© TrendForce

Analysis |

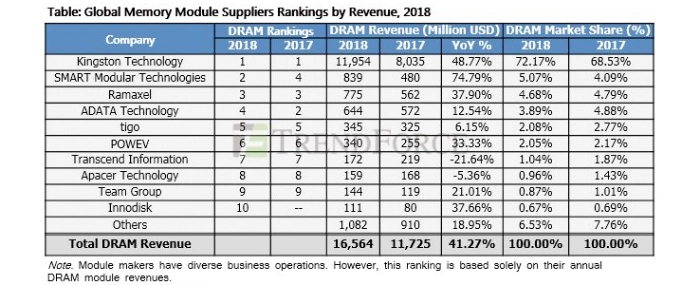

Top 10 DRAM module suppliers by revenue, which grew by over 40% YoY in 2018

According to the latest global DRAM module supplier rankings by DRAMeXchange, a division of TrendForce, although DRAM prices took a downturn in 2H18, ASP for the whole year came above 10% in 2017.

Along with the increase in shipments, this put total revenue for the global module market 2018 at USD 16.6 billion, a 41% increase YoY.

Looking back at price trends in 2018, TrendForce points out that spot prices remained high in 1H19, even surpassing contract prices by over 20%, and thus generated plenty of revenue and profit for module manufacturers. Despite end demand's being dragged down by the overall situation in 2H19, clients' increasing inventory levels and the subsequent dive in DRAM prices, most module manufacturers still sailed through violently fluctuating prices with proper management. Thus although the baseline revenue was already set quite high in 2017, module manufacturers still enjoyed an above-40% revenue growth in 2018.

Kingston the King in Spot Markets; ADATA Slides to No. 4

TrendForce's statistics show that the top five memory module manufacturers already take up nearly 88% of total sales revenue in 2018, whereas the top ten form 93% of total operating revenue for the global module market, cementing the existence of a Matthew effect in the market.

Kingston continues its winning streak, taking the top spot yet again in 2018. As DRAM prices and supply rise hand in hand, Kingston's DRAM revenue grew by nearly 50% to create a new historical record. Besides efficient cost management, Kingston has made outstanding progress in China's markets, pushing market penetration up to a new 72% high.

American company Smart Modular Technologies enjoyed a revenue growth of over 70%, ascending from fourth place in 2017 to second in 2018. China supplier Ramaxel also performed brilliantly in 2018, with DRAM revenue growing by nearly 40% YoY and becoming the third greatest module house.

Although Taiwanese supplier ADATA Technology's DRAM revenue made up over 60% of its total revenue in 2018 and registered a growth of 12.5%, a new high after the last eight years, that growth didn't compare to Ramaxel and Smart Modular Technologies, causing it to slide to number four. ADATA will continue to expand in emerging industries such as gaming, industrial control, automotive applications and electric vehicle motors, whose overall revenues and profit scales may hope to grow gradually in the process.

Furthermore, tigo, a longstanding DRAM module contender in the game, registered small growths in revenue last year and remained where it stood in the rankings at fifth place. POWEV, another Shenzhen module manufacturer, also made gradual strides in promoting its own brand in addition to conducting foundry business, and grew by over 30% in revenue YoY, sitting safe and sound at sixth place.

Transcend Continues to Make the Transition into Niche Markets, While Apacer Makes Strides in Industrial Control

Looking at the performance of other Taiwanese suppliers, we see Transcend holding on to seventh place, but due to falling quotes and the company's continual transitioning, DRAM revenue fell by about 20% YoY. Transcend will still be focusing on industrial control, which yields a better gross profit margin, as well as on total solutions to upgrade Apple products and strategic products such as wearables, in hopes of reducing their amount of business in the highly fluctuating, high-risk spot markets.

Although Apacer, which took eighth place in 2018, saw DRAM revenue scale dipping as a result of the global situation, their continual investment in industrial control led to a YoY profit growth against the falling trend. As the company continues to take on IIoT (industrial IoT) applications, such as nursing and healthcare, spectroscopy and transportation, they may be able to reel in steady profits.

Team Group Surges in the Gaming Business, While Innodisk Rides its Industrial Control Business into the Top Ten

Team Group, at ninth place, continued to center in on gaming and industrial control while working proactively and cross-industrially with brands, PCB manufacturers and peripheral suppliers to increase the exposure their brand receives as well as their variety of gaming products. This drove DRAM revenue growth to above 20%. Team Group still plans on developing business in the gaming sector and expanding their presence in emerging markets in the future to further capitalize on differentiation.

Innodisk, which took tenth place, saw DRAM revenue grow by nearly 40% and made it into the top ten for the first time. The company targets the rather niche field of industrial control, and has always operated steadily owing to the wide distribution of customers over various application segments. Innodisk will be integrating its resources in the future in anticipation of the rise of AI and HPC (high performance computing) and memory applications required by edge computing, and to meet the emerging demand to spring out of AIoT.