© Trendforce

Analysis |

In-display fingerprint sensors on the rise

Samsung will launch models with in-display fingerprint sensors, following Vivo, Huawei, Xiaomi, and OPPO, says TrendForce. The adoption by these major Android smartphones has constantly increased the penetration of in-display fingerprint technologies, among which ultrasonic and optical fingerprint sensing have made considerable breakthroughs.

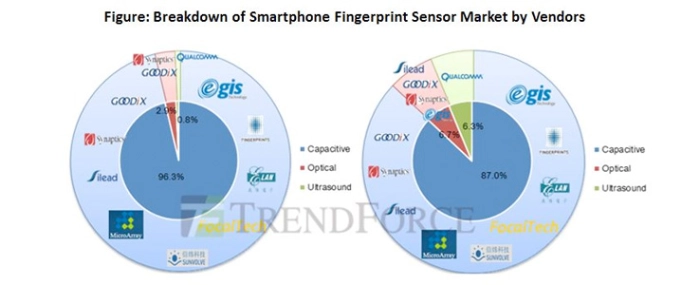

TrendForce estimates that ultrasonic and optical in-display fingerprint sensors will account for 13% of all fingerprint sensor technologies in 2019, significantly up from 3% in 2018.

There are many types of biometric identification technologies adopted by smartphones, with fingerprint sensing, face recognition, and iris recognition to be the major ones. In terms of fingerprint sensors, the development of capacitive solutions is the most mature, while optical and ultrasonic ones have started to make breakthroughs this year. The increasing penetration of full-screen smartphone models has directly boosted the demand for in-display fingerprint sensors.

Optical in-display fingerprint sensors will be increasingly adopted by mid and high-end models

The development of fingerprint sensor technologies has been previously restricted by low yield rate and insufficient investment from the supply chain, says TrendForce. However, with the increasing demand for fingerprint sensors from smartphone vendors like Vivo, the design houses have invested heavily to increase yield rates and seek more cost-effective solutions. The cost of the optical in-display fingerprint sensor of Synaptics was USD 12~15 each in 2017, but has a chance to decrease to lower than USD 8 in 2019, as Goodix, Silead and other companies in turn enter the field. At that time, brands may also embed in-display fingerprint sensors in their mid and high-end models, instead of only in flagships, so as to fit in the design of full-screen.

On the other hand, led by the active product development by Qualcomm, the share of ultrasonic in-display fingerprint sensors is expected to reach 6.3% in the smartphone fingerprint sensor market in 2019. There have been rumors in the market that Samsung will adopt Qualcomm's ultrasonic fingerprint sensors next year. In general, the in-display fingerprint sensor market may grow by multiple times in 2019, and the market will no longer be dominated by optical solutions provided by Synaptics and Goodix.

Regarding the supply chain, it is worth noting that Qualcomm may change the landscape of the traditional capacitive fingerprint sensor market, although it is a latecomer to the competition. If Qualcomm’s products are successfully embedded in Samsung’s phones, and further adopted by flagship models of Chinese smartphone brands in the future at a price close to that of capacitive solutions, then Qualcomm’s participation may influence the sales strategies of existing companies that provide both optical and capacitive solutions. These companies, including Goodix and Silead, may have to lower their prices of both optical and capacitive solutions significantly in order to introduce the products to the middle and high-end smartphone segments.

There will be more Android phones featuring both fingerprint sensing and face recognition

With the decreasing prices, in-display fingerprint sensor has become part of the standard equipment for Android phones at a price of RMB 2,500 or higher. In order to provide consumers with more diversified specs, it is expected that there will be more Android phones featuring both fingerprint sensing (including in-display or conventional ones) and face recognition (including 3D and 2D).

3D sensing technology is still favored by flagships of major brands, and has been constantly improved in terms of costs, design, and algorithm. In addition to Apple’s large-scale adoption of Face ID in 2019, major Android brands will also adopt 3D face recognition in their flagship models. In the long run, 3D sensing will be embedded in middle and high-end smartphones, while 2D face recognition will penetrate into the middle and low-end segments which are more sensitive to costs.