© TrendForce

Analysis |

DRAM quotes continue to fall in 2Q

According to the latest investigations by DRAMeXchange, a division of TrendForce, DRAM prices have faced mounting pressure to trend down in 1Q, the traditional offseason.

Not only was this due to the production capacities added in 2H18, which found full expression in 1Q, but also a compressed procurement momentum by a demand side busy clearing out their own inventories. This caused a pronounced double-decline effect: Both DRAM prices and volume fell in 1Q, causing overall production revenue to drop by 28.6 % QoQ.

Looking at 2Q19, ASP for 8GB modules have fallen to USD 34 in April as seen from the final pricings by Tier-1 PC-OEMs, falling by 20% QoQ. Inventory levels kept rising for DRAM suppliers due to lukewarm trade. TrendForce predicts contract prices will keep plunging under as monthly deals are made in May and June and decline by nearly 25% for the whole 2Q. Server DRAMs, which contribute to over 30% of DRAM shipments, will face an even heavier price pressure.

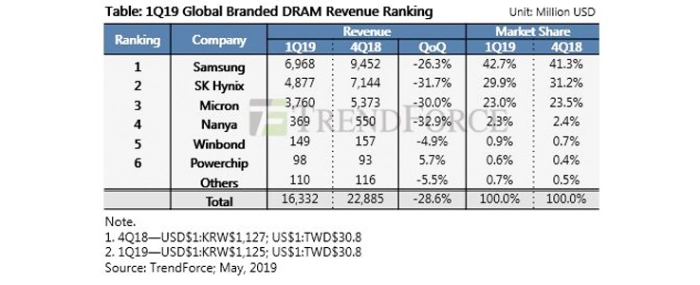

Revenues show dramatic drops QoQ across the board. Market leader Samsung's reference revenue started low and performed better than expected in 1Q mobile DRAM shipments, bringing 1Q sales bit performance on a par with the previous quarter. Still, revenue was still impacted by declining quotes and dropped by 26.3% QoQ and arrived at USD 6.97 billion, with market share recuperating to 42.7%. SK Hynix's sales bit performance slid by 8%, which was slightly better than what it had expected, and arrived at USD 4.88 billion in revenue 1Q, a 31.7% decline QoQ, and took home a 29.9% market share.

Micron continued to hold third place and came to USD 3.76 billion in revenue, sliding by 30.0% QoQ, while market share remained at about 23%. TrendForce predicts that the top three suppliers will continue utilizing aggressive quoting strategies in the coming months under pressure from mounting inventory levels.

Now let's take a look at profitability. Some of Samsung's 1Xnm servers were returned or replaced due to quality issues, which incurred additional operating expenses and lowered profit performance: Its operating margin slid QoQ from 66% to 48%, exhibiting the greatest slide among the three giants. Yet even though quotes have fallen 20% to 30%, Samsung's gross margins from DRAM production still neared 60%. Although Samsung's product issues gave way to a rising SK Hynix's shipments, those shipments were concentrated in March, where prices came to their seasonal low. This brought the 1Q operating margin down from 58% in the previous quarter to 44%.

Since Micron's financial statements spanned the period from December 2018 to February this year, their prices did not register a slide comparable to Korean suppliers', which were calculated from January to March. Hence, Micron performed the best among the top three in operating margins, falling from 58% last quarter to 46%. We will see suppliers' profitability facing further shrinkage as industry prices continue to dive in 2Q.

Technology observations show that Samsung's Line 17 and Pyeongtaek plant (2nd floor) will continue to make the transition into 1Ynm, yet considering current market trends, the company has yet to speed up its transition. In dealing with 1Xnm server issues, Samsung is planning to make capacity allocation adjustments to its production processes in order to reduce damage to a minimum. Meanwhile, SK Hynix's 1Xnm shipments have already risen above 30% in 1Q, and will begin to introduce its 1Ynm processes. Micron Memory Taiwan (formerly Rexchip) currently manufactures all products with 1Xnm technology, and will immediately move towards 1Znm as its next goal, which are poised to make actual contributions in 2020; Micron Technology Taiwan (originally Inotera) already have 1Xnm shipments forming over half of total shipments, and will be raising the proportion of 1Ynm shipments in 1H this year.

For more information visit TrendForce

For more information visit TrendForce