand, suppliers were able to improve their inventory levels and deter a mass sell-off in the wafer market driven by low prices, in turn diminishing the dip in contract price. 3Q19 industrial revenue reached USD 11.9 billion, a 10.2% growth.

Looking towards 4Q19, we project an improvement in the revenue performance of suppliers, once contract price adjusts itself to properly reflect the Yokkaichi power outage-induced price hike, and peak season market demand becomes healthy again.

Samsung

Samsung’s performance in bit shipment exceeded previous expectations and reached a QoQ growth of more than 10%, thus continuing the company’s longstanding advantage in the high-capacity storage market, including such use cases as servers and mobile devices. This performance took place on the heels of Intel’s new platform release, as well as the release of multiple flagship phones in 2H19. In addition to stabilizing its 3Q19 inventory levels, Samsung was able to limit its ASP decline to no more than 5%, registering a USD 39.87 billion revenue, a 5.9% QoQ growth.

In terms of production capacity, Samsung is decreasing its Line 12 2D NAND products, as previously planned. As the company moves toward advanced process nodes, it will maintain the same amount of 3D NAND wafer input. In terms of new capacity, Samsung’s second semiconductor plant in Xian will start manufacturing in 1H20, while its second Pyeongtae-based memory fab is projected to begin operation in 2H20.

SK Hynix

After the 40% surge in 2Q19 bit shipment, SK Hynix’s bit shipment has slowed down in 3Q19, with a 1% QoQ drop. However, its ASP underwent a 4% QoQ growth because of price stabilization and reductions in wafer sales. On the whole, revenues from NAND flash reached USD 1.146 billion, a 3.5% QoQ growth.

In terms of production capacity planning, SK Hynix has seen consecutive quarterly decreases this year mainly due to cutbacks in its 2D NAND capacity. This is accompanied by a small expansion in mainstream 3D NAND capacity, most of which is handled in the M15 fab.

Kioxia

Despite being negatively affected by the power outage incident in Yokkaichi, Kioxia was able to increase its bit shipment by more than 20% QoQ as a result of strong seasonality and the demand placed by Apple’s new smartphone release. Nonetheless, ASP fell by 5% QoQ, leading to a revenue of USD 2.227 billion, with a 14.3% QoQ growth.

In terms of production capacity, although all of Kioxia’s production lines at Yokkaichi have resumed operation, the outage ensured Kioxia’s bit output to lag behind that of its competitors. Regarding the company’s development in 2020, the Kitakami-based K1 fab finished construction in October; K1 is projected to begin operations in 1H20 at the earliest. This is expected to increase Kioxia’s bit shipment share to return to pre-outage levels.

(Note: Toshiba Memory was rebranded to Kioxia on Oct. 1, 2019.)

Western Digital

Western Digital’s 3Q19 bit shipment grew approximately 9% QoQ thanks to peak season-induced demand. Also, the decline in ASP came to a halt due to the power outage at the Yokkaichi plant and the influx of additional demand. Western Digital posted a USD 1.632 billion revenue, an 8.4% QoQ growth.

In terms of production capacity planning, following the power outage in the Yokkaichi campus, the production lines began to recover in mid-July, with the newest estimates of production loss being 4 exabytes. In terms of new production lines, Western Digital invested USD 64 million into the K1 plant in Iwate Prefecture in 3Q19, which is projected to start production of BiCS4 or other products based on the more advanced process nodes in 2020.

Micron

Owing to the growth of mobile devices shipments and surging client-side inventory demand, Micron’s NAND flash revenue reached USD 1.53 billion, a 4.7% QoQ growth. The company’s bit shipment also grew by more than 10% QoQ because of last-minute redirected orders by its main clients in July and August. However, Micron’s ASP still declined by over 5% QoQ.

In term of production capacity, Micron announced the grand opening of its new fab in Singapore in August, providing additional support to its effort to adopt new architecture for NAND flash products. There has been no significant change in production capacity for Micron’s other NAND flash production facilities, such as its other Singapore- and Manassas-based plants.

(Note: The 3Q19 period overlaps with Micron’s fiscal 4Q19, which ran from June to August.)

Intel

Because of a strong increase in both enterprise SSD and client SSD shipment, Intel grew its 3Q19 bit shipment by more than 50%. However, despite its Clients’ increased adoption of products based on more advanced process technologies and of higher density specifications, ASP fell by over 10%. Overall, Intel’s NAND flash revenue reached USD 1.29 billion, a 37.2% QoQ growth.

In terms of production capacity, Intel’s Dalian-based fab is expected to maintain its production capacity until the end of the year, with no mention of any expansion plans in 2020.

For more information visit TrendForce

For more information visit TrendForce