© adam121 dreamstime.com

Analysis |

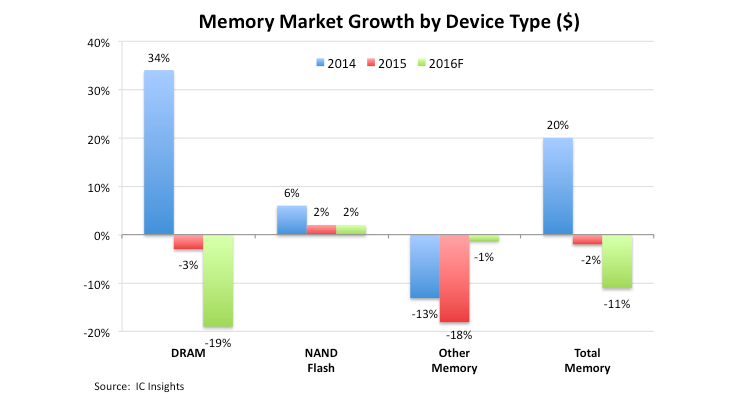

An expected 19 percent DRAM market decline

The year 2016 is not expected to be a good one for the total memory market and the main culprit is DRAM.

Declining shipments of desktop and notebook computers, the biggest users of DRAM, as well as declining tablet PC shipments and slowing growth of smartphone units have created excess inventory and suppliers have been forced to greatly reduce average selling prices in order to move parts, writes market analyst firm IC Insights.

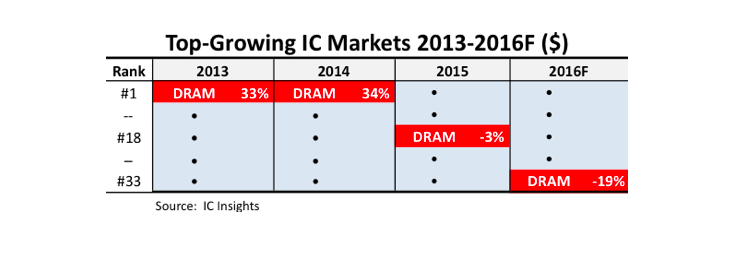

A DRAM ASP decline of 16 percent coupled with a forecast 3 percent decline in DRAM unit shipments is expected to result in the DRAM market declining 19 percent in 2016, lowest among the 33 IC product categories IC Insights tracks in detail. This steep decline will be a drag on growth for the total memory market ( minus 11 percent) and for the total IC market ( minus 2 percent) in 2016.

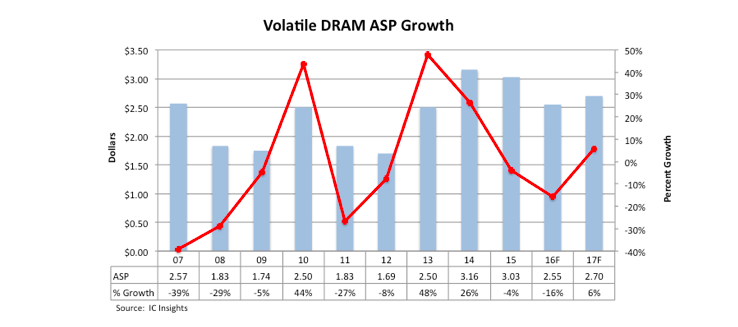

Big swings in average selling price are not new to the DRAM market. Annual DRAM average selling price increases of 48 percent and 26 percent in 2013 and 2014 propelled the DRAM market to more than 30 percent growth each year. In fact, the DRAM market was the strongest growing IC product segment in each of those years. Then, marketshare grabs and excess inventory started the cycle of steep price cuts in the second half of 2015 and that continued through the first half of 2016.

Looking more like the profile of an alpine mountain range, DRAM ASP growth has taken several dramatic upward and downward turns since 2007, confirming the volatility of this IC market segment. When coupled with strength or weakness in DRAM unit shipments, bit volume demand, and the amount of capacity and capital spending dedicated to DRAM production each year, this market can turn quickly up or down.

On a positive note, DRAM ASPs strengthened in late 2Q/16 and are forecast to continue growing through the balance of 2016 and into 2017. The boost to DRAM ASP is expected to come from demand for enterprise (server) systems, which have been selling well due to the need to process “big data” (e.g., the Cloud and the Internet of Things). Also, low-voltage DRAM continues to enjoy solid demand for use in mobile platforms, particularly smartphones. Demand from new smartphone models is expected to help contribute to increasing DRAM ASPs through the end of this year and into 2017.

The upward DRAM ASP trend may be short lived, however, as two China-based companies, Sino King Technology in Hefei, China, and Fujian Jin Hua IC Company, plan to enter the DRAM marketplace beginning in late 2017 or early 2018. It remains to be seen what devices and what technology the two new entrants will offer but their presence in the market could signal that another round of price declines is around the corner.

-----

More can be found at © IC Insights.