Global fab equipment investment expected to reach $110B in 2025

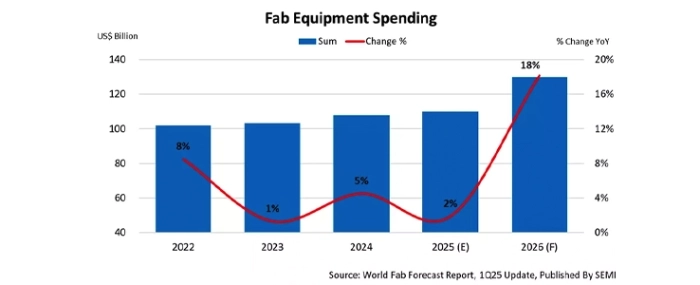

Global fab equipment spending for front-end facilities in 2025 is anticipated to increase by 2% YoY to USD 110 billion, marking the sixth consecutive year of growth since 2020, SEMI reports.

Fab equipment spending is projected to rise by 18% in the following year, reaching USD 130 billion. This growth in investment is driven not only by demand in the high-performance computing (HPC) and memory sectors to support data centre expansions – but also by the increasing integration of artificial intelligence (AI), which is driving up the silicon content required for edge devices.

“The global semiconductor industry’s investments in fab equipment have been edging up for six straight years, and spending is poised to see a strong 18% increase in 2026 as production ramps to meet booming AI-related chip demand,” says Ajit Manocha, SEMI President and CEO, in a press release. “This forecasted capex growth signals an urgent need for intensified workforce development initiatives throughout 2025 and 2026 to deliver skilled workers necessary for the approximately 50 new fabs expected to come online during these two years.”

The Logic & Micro segment is anticipated to be a key driver of growth in fab investments. This growth is primarily fueled by investments in cutting-edge technologies, such as 2-nanometer process and backside power delivery technology, which are expected to enter production by 2026. The Logic & Micro segment is projected to see an 11% increase in investments, reaching USD 52 billion in 2025, followed by a 14% increase to USD 59 billion in 2026.

Overall Memory segment spending is expected to grow steadily the next two years, increasing by 2% to reach USD 32 billion by 2025, with an even stronger growth forecast of 27% in 2026. Investments in the DRAM segment are projected to decline by 6% year-over-year, totalling USD 21 billion in 2025, but are anticipated to rebound with a 19% increase to USD 25 billion in 2026. Conversely, NAND segment spending is expected to recover significantly, rising by 54% year-over-year to USD 10 billion in 2025, and further increasing by 47% to USD 15 billion in 2026.

China Continues to lead in regional fab equipment spending

Despite a decline from a peak of USD 50 billion in 2024, China is expected to maintain its position as the leader in global semiconductor equipment spending, with projections of USD 38 billion in 2025 representing a 24% year-over-year decrease. By 2026, spending is forecast to decline further 5% year-over-year to USD 36 billion.

With the growing penetration of AI technology driving higher memory adoption, Korean chipmakers are planning to invest more in equipment for capacity expansion and technology upgrades, which is expected to position the region as the second highest spending through 2026. Korean investment is forecasted to grow by 29% to USD 21.5 billion in 2025 and by 26% to USD 27 billion in 2026.

Taiwan is set to secure third place in spending as its chipmakers aim to enhance their leadership in advanced technology and production capabilities. Taiwan is projected to spend USD 21 billion in 2025 and USD 24.5 billion in 2026 to meet the growing demand for AI applications across cloud services and edge devices.

The Americas region ranks fourth, with expected spending of USD 14 billion in 2025 and USD 20 billion in 2026. Japan, Europe and the Middle East, and Southeast Asia follow in investments, projected to spend USD 14 billion, USD 9 billion, and USD 4 billion in 2025, and USD 11 billion, USD 7 billion, and USD 4 billion in 2026, respectively.