© Trendforce

Analysis |

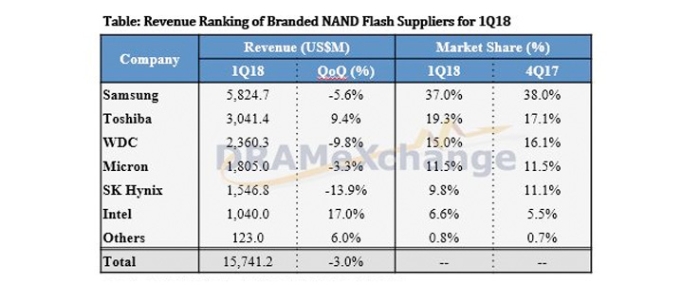

Global NAND Flash revenue dropped by 3% QoQ in 1Q18

The latest analysis by DRAMeXchange, a division of TrendForce, finds that the seasonal headwinds in 1Q18 has resulted in downward corrections of prices.

On the whole, the revenue of branded NAND Flash suppliers dropped by 3% QoQ in 1Q18. Contract prices of eMMC/UFS and SSD products will keep falling in 2Q18 since the market is in slight oversupply. However, NAND Flash suppliers have also slashed prices significantly on products belonging to the standard and high-density categories (e.g. 256GB SSDs, 128/256GB UFS) to help stimulate bit demand growth. DRAMeXchange therefore expects stable revenue performances from NAND Flash suppliers for 2Q18.

Looking ahead to 2H18, stock-up demand related to the next iPhone release and the year-end busy season will stabilize prices of NAND Flash products. In fact, the NAND Flash demand from OEM has been constrained by surging prices for almost one year, so the latest development in price trend will spur OEMs in the PC and smartphone markets to upgrade the storage specifications of their upcoming products. In turn, the demand in the NAND Flash market will return to a state of healthy growth.

Samsung

Samsung’s NAND Flash bit shipments dipped a bit in 1Q18 because of the seasonal headwinds that affected demand from the server/data center and the smartphone markets. The supplier also lowered the prices of its Client and Enterprise SSDs. Consequently, Samsung’s NAND Flash revenue for 1Q18 came to USD 5.82 billion, down by 5.6% QoQ.

Samsung anticipates a demand growth spurt for SSDs once the recent NAND Flash prices decline reaches a satisfactory level. The prices decline will stimulate the Client SSD market and again accelerate SSD penetration among notebook PCs. In the Enterprise SSD market, Samsung will keep promoting its highly competitive PCIe and high-density products with the expectation that lowering prices will increase the average content per box. As for the mobile market, Samsung will continue to encourage smartphone OEMs to raise the storage specifications of their flagship devices.

SK Hynix

SK Hynix’s bit shipments fell by nearly 10% QoQ in 1Q18 due the negative seasonality affecting the demand from the smartphone market. Nevertheless, the supplier’s ASP was supported by the contract prices of its eMCP products and dropped by just 1% QoQ. SK Hynix’s NAND Flash revenue for 1Q18 fell by 13.9% QoQ to USD 1.55 billion.

Mobile NAND Flash products and MCP are currently the focus of SK Hynix’s sales efforts. The overall demand for smartphones however was weak in 1Q18, however, Apple will again start stocking up at the end of 2Q18. Chinese brands, too, will increase the densities of their mid-range and high-end devices from 64/128GB to 128/256GB. This turnaround in demand is expected to benefit SK Hynix’s revenue performance as well as sustaining its bit shipment growth. In terms of technological development, SK Hynix has raised the capacity and yield rate of its 72-layer 3D-NAND process. Following this, the supplier plans to take this solution into the SSD market. DRAMeXchange anticipates that the share of 72-layer 3D-NAND Enterprise SSDs in SK Hynix’s overall shipment will increase significantly within this year.

Toshiba

Despite the traditional slow season for smartphones and lower-than-expected sales of the latest iPhone devices, Toshiba managed to marginally increase its NAND Flash bit shipments in 1Q18 as it began shipping 64-layer 3D-NAND wafers to memory module makers. Furthermore, Toshiba’s ASP rose by nearly 10% QoQ in 1Q18 due to the demand from the module makers and the increase in the average density of its shipped SSDs. Consequently, Toshiba’s NAND Flash revenue for the same period went up by 9.4% QoQ to USD 3.04 billion.

With regard to the sales of Toshiba’s memory business, the deal officially passed the review by China’s regulatory authority on 17 May and is arranged to be completed on 1 June. The successful conclusion of this deal is expected to smooth the construction schedules of Fab 6 and Fab 7 as well as making it much easier to obtain the necessary capital for developing the 96-layer (or more advanced) 3D-NAND technologies. In sum, the Toshiba-Western Digital alliance is now in a better position to compete with other major suppliers in the NAND Flash market.

Western Digital

Western Digital’s 1Q18 bit shipments fell by more than 5% QoQ mainly due to the negative seasonal influence, which also led to sliding shipments for the supplier’s notebook PC and server SSDs. Although Western Digital has done well in the retail market by selling products under various brands, prices of its products have declined on account of the oversupply of NAND Flash and the inventory adjustments that occurred in 1Q18. The supplier’s ASP also fell by nearly 5% QoQ in 1Q18. Consequently, the company’s total NAND Flash revenue for the same period dropped by 9.8% from the prior quarter to USD 2.36 billion.

Micron

Following changes in sales strategy, Micron is gradually shifting its focus from chip and wafer shipments in the channel market to its branded storage products. The supplier scored impressive results in the sales of its SSDs in 1Q18, and its bit shipments also rose by more than 10% QoQ in the same period. However, Micron’s ASP dropped by almost 15% QoQ because of the sharp price decline for SSDs and 3D-NAND TLC wafers in the channel market. With the gain in sales offset by the drop in ASP, Micron’s NAND Flash revenue for 1Q18 came to USD 1.81 billion, a QoQ drop of 3.3%.

Intel

Sales of server SSDs continue to sustain the growth of Intel’s bit shipments, which rose by nearly 30% QoQ for 1Q18. However, the downward price corrections in the NAND Flash market also dragged down Intel’s ASP by about 10% QoQ. Taken together, Intel registered a 17% QoQ growth in its 1Q18 NAND Flash revenue, reaching an impressive total of USD 1.4 billion.

For more information visit Trendforce.

For more information visit Trendforce.